CommentsWhy did the Bar not apply the rule of law? Why did the Bar continue the lawyer's and CPA's agenda of dividing and destroying our family? Why assume our family was already divided when I'm writing the Bar to stop it? Is making our family appear divided the justification for not holding the lawyer accountable? Please judge for yourself. Did the Bar frame our family to cover-up for the lawyer? Our Mother did not hire the lawyer Edward White. The CPA Joanne Barnes brought him in. History suggests the CPA unilaterally brought the lawyer in just like the lawyer unilaterially brings the CPA in (I do need to check with Jo Ann Barnes as to a technical question as to whether or not any of your father's trust comes into this. I do not think it does, but there have been many changes in the law since that trust was established. I will have to ask her to bill us for that advice and any other technical tax matters I am not comfortable with. I can do most of the rest of the tax work and save the estate some money. (From Mr. White's letter to our sister, Jean Nader, April 22, 1992). When I wrote the Bar in 1992 I assumed she did because I automatically trusted the system. I know more after twenty-six years. The evidence for exposing accounting fraud is in exposing the accounting trails. Expose the accounting trails at http://www.book467page191money.com and see how much money disappeared. Then things will fall into place. There is a reason those in control won't allow it. There is a reason these accounting trails have been concealed since they were entered into the public Court records in 1993. Virginia BarFebruary 10, 1993 - Virginia Bar to Anthony OConnell, Trustee, in part (I added the numbers in bold and altered the spacing for clarity). I wrote the Virginia Bar in 1992 to stop the lawyer from tearing our family apart. The Bar blamed our family, by using the false premise that our family was already torn apart, and used that false premise to justfy immunity for the lawyer. This is a pattern. Tearing the victimized family apart makes the fraudsters immune. It appears to be the perfect cover. Our family was whole. I wrote the Bar to keep it whole. I believe the Bar's words highlighted in purple create the false premise that our family was already torn apart. This is the lawyer's and CPA's agenda.

3. Your complaint alleges that the Respondent served as co-executor of your father's estate 3 along with your mother and that the Respondent allegedly withheld certain information concerning a trust which was set up under your father's will in which you were named as a trustee.

4. According to your complaint, you retained the Respondent in 1987 to handle a real estate closing and you allege that the Respondent appointed himself co-trustee on the note securing that transaction. Then, the day prior to closing, Respondent allegedly informed you that he was not representing your interests in this real estate transaction. You have also claimed that the Respondent has handled your mother's estate incompetently. 5. With respect to your first complaint, it appears that your mother, rather than you, retained the Respondent for legal assistance in her capacity as executrix of your father's will. 4 Apparently, your mother removed you from her will as a co-executor and nominated the Respondent in your place. However, none of these matters fall within the scope of the Code of Professional Responsibility particularly in view of the fact that you and the Respondent did not share an attorney-client relationship.

6. Your father's will poured over into a trust which you were nominated trustee. By your own complaint, you admit that you hired another attorney 5 to look into the funding of the trust, i.e., what distributions the estate would make to the trust. It is my understanding that you came to Virginia to qualify as a trustee. Again, in respect to that matter, there is no attorney client relationship between you and the Respondent, Mr. White.

7. In the absence of an attorney-client relationship between you and Mr. White, Mr. White was under no ethical obligation to follow any of your directions or instructions nor was he obligated to communicate directly with you. His ethical duties regarding competence, promptness and communication were owed to your mother. 6

8. It is my understanding, based upon a reading of your complaint, that the Respondent and your attorney reached an agreement 7regarding the funding of the trust and the Respondent agreed to cooperate by providing your attorney with a draft8 of the final accounting of your father's estate. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| JEAN M .O'CONNELL ESTATE TAX ANALYSIS | ||||

| CASH(?), NOTES, STOCKS & BONDS. | ||||

| ck Wash Gas Light Co. 8/1/91 | 105.00 |

|||

| ck Signet 8/5/91 | 39.00 |

|||

| ck A. G. Edwards 8/15/91 | 2,346.63 |

|||

| ck Kemper Mun Bond Fund 4/30/91 | 162.86 |

|||

| ck Kemper Mun Bond Fund 5/31/91 | 162.86 |

|||

| ck Kemper Mun Bond Fund 7/31/91 | 162.86 |

|||

| ck Kemper Mun Bond Fund 8/30/91 | 162.86 |

|||

| Ck Nuveen Fund 3/1/9 | 63.00 |

|||

| Ck Nuveen Fund 5/1/91 | 63.00 |

|||

| ck Nuveen Fund 6/3/91 | 63.00 |

|||

| ck Nuveen Fund 8/1/91 | 66.50 |

|||

| ck Nuveen Fund 9/3/91 | 66.50 |

|||

| ck American Funds 9/9/91 | 424.76 |

|||

| Sovran Bank #4536-2785 | 3,310.46 |

|||

| First Virginia Bank #4076-1509 | 22,812.52 |

|||

| Fx Co. Ind Dev Bond | 109,587.00 |

|||

| FranklinxVa. Fund 4556.001 sh | 50.507.84 |

|||

| Investment Co. of America 3861.447 sh | 65.663.91 |

|||

| Kemper Mun Bond Fund 2961.152 sh | 30,396.23 |

|||

| Nuveen Premium Inc Mun Fund 700 sh | 6,450.60 |

|||

| Washington Gas Light Co. 200 sh | 6,375.00 | (corrected 8/10/2018) | ||

| Signet Banking Corp 198 sh | 4,331.25 |

|||

| Lynch Properties note | 518,903.26

|

|||

| Travelers Check | 20.00 |

|||

| 1988 Plymouth Van | 8,000.00 |

|||

| Am Funds 5/10/91 | 326.60 |

|||

| USAA Subscriber savings acct | 25.10 |

|||

| SUB TOTAL | 830,599.10 |

|||

| OTHER ASSETS | ||||

| 1990 Virginia Tax refund | 1,605.58 |

|||

| Debt from Harold O'Connell Trust | 659.97 |

|||

| Blue Cross refund | 88.78 |

|||

| SUB TOTAL | 2,354.33 |

|||

| JOINT ASSETS | ||||

| Hallmark Bank #1107849600 | 40,796.81 |

|||

| REAL ESTATE | ||||

| 15 acres Fairfax Co. Va. 53.9006% interest | 323,403.60 |

|||

| TOTAL ASSETS | 1,197,153.84 |

|||

| -------------------------------------------------------- | ||||

| DEBTS | ||||

| Colonial Emerg Phys (med bill) | 10.40 |

|||

| Fairfax Circ Ct. letters | 14.00 |

|||

| Jean M. Nader probate tax reimb | 1,269.00 |

|||

| Sovran Bank Car loan payoff | 1,364.97 |

|||

| Checks | 15.89 |

|||

| Commissioner of accounts Inventory | 61.00 |

|||

| IRS 1991 1040 return | 15,332.00 |

|||

| Va. Dept Tax 1991 return | 2,856.00 |

|||

| Jean M. Nader, hills pd | 8,559.00 |

|||

| Sheila Ann O'Connell-Shevenell, cem bill | 475.00 |

|||

| Co-Executors' Commission | 41,529.96 |

|||

| Commissioner of Accounts fee for Accounting | 1,048.25 |

|||

| TOTAL DEBTS AND EXPENSES | 72,535.46 |

|||

| JEAN M. O'CONNELL ES'I'A'l'E TAX ANAI.YSIS [page 2] | ||||

TAX COMPUTATION |

||||

| GROSS ESTATE | 1,197,153.84 |

|||

| DEBTS & EXPENSES | 72,535.46 |

|||

| ACC 75% | ACC 60% | |||

| TAXABLE ESTATE | 1,124,615.38 |

1,043,767.48 | 995,256.94 | |

| TENTATIVE TAX 41% bracket | 396,893.53 |

363,744.67 | 343,950.21 | |

Unified Credit before gift comp |

192,800 | |||

| Unified Credit used for gifts | 9,784 |

|||

| UNIFIED CREDIT | 183,016.00 |

183,016.00 | 183,016.00 | |

| CREDIT FOR VIRGINIA TAX | 40,375.58 |

35,201.12 | 32.934.39 | |

| NET FEDERAL TAX | 127.999.82 | |||

| VIRGINIA TAX | 32.934.39 | |||

| ---------------------------------------------- | ------ | ------------ | ---------- | --------- |

| TOTAL ESTATE TAXES | 213,877.53 |

180,728.67 | 160,934.21 | |

14. The third complaint involved an allegation that Mr. White allegedly withheld a $75,000 distribution until you agreed to obtain your own legal counsel.14 With respect to this allegation, Mr. White, in his capacity as an administrator or

executor of an estate is under no obligation by law to make a interim distribution to you. Whether an interim distribution is made is entirely discretionary and the law requires a distribution to be made only upon the filing of a final accounting.

14 False.

My seeing our family lawyer, Mr Ed Prichard, had nothing to do with the $75,000 distribution. In retrospect, I believe Mr White releasing the $75,000 distribution just after I saw Mr. Prichard, was a set up to make it look that way.

I saw Mr. Prichard to resolve a conflict Mr White planted in our family. He gave our innocent sister Jean Nader a bad document to give to me for my signature. I know its bad but my sister doesn't. So I appear as the source of the problem instead of Mr White. There were five "receipts" for our Mother's vehicle; Three by Edward White or anonymous, and two by me. Mr White's create accounting entanglements. His first one is - "RECEIVED of the Estate of Jean M. O'Connell, one 1988 Plymouth Station Wagon of a value of $8,000.00".

I am guessing Mr White wrote three documents for the car and instructed innocent Jean Nader to give me the first two for my signature: The only thing needed to create a wedge through the family is to give a trusting family member a bad document to give to another family member for signature. The trusting family member believes it is a good document and the family member who is to sign it can't convince the trusting family member that it is a bad document and that it should not be signed, because it would create accounting entanglements. The known documents by Edward White or anonymous create accounting entanglements.

1992.03.31 (Edward White (using Jean Nader to mail it) to Anthony O'Connell)

"Dear Tony

I hope you are having a good day-

Enclosed is

(1) the Van Title,

(2) a death certificate

(3) a court appointment and a

(4) receipt.

You need # 1, 2, 3 to have the van transferred to your name-

The receipt # 4, must be returned to me or Ed White as soon as possible because it must be filed with our accounting to the court-"Enclosure:

"Received of the Estate of Jean M. O'Connell, one 1988 Plymouth Station Wagon of a value of $8,000"There are five documents for the car; three by Edward White or anonymous, and two by Anthony O'Connell.

(1) "RECEIVED of the Estate of Jean M. O'Connell, one 1988 Plymouth Station Wagon of a value of $8,000.00"

(2) Unknown.

I am guessing that this is what Edward White is referring to in his letter of April 22, 1992, and one that I am supposed to sign: "Enclosed is an agreement which should satisfy Tony as to the car. It cannot be any clearer"///// "Of course he will furnish that receipt."

I am guessing that this is what Jean Nader wanted me to sign when we meet on or about May 9, 1992, at the dedication of Jean O'Connell's garden at Goodwin House West in Fairfax County, Virginia, but I didn't look at it because I had given up on getting a good document from Edward White and I had already gotten E. A. Prichard advice on how to write a proper document and had sent it to my sisters on May 5, 1992, with a copy to Edward White.(3) "AGREEMENT CONFIRMING DISTRIBUTION OF VEHICLE

We, Jean M. Nader and Sheila O'Connell-Shevenell, hereby confirm that one 1988 Plymouth Van was distributed to our brother, Anthony M. O'Connell by the Estate of Jean M. O'Connell, and that we hereby confirm and agree to that distribution. We further confirm and agree that this distribution shall not be charged against Anthony M. O'Connell's share of the estate and that *the remaining net proceeds of the estate after settlement of all debts and obligations shall be divided in three equal shares.

DATE: *_____ *_____

Jean M. Nader (seal) Sheila O'Connell (seal)"

* . . the remaining net proceeds of the estate after settlement of all debts and obligations shall be divided in three equal shares.- This creates unnecessary complications and openings for confusion and conflict. Buying my sister's share of the vehicle for one dollar does not.I wrote two documents for the car. Mr. White ignored both.

(1) "April 21, 1992 Today I received from the estate of Jean O'Connell, one 1988 Plymouth Station Wagon, VIN IP4FH4037JX221930. Anthony M. O'Connell"

(2) "It is my decision as a beneficiary of the estate of Jean O'Connell, that Anthony O'Connell may purchase the 1988 Plymouth Van now in the estate, VIN l4FH4037JX221930, for one dollar.

Name Jean Nader (seal) Date May (9?), 92"

"It is my decision as a beneficiary of the estate of Jean O'Connell, that Anthony O'Connell may purchase the 1988 Plymouth Van now in the estate, VIN lP4FH4037JX221930, for one dollar.

Name Sheila O'Connell (seal) Date 5-9-92"Reference

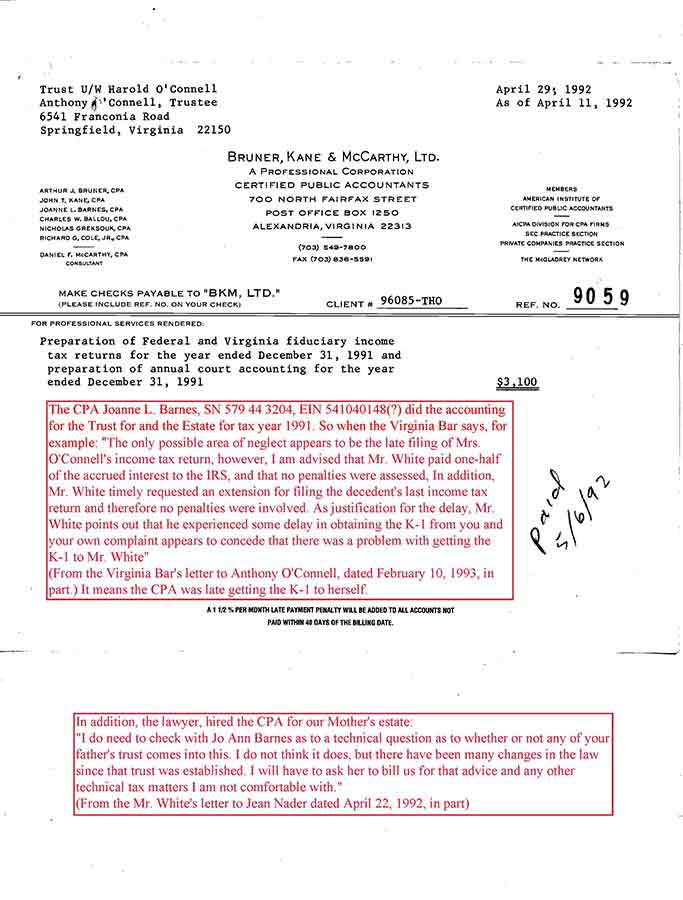

15. With regard to your allegations of incompetence and delay on the part of Mr. White in handling your mother's estate, I have determined that Mr. White has filed in a timely manner the inventory and first accounting for this estate. No delinquency notices or show cause summonses have been issued. The only possible area of neglect appears to be the late

filing of Mrs. O'Connell's income tax return, however, I am advised that Mr. White paid one-half of the accrued interest to the IRS, 15 and that no penalties were assessed,

15 . . . I am advised that Mr. White paid one-half of the accrued interest to the IRS, . . . - This creates an accounting entanglement like those covering the accounting trails of the First Account for our Mother's estate at book 467 pages 193 - 194:

1. Decedent: had a POD account in Hallmark Bank with Jean Nader. The bank erroneously paid the amount to the estate. This figure is the interest earned on that sum while in the estate account. (Accounting entanglement $270.82)

2. This represents interest earned in the estate account on the amount of the disbursement while the disbursal was delayed. This is to equalize the disbursements among the legatees. (Accounting entanglement $230.14)

3. Estimated tax was paid with an extension request. ($175,000.00 version and $119,000.00 version)

4. Expenses incurred due to lost Nuveen certificate of ownership. (Accounting entanglements $169.26 and $20.00 )5. Decedent owned a partial interest in 15 acres of land in Accotink. The Harold O’Connell Trust owned the other share. The estate agreed to pay for the appraisal which hopefully will reduce the value of the tract by 50%. The beneficiaries of the Trust are the same persons as the devisees under the will and in the same shares. (Accounting entanglement using an imaginary $2,000.00)

6. When the 1991 income tax was prepared by Edward J. White, Co- Executor, a large capital gain was omitted necessitating the filing of an amended return. $526.55 was assessed in interest by the IRS. The figure is the amount of interest earned by the estate while the amount due the IRS was in the estate bank account. The balance of the interest assessment was paid by Edward J. White. (Accounting entanglement $241.81)

7. Jean M. Nader and Sheila O’Connell-Shevenell agreed that the vehicle should be disbursed to Anthony M. O’Connell in addition to his 1/3 share of the remainder of the estate. (Accounting entanglement using car as $8000.00 gift-estate tax interplay)

16. In addition, Mr. White timely requested an extension for

filing the decedent's last income tax return and therefore no penalties were involved. As justification for the delay, Mr. White points out that he experienced some delay in obtaining the K-1 from you and your own complaint appears to concede that there was a problem with getting the K-1 to Mr. White. 16

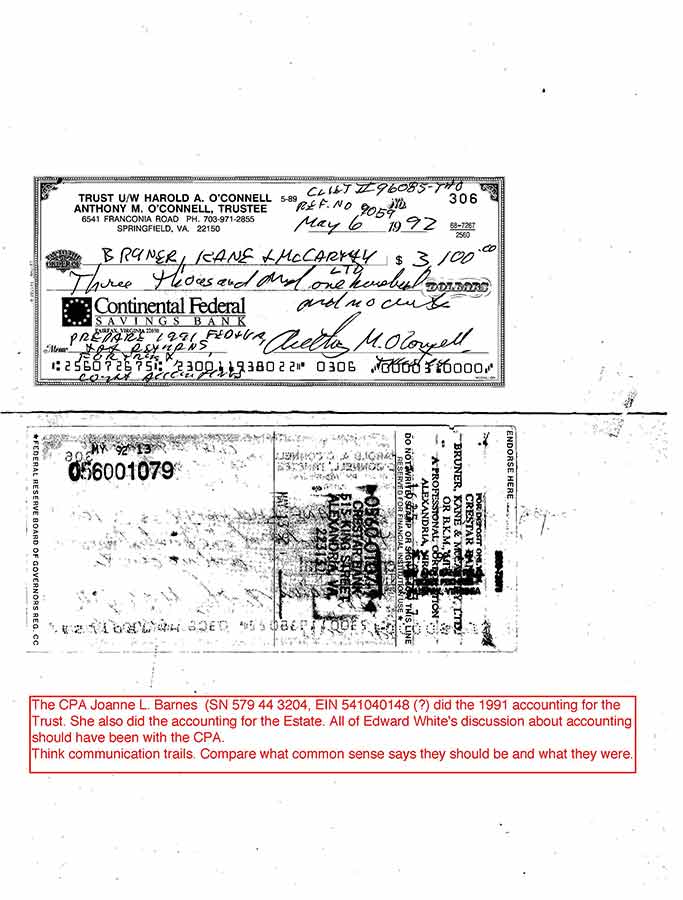

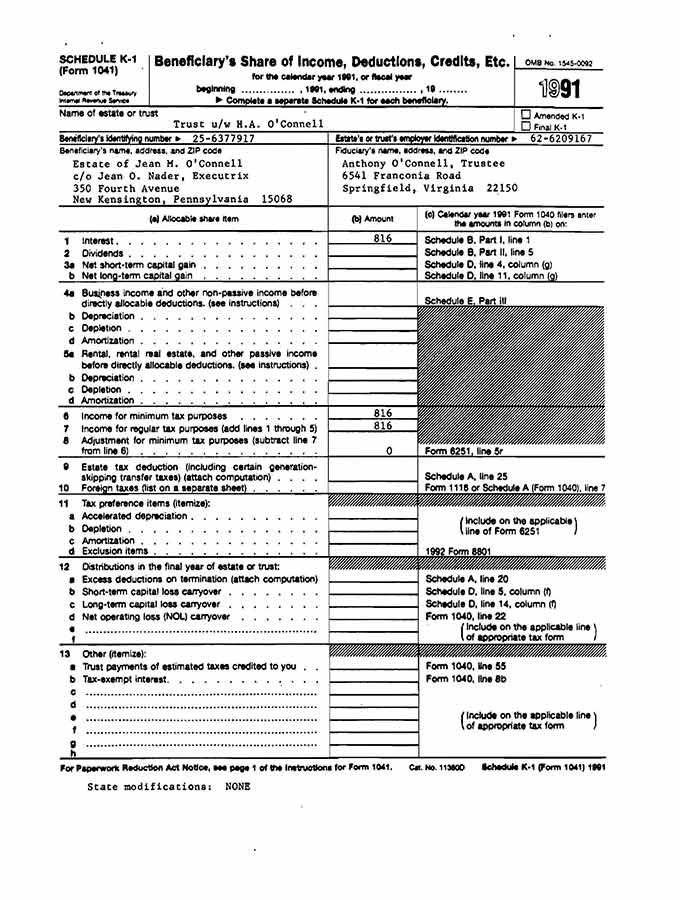

16 The CPA Joanne Barnes did the accounting for the Trust and the Estate. This would mean that the CPA was late in getting the K-1 to herself.

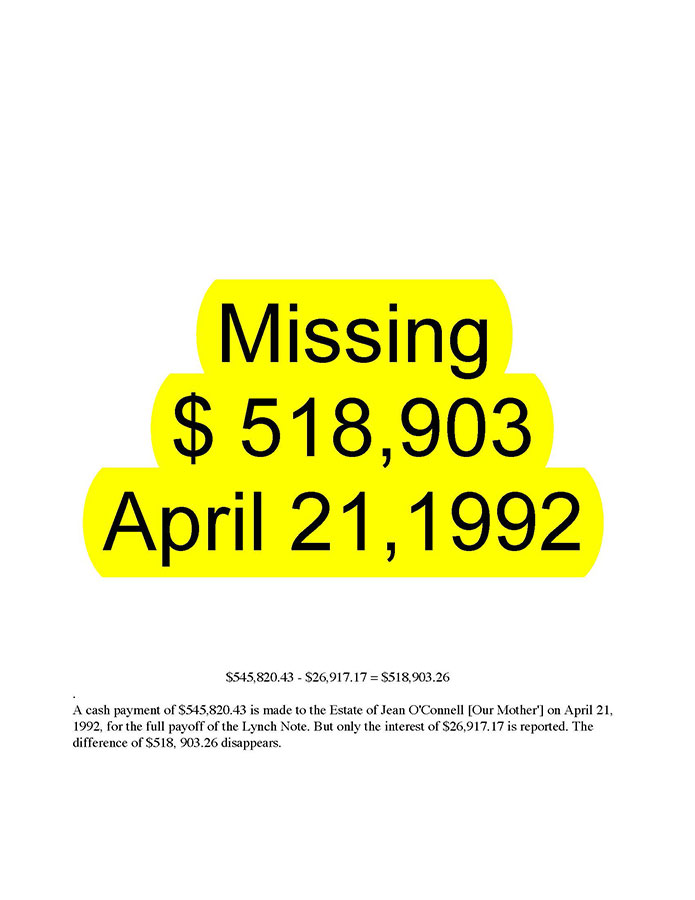

The AE (accounting entanglement) 1,475.97 - 816.00 = 659.97 covers the disappearance of $518, 903.26 (545,820.43 - 26,91717 = 518,903.26). History suggests the intent was to cover-up the dissappearance of the $518,903.43. That I'm made responsable for 1,475.97 - 816.00 = 659.97t, and the K-1 with its 816.00 further evidence to support that.

I believe these documents and transcripts are self explanatory. Basically, they frame me with the AE (accounting entanglement) 1,475.97 - 816.00 = 659.97. After I brought attention to the 659.97 its made to appear as if it doesn't exists. One indicator of its importance is the degree the Commissioner of Accounts and the B&K law firm cover it up. Small numbers are used to create accounting entanglements. as if the issue were the amount and not that they entangle. The issue is that they entangle.

See note 16

The AE 1,475.97 - 816.00 = 659.97 covers the 545,820.43 - 26,91717 = 518,903.26

1992.05.19 (Edward White to Anthony O'Connell, c/o E.A. Prichard, copy to Jean Nader)

"In your letter of May 6 to Jean you asked that I communicate with you with regard to the Harold O'Connell Trust.

I am trying to prepare the estate tax, and as usual in these cases, there are problems trying to understand the flow of debts and income.

I do have a few questions which are put forward simply so that the figures on the Trust's tax returns and accounting will agree with the estate's.

1. The K-1 filed by the Trust for 1991 showed income to your mother of $41,446.00. The Seventh Accounting appears to show a disbursement to her of $40,000.00 plus first half realty taxes paid by the trust for her and thus a disbursal to her of $1794.89. If these two disbursals are added the sum is $41,794.89. This leaves $348.89 which I cannot figure out. It could well be a disbursal of principal and not taxable.

2. The K-1 filed by the Trust showed a payment of $816.00 in interest to the estate. You sent a check in the amount of $1475.97 to the estate. What was the remaining $659.97? Do I have this confused with the tax debt/credit situation which ran from the Third Accounting?

3. On the Seventh Accounting "Income per 7th Account" is shown as $5181.71, but I cannot figure that one out either.

I am of the opinion that the estate owes the trust for the second half real estate taxes from September 15, 1991 through December 31, 1991 in the amount of $1052.35. This is shown on your accounting a disbursed to the heirs. Should this be paid back to the heirs or to the Trust?

I believe that the income received from the savings accounts from September 15 to the date the various banks made their next payment to the Trust (9/30 and 9/21) should be split on a per diem basis, since the Trust terminated on her death. This will be a small amount of course.

Are there any other debts which your Mother owed the Trust?

I realize that Jo Ann Barnes prepared this and if you authorize it I can ask her to help me out.

Please understand that I have no problem with the Accounting, I m just trying to match things up. In the long run, since the beneficiaries are the same, the matter is academic. Please send the bill for the appraisal whenever you receive it. Jean is filing the Fairfax form for re-assessment in her capacity as a co-owner in order to give us a better basis to get this assessment changed and to meet the county's deadline. It will state that the appraisal you have ordered will follow. I think this will be to all of your benefit in the long run.

Sincerely, Edward J. White"

2000.08.08 (Jesse Wilson's Report to the Judges)

"To the Honorable Judges of Said Court:

RE: Estate of Harold A. OConnell, Trust

Fiduciary No. 21840

1. By a Tenth Account duly filed herein and approved by the undersigned on August 25, 1995, the trustee herein, Anthony M. 0'Connell, properly accounted for all of the remaining assets reported as being assets of the trust created by the will of Harold OConnell and reported a zero balance on hand. A copy of said account is filed herewith as Exhibit 1.

2. By an Eleventh Account, Anthony M. OConnell, trustee, again reported zero assets on hand and no receipts or disbursements. A copy of said account is filed herewith as Exhibit 2.

3. Both the Tenth and Eleventh accounts carried the notation "This is not a final account".

4. In the ordinary case, an account which shows the distribution of all remaining assets is filed as a Final Account, and its approval terminates the fiduciary's responsibility to the Court and permits the Commissioner of Accounts to close the file.

5. The said trustee has also filed a Twelfth Account in which he reports as an asset $659.97 "due from the Estate of Jean M. OConnell". A copy of that "account" is enclosed herewith as Exhibit 3.

6. The Estate of Jean M. OConnell, deceased, Fiduciary No. 49160, was closed in the Commissioner of Accounts office after approval of a Final Account on May 31, 1994.

7. The said $659.97 was the subject of correspondence between the said trustee and Edward J. White, attorney and co-executor of the estate of Jean M. OConnell, copies of which are attached hereto as Exhibits 4 and 5. In his letter,

Exhibit 5, the trustee explains that the $659.97 is part of a net income payment of $1,475.97 which the trust owed the estate of Jean M. OConnell. In that same letter, the trustee states that "At this point in time, I believe Mr. Balderson and I are of one mind that the estate does not owe the trust and the trust does not owe the estate".

Mr. Balderson was a CPA for the estate. Both of these letters were provided to the Commissioner of Accounts by the trustee in support of his "Twelfth Account".

8. The trustee also provided the Commissioner with a copy of a page from a "Jean M. OConnell estate tax analysis" which shows $659.97 under "Assets" of that estate as "Debt from Harold OConnell Trust". A copy of that page is attached as Exhibits 6.

From a review of this information the Commissioner finds that there is no evidence to support an assertion by the trustee that the $659.97 is an asset of the trust. To the contrary, it appears that either it is not a debt at all, or, from the estate's point of view, it was money owed by the trust to the estate, i.e. an asset of the estate of Jean M. OConnell. That estate has been closed for more that six years.

Accordingly, the foregoing Eleventh Account of Anthony M. OConnell, Trustee has been marked a "Final Account" by the undersigned and is hereby approved as a Final Account in the trust under the will of Harold A. OConnell and is filed herewith.

In the event that the trustee is successful in recovering $659.97 or any other funds which are proper trust assets to be accounted for, such may be reported to the Commissioner of Accounts by an Amended Inventory and, thereafter, accounted for by proper accounts.

GIVEN under my hand this 8th day of August, 2000.

Respectfully submitted,

Jesse B. Wilson, III

Commissioner of Accounts

Fairfax County, Virginia

JBW:jcs

Enc.: Exhibits, 1 - 6

cc: Anthony M. OConnell, Trustee"

(See the exhibits in the pdf reference)

delinquent 12th account 8p

my actual 12th account 22p

From the Complaint against me prepared by the B&K law firm (above).

http://www.canweconnectthedots.com/plant659/plant659-home.html

17. Based on the foregoing, I see no basis in fact or in law to conclude that Mr. White has engaged in any misconduct in violation of the Code of Professional Responsibility. Therefore, please be advised that no further action will be taken on your complaint.17 By copy of this letter to Respondent's counsel, Mr. Rosenfeld, I am advising him of my determination.

17 The CPA and lawyer makes money disappear and cover it up by dividing and destroying the family they victimized. The evidence for exposing accounting fraud is in exposing the accounting. Expose the accounting trails at http://www.book467page191money.com and see how much money disappeared. Then things will fall into place. There is a reason those in control won't allow exposure. There is a reason these accounting trails have been concealed since they were entered into the public Court records in 1993. complete accounts 24p

Very truly yours,

James M. McCauley

Assistant Bar Counsel

JMM/ge

cc: David R. Rosenfeld, Esquire"

Reference

Anthony OConnell mail

Anthony OConnell mail 87p

Virginia Bar mail

Virginia Bar mail 7p

Sales contract 15p

This concerns the two lawyers for one family scam. Lawyer 1 hides. Lawyer 2 is hired because other family members don't know there is a lawyer 1. In our family lawyer 1 was Mr. Edward White. Secrecy is difficult to document:

The CPA Joanne Barnes never mentions Mr. White in her mail. mail-joanne-barnes

The lawyer Edward White never contacts me until 1991. mail-edward-white

The lawyer Henry Mackall never mentions Mr White in his mail until May 8, 1986. mail-henry-mackall

Our Mother Jean O'Connell never mentions Mr. White in her mail. mail-jean-oconnell

Anthony OConnell doesn't mention Edward White until sometime after May 8, 1986.

mail-anthony-oconnell

1992.12.03 (Anthony

O'Connell

to Virginia State Bar)

"I am writing to register several complaints about Mr. Edward J. White, an attorney practicing in Virginia. Over the past seven years, Mr. White represented my mother [Our Mother's intent was for our whole family] the on numerous occasions, he was hired by me [To represent all of our family] on one occasion, and he is now acting as co-executor with my sister on my mother's estate. I am a beneficiary of that estate.For seven yeayrs I have tried to understand why I became alienated from my mother after trying to work with Mr. White in funding a trust created by my father's will. After going through my mother's papers after her death in September, 1991, and initially experiencing that same alienation from my sister as she worked with Mr. White as co-executor, I now feel I understand these dynamics.

I will give a brief summary of my complaints and then provide the details of each one.

My first complaint arises from Mr. White's withholding of information in the funding of a trust established by my father's will, and in his defamatory and divisive statements about me to my mother. My mother was executrix of my father's will and at some point hired Mr. White to help her. My second complaint concerns Mr. White's conduct after I hired him in 1987 to handle the closing of a $1.41 million real estate sale. Mr. White repeatedly failed to return my telephone calls and failed to inform me of critical issues. The day before closing, Mr. White informed me he was not representing me and, when I suggested we postpone the closing until I had time to review the settlement documents he had written and that I had just read, he threatened to force me to go to settlement the next day. No justification was given.

My third complaint arises from Mr. White's withholding of information, his defamatory and divisive statements about me to my sister, and his performance as co-executor of my mother's estate.

First Complaint.

My first complaint arises out of events surrounding the funding of a trust (fiduciary # 021840) established by my father's will. My mother was executrix of my father's will and at some point hired Mr. White to help her. I felt Mr. White purposely withhold information from me, and in the created confusion, presented a negative image of me to my mother with divisive and defamatory accusations and threats. During this period my mother dropped me from her will as co-executor and added Mr. White. Mr. White also writes, with a copy to my mother, that he may have to seek to remove me as trustee (enclosure 4).

The general situation was that: (1) I lived in Missouri; (2) I did not know the procedures for being a trustee in Virginia; (3) Mr. White and my mother were not answering my questions and (4) for some reason still unknown to me, no one told me my responsibility about the trust for the first ten years after my father died. I was concerned about Mr. White's unwillingness to give information. It was not supposed to have been an adversarial situation. In view of the above, I hired an attorney, Mr. Mackall, and among other things asked him to send me a draft copy of what the estate was going to distribute to the trust.

The letters listed on the left column below relate to my requests for estate filings. Mr. White's letters are listed in the right column below. I initially requested a copy of the final estate accounting on December 9, 1985, and I believe I received a draft copy several days prior to June 20, 1986, the date the trustees qualified. I can not find a dated letter to be more exact, but I remember coming to Virginia to qualify as trustee immediate after the receipt of that information.

Request for estate filings

August 16, 1985 (enc. 6)

December 9, 1985 (enc. 7)

February 20, 1986 (enc. 8)

June 15-18?, 1986, I received draft copy (enc.8.1)

June 20, 1986, trustees qualified

July 1, 1986 (enc. 9)

August 11, 1986 (enc. 10)

Mr. White's letters

January 24, 1986 (enc. 1)

January 27, 1986 (enc. 2)

April 10, 1986 (enc. 3)

April 25, 1986 (enc. 4)

May 27, 1986 (enc. 5)

I believe my letters show I was not the cause of the delay. I received the information I requested approximately six and one half months after I asked for it. During this six and one half month period, Mr. White wrote these letters to my mother:

1. January 24, 1986, letter to my mother (enclosure 6):

"I spoke to Mr. Mackall on January 22nd as to the causes of the delay in obtaining the agreement from your son.

"He stated that he had several discussions with your son and they ironed out some minor details, and that the agreement being sent to Anthony to be signed on that date."

2. January 27, 1986, to my mother (enclosure 2):

"At long last we have a signed Agreement concerning the funding of the Trust. The Agreement is enclosed."

"Mr. O'Connell was unwilling to agree to pay interest on the real estate tax advancements. While I am at a loss to understand his attitude, I am of the opinion that we would be best served by signing the Agreement as is."

Mr. White knew my mother received the net income from the trust and any interest to her would be a deducted expense from her net income from the trust. The numbers would "wash". He makes it seem as if I had no rational reason for such a position.

I was never comfortable with the Agreement but, went along with it.

I felt the proper document funding the trust should be the customary final estate filing, as it was a continuation of the ten year audit trail of the assets in my fathers estate.

3. April 10, 1986, to Joanne Barnes, my mother's C.P.A., copy to my mother (enclosure 8):

"I have agreed with Anthony O'Connell's attorney that we will provide them with a draft of the final accounting in the Harold O'Connell Estate. This, I think, will allay all of the suspicions that have arisen on the other side in this matter." (My underline.)

I think Mr. White is aware that withholding information causes suspicion.

4. April 25, 1986, to Mr. Mackall, copy to my mother (enclosure 9).

"If he does not agree or requests further delaying tactics, I feel that I have no other recourse in serving my client than to seek to have him removed as a Trustee. This matter is costing Mrs. O'Connell dearly with the delay."

5. May 27, 1986, to the Commissioner of Accounts, copy to my mother (enclosure 5). (Mr. White is asking for an extension on the delinquent estate account of my father who died in 1975.) "However, the will established a trust and Mrs. O'Connell's son has been most difficult in coming to terms on qualifying as trustee of the trust. Both Mr. Henry Mackall, who represents the trustee, and I have been working diligently on this case."

I believe Mr. White is blaming me for the estate filings being late here. I think it is ironic that no one accused me of "delaying tactics," "causing delay," or being "most difficult in coming to terms" during the ten years I did nothing about the trust because I was not told of my responsibilities. I only found out about the trust because, while visiting my mother, she showed me a May 8, 1985, letter to her from the Commissioner of Accounts (enclosure 11). I began to realize my responsibilities after I took this letter to the Commissioner of Accounts and I asked him what it meant. She later received a summons (enclosure 12). I don't know when my mother first contacted Mr. White about my father's estate, but if it had been for some time, I believe Mr. White should have notified me since I was designated trustee of the trust made by my Dad's will.

The codicil to my mothers will removing me as co-trustee and adding Mr. White was signed September 20, 1985. Most of the written documentation I have been able to obtain occurs after that date. I have no idea what Mr. White told my mother in private conversations. I can only guess from what this experienced attorney left in writing. I believe his agenda was not radically different from him wanting to remove me as trustee (enclosure 4).

Second Complaint.

My second complaint concerns Mr. White's conduct after I hired him to handle the closing of a $1.41 million real estate sale I made. If the reader wonders why I would hire an attorney who operated as I described in my first complaint above, it's because I did not understand then why things were not working. I discovered the defamatory and divisive letters about me to my mother only after her death in 1991. I believed that my goodwill of handling the sale myself and saving the expense of the realtor fee on the 1.41 million dollar sale price would generate goodwill from others. I also believed in my naivete, that if Mr. White worked with me, he would realize I was a good man and the suspicion and mistrust would stop. All the information about the sale would be available to everyone and we would all have the same goal in bringing it to a successful conclusion. For lack of other information or motivation, I still believed the years of grief beginning in 1985 were due to misunderstandings caused by separate lawyers and miss communication or no communication.

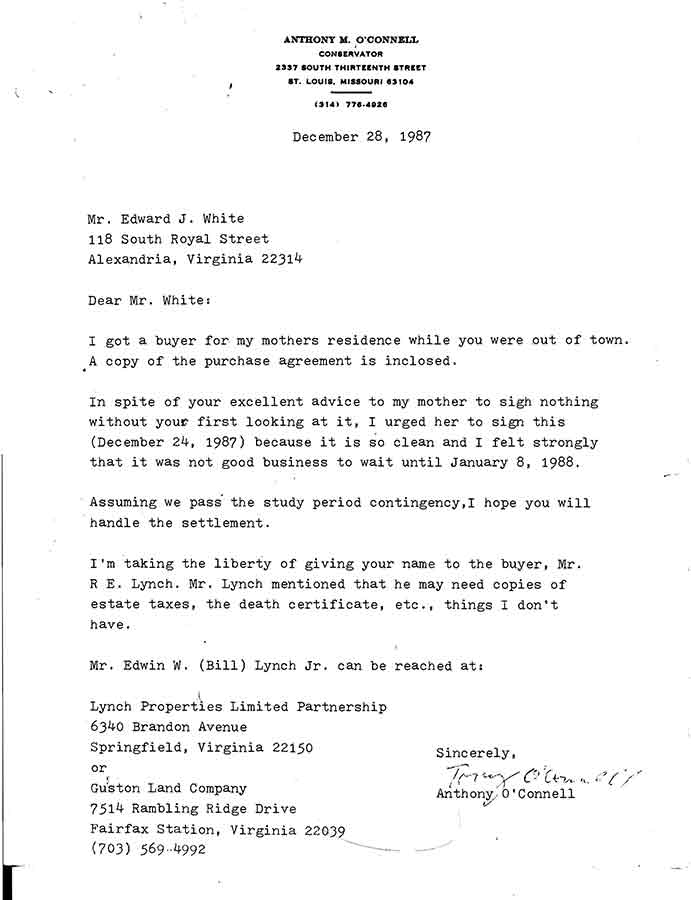

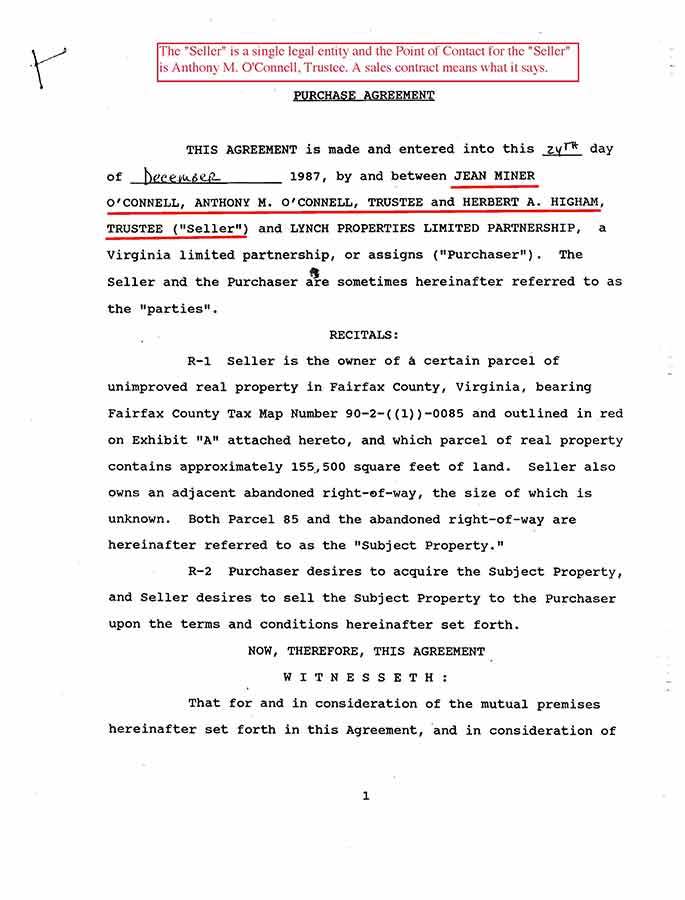

The events occurred as follows. On December 28, 1987, I sent a letter to Mr. White asking him to handle the closing of a real estate sale I made of my mother's residence (enclosure 13). I owned in fee simple a portion of this real estate in my capacity as trustee for a trust established by my father's will. In my letter,

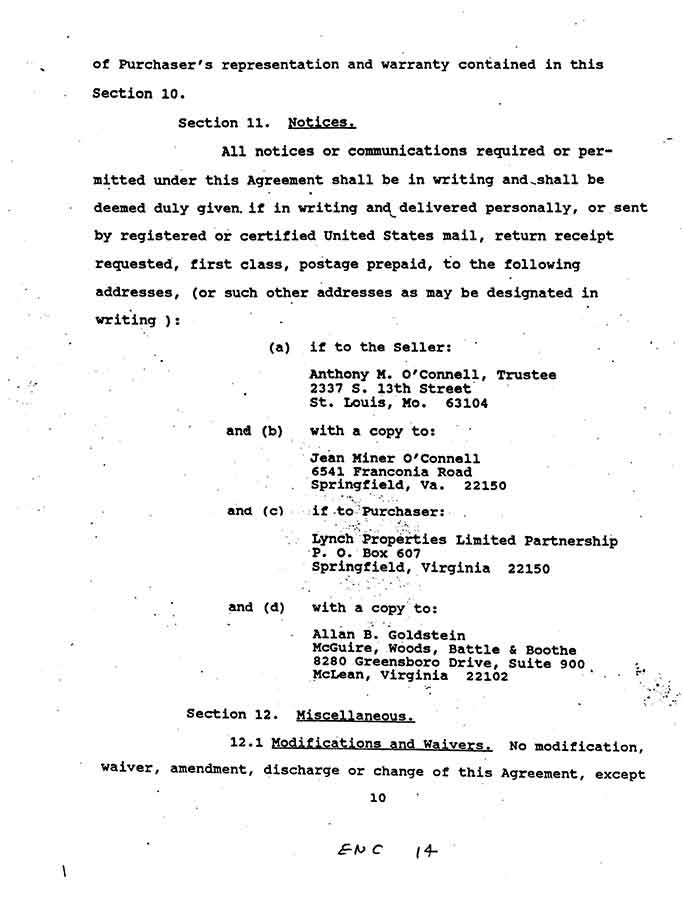

I mentioned that I was giving his name to the buyers and I enclosed a copy of the sales contract. After I did not hear from Mr. White for some period of time, and he did not respond to my telephone calls, I visited his office (I do not know whether that was during my January 25-29, 1988, visit or my March 11-13, 1988, visit toVirginia). He said he did not have a copy of the sales contract. When I got back to Saint Louis, I sent him another copy. I never heard from Mr. White again until I walked into his office the day before closing. As the seller and negotiator of the sales agreement, and the person who hired Mr. White, I assumed he realized I wanted to be kept informed about the matter. It was even written into the sales contract that: "All notices or communications required or permitted under this agreement shall be in writing . . . and delivered personally, or sent . . . to the following addresses .: (a) if to the Seller: Anthony M. O'Connell, Trustee, 2337 S. 13th Street, St. Louis, Mo. 63104 . . ." (enclosure 14)

By late March, I was reduced to the embarrassing position of asking the buyer for information. On April 15, 1988, I received a copy of a letter from the buyer's law firm saying that settlement would be in six days (enclosure 15). That was the first/information I had received since the day I hired Mr. White. I don't believe even one of the dozens of telephone calls I made to Mr. White during this three and a half month period were returned.

The day after I received the closing notice from the buyer, I left Saint Louis for Virginia. After arriving, I left more telephone messages in Mr. White's office saying I had come from Saint Louis for the closing and would like to meet with him. Again, none of my calls were returned. The day before the scheduled closing, I exercised my last option and walked into Mr. White's office. On that day, I found Mr. White in his office. He allowed me to read the documents he had prepared for settlement. To my surprise, I discovered that without asking me, he had written in himself and someone I did not know as trustees on the Deed of Trust. Mr. White also informed me that he was not representing me. I was shocked. I suggested to Mr. White that settlement be postponed until I had time to think about the consequences of these surprises, and so I could consult with my co-trustee, f-er-the property. Mr. White informed me that he would force me to go to settlement the next day. At that point, I realized the attorney I had entrusted with my $1.41 million sale had taken advantage of that trust, and he did it under the cover of pretending to represent me. I was in shock.

I felt I had been set up and locked in. I wanted a trustee I could trust. Living in Saint Louis, I did not know of a good substitute trustee who was a Virginia resident. Until I walked into Mr. White's office, I did not even know one was required. I had trusted that the attorney I had hired to represent me would tell me these things in adequate time to plan for a successful closing. If I tried to postpone the settlement to hunt for a substitute trustee, Mr. White threatened he would "force" me to go to settlement. I did not know what this "force" involved, but I was intimidated.

I also felt a big conflict between the two sellers over who would be trustee on the note could be disastrous in negotiations with the buyer at closing. As it was, the negotiations at settlement took over four hours. One reason for this was that my co-trustee discovered that the notes from the buyer were non-recourse to the limited partners although the sales contract had specified that the sale was to be recourse to the limited partners. This was a significant issue and one that Mr. White either apparently hadn't realized or chose not to tell me about.

I felt Mr. White put his personal interest first, of being trustee with a 5% commission on two notes to a Limited Partnership with a combined face value of $1,161,287.37, and he put the success of the sale in jeopardy by doing so. For the reasons given above I agreed at closing for Mr. White and his other party to be trustees on the Deed of Trust.

While visiting my mother several years later, she told me Mr. White had died. With my mother in the room, and at the request of my mother's retirement home, I called Mr. White's office to inquire about the status of the Power of Attorney that my mother had executed authorizing Mr. White to act for her. To my surprise, Mr. White answered the telephone. At this unexpected opportunity, I asked him why, back in 1988, he had not responded to my telephone calls and letters asking for information concerning the upcoming settlement. Incredible and embarrassing as it seems to me now, I still believed it was mostly misunderstanding and I jumped at this unexpected opportunity to clear something up that had poisoned my relationship with my mother. Mr. White followed up the conversation with his letter of March 15, 1991, (enclosure 16):

"In regard to your inquiry as to why, in 1988, there came a time when I refused to deal with you on the sale, as I said, I recalled that a conceivably adverse relationship had developed between you and your mother concerning the sale. 1 call your attention to the sixth paragraph in your letter to her of December 8, 1987, a copy of which is enclosed."

The sixth paragraph of my letter states (enclosure 17):

"I am disappointed that you apparently do not want me involved in this transaction. As near as I can determine, you are concerned that I will block the sale. Please tell me of your specific concerns and maybe we will all have a more pleasant and successful experience." I fail to see the logic in Mr. White's substantiating his refusal to disclose settlement information to me because of paragraph six of my December 8, 1987, letter to my mother. She had called me on December 7, 1987, to tell me she had to sell the house within six weeks to get her share of the money to buy into a retirement home, and that I was not to come because "people here" were going to take care of selling the house. To this day I do not know why she apparently did not want me involved in the sale of the house. I think most people would read paragraph six and interpret it in the manner that I intended it--that is, to try to find out her concerns as to why she wanted to exclude me. I resorted to guessing in hopes that it would be a catalyst to get her to talk. I do not consider my letter to my mother to have been adverse.

Please compare these two letters and their intent. I believe my letter shows my intentions; to keep everyone informed (copy to four people) and to try to resolve a problem. I believe Mr. White's letter shows his intentions; to deliberately mislead a seventy-nine year old woman into thinking she should not trust her son.

Moreover, if Mr. White thought an adverse relationship had developed between my mother and me, and that adverse relationship prevented him from representing me, why didn't that same rationale prevent him from accepting my hiring of him three weeks later to handle the closing? He could easily have suggested that I obtain other counsel. Why did it not prevent him from naming himself as trustee on both the note to the estate and the note to the trust? Moreover, even if Mr. White was not representing me, he still had an obligation to keep me informed under the terms of the sales contract (enclosure 14).

Mr. White did send the deed and the documents to my address in St.

Louis, but they did not arrive until after I had left. The cover letter is dated April 16, 1992 (enclosure 17.1). If you consider the timing, it tended to limit my options to either staying in Saint Louis to receive the documents and agreeing to everything Mr. White wrote, or attending the closing in person in Virginia on April 21, 1992. If I had not walked into his office the day before closing, I wonder when I would have found out Mr. White was not representing me?

I believe if someone hires an attorney to represent them and that attorney accepts, a certain level of trust has to be given that client. It is a fiduciary relationship. At that point in time, I did not think it necessary to get Mr. White's acceptance in writing. If the attorney then works in secret and at the conclusion says he is not representing the client that hired him, I feel it is an abuse of the fiduciary trust. I feel it is a license to steal.

Third Complaint

My final complaint arises from Mr. White's withholding of information, his defamatory and divisive statements about me to my sister, and his performance as co-executor of my mother's estate (fiduciary #49160, her SSN 230-50-6044).

The first conflict occurred when I asked Mr. White in my letter of March 30, 1992, for verification of who would get my mother's Plymouth Van and at what cost (enclosure 18). Because of my experience in hiring Mr. White to handle the closing of my sale described above, I felt it prudent to get the understanding in writing from him.

Perhaps I did underestimate the complexity of paying off a car loan, but I think Mr. White's response of April 4, 1992, with his

"I do not know what your problem is, but in the future, please address all correspondence to Mrs. Nader", typifies the problem I am trying to describe (enclosure 19). Because Mr. White was not willing to respond with something such as "The actual cost of the Plymouth to you would be xxx dollars," the consequences were:

1. I had to write a second request to Mr. White (enclosure 20). Mr. White did not respond.

2. I had to write a third request to my sister (enclosure 21).After I wrote this letter, I felt it was inappropriate for Mr. White to try use my sister to explain what he may or may not do. Although both were co-executors, it was Mr. White who was calling the shots and the one I did not trust.

3. My sister had to write a letter to me (enclosures 22)

4. My sister and I had several unsettling telephone calls.

5. I had to make a judgement on my own and prepare my own receipt with the information I was able to get from Mr. White (enclosure 23).

6. Mr. White send an agreement to my sister about the car which "cannot be any clearer". He never mentions the contents of the agreement nor the fact of this agreement to me (enclosure 24).

Mr. White makes numerous threats to me in this letter. He mentions that he will seek my sister's approval to file suit against me for an accounting.

7. My sister tells me Mr. White is withholding my $75,000.00, and will continue to hold it, until I sign the receipt just as he wrote it. If I have to sue Mr. White to get my distribution, I also have to sue my sister, since she is a co-executor.

8. I hire an attorney. I receive my $75,000 distribution from Mr. White in the mail May 16, 1992, with no explanation.

9. After I get proper information from my attorney, I write my sisters with the appropriate legal form to resolve the problem (enclosure 25).

10. I have to write a clarifying letter to my sisters (enclosure 26) .

11. By May 15, 1992, both my sisters sign the form and I sign and send to Mr. White the receipt as he wrote it.

12. The extra paper work, the time, and having to hire an attorney is insignificant compared with all the bad feelings, suspicion and mistrust that was generated between me and my sister.

When I compare the time and effort that would have been required for Mr. White to write one letter specifying the dollar cost of the Plymouth to me, with the time, effort and angst represented above, I believe problem resolution was not Mr. White's intent. I believe Mr. White had a responsibility to explain the matter to me to the extent necessary so that I could make an informed decision regarding the matter. As was the case with my mother, I feel Mr. White's propensity to withhold information generated mistrust and damaged the relationships within my family.

As was the letters Mr. White sent to my mother, the letters he sent to my sister also present a negative image of me with divisive and defamatory accusations and threats.

1. May 4, 1992, letter to my sister (enclosure 27). My sister was good enough to sent me a copy of this.

"If we have knowledge of a gift to Tony of $15,000, we must report it. Tony is going to have to answer that question before we can be satisfied. If he claims he did not receive the money, he will have to supply us with an affidavit to that effect."

My mother's 1988 tax return shows this gift. After reading this, I requested a copy of the Form 709 from my mothers accountant (enclosure 37) and forwarded it to Mr. White (enclosure 36) when he first asked me about it eight weeks later (enclosure 35). Why accuse me before checking the returns?

"With regard to the filing of the income tax return, my file indicates that I received a fax copy of the K-1 from the Harold

O'Connell

Trust on April 9, 1992, only six days before the tax return was due."

I had asked the accounting firm to send out the K-1's earlier. When

I followed up on this later I discovered that they had inadvertently been left sitting on the receptionist desk. I mailed them myself. The accountant had consultant with Mr. White on these same K-1's in March. If Mr. White wanted it earlier, he could have called me or the accountant. Mr. White fails to tell my sister that the K-1 is not due until April 15, 1992.

2. April 22, 1992, letter to my sister (enclosure 24). My sister was good enough to send me a copy of this also.

"In order to file that return and the subsequent Fiduciary income tax return we will need an accounting from Tony from the date of his last accounting to the date of death. If he does not want to prepare it, I will not agree to any preliminary disbursal to him at all, and will seek your approval to file suit against him to compel the accounting, plus damages to the estate for his delay. Since that trust terminated on your mother's death, his final accounting is due now and not in October."

"There will be no further explanations or written entreaties to him as far as I am concerned. He has the duty and he will perform it under a court order if necessary. Of course he will furnish that receipt."

The Commissioner of Accounts tells me the trust account is due their office October 20, 1993 (enclosure 28). Mr. White never told me he thought an account was due "now". He is asking my sister to join him in suing me for something he never asked me about. I believe I sent Mr. White a copy of that account around May 12, 1992. I am not required to send him any account.

The Commissioner of Accounts Office and my attorney tell me that

Mr. White and the estate have nothing to do with the trust. The trust is not required to give any special accounting to the estate at any time. Just because the net income of the trust was distributed to my mother does not mean he is owed a special accounting. Similarly, he is due no special accounting from banks or brokerage firms from which she received income.

If Mr, White genuinely doesn't know how trust work, he should know his limitations before setting up family members to sue each other.

He could find this information by talking to most any clerk in the Commissioner of Accounts Office.

"In the event that we do seek a reduction in the assessment Tony will be given written notice that his prompt cooperation is necessary and that if he fails to cooperate that he is aware of the adverse consequences to the estate and is responsible for them."

The situation is that the trust and the estate each own a portion of fifteen acres of unimproved land. The estate can do anything it wants to with it's portion without any approval or "cooperation" from the trustee. The estate and the trust are legally separate. I have never been able to convince Mr. White that he and the estate have authority over the trust.

Again, I am threatened behind my back for some unknown. I would like to know, in writing, from Mr. White, exactly, what "cooperation'' is required before I suffer the adverse consequences.

This is what did happen. About mid May, out of the blue, I was sent a county form that had to be completed in something like two weeks on which the valuation of the 15 acres would depend. I wanted no part of it for fear of getting sued for something.

My sister told me Mr. White said a formal appraisal of the land would cost $7,000.00 to $7,500.00 and the earliest he could get an appraiser was in October. The first two people I called said it would cost about $2,000.00. I hired an appraiser who completed the appraisal within three weeks after I called him, he charged me $2,000.00, he appraised the property for half the county's valuation and the County accepted this 50% reduction (enclosure 42). I sent a' copy to Mr. White June 8 or 9, 1992. I paid the appraiser from the trust. I did this because I was told the earliest Mr. White could get an appraiser was 11 months after my mother's death. I would like to know why Mr. White's appraisers are 350% to 375% higher than the market rate I found and why they could not get to it for five more months. The trust has absolutely no responsibility here. I did it because Mr. White was not getting the job done. Not only did I have to do the estate's work, I had to write and request proper reimbursement from the estate. I believe Mr. White put my sister up to what she told me:

"Since the trust was supposed to terminate on Mother's death, the $2000.00 for the appraisal should be paid to the beneficiaries, not to the trust. The checks from Sheila and me can then be paid back to you" (enclosure 29).

I can not imagine trying to explain this scenario to a tax preparer. Who is delaying, who is not cooperating, who should be sued for damaging the estate? Again, if Mr. White genuinely doesn't know how trusts work, he should be aware of his limitations before setting up family members to sue each other. Trusts, like estates, stay open until the paper work is done. Mr. White could find that out by talking to most any clerk at the Commissioner of Accounts Office.

I have been advised that my mother's estate is a simple one, cash, one vehicle, stocks and bonds, and a Deed of Trust with two notes voluntarily paid off in full on 4/21/91.

I agree with Mr. White that anyone damaging the estate should pay for those damages. Even though Mr. White is serving without surety, I feel he, as co-executor of my mother's estate, is at least as responsible to it as he has held me, a beneficiary and trustee with zero responsibility to the estate except to send a K-1. I believe my mother's estate has been damaged by Mr. White's co-executorship, a co-executorship that he refused to relinquish at the request of all the beneficiaries (enclosure 30).

1. Mr. White's initial filing of my mother's 1991 individual tax return was liable for penalties for underpayment of estimated taxes. I was particularly interested in this because I felt Mr. White had convinced my sister that it was my fault. My request for information about this was never answered (enclosure 31).

2. Mr. White failed to notice a 4/21/91 payment of $125,000.00 to my mother in 1991. After I brought it to his attention that 79% of this was taxable, he amended her Federal and Virginia returns. Mr. White then asks my sister to limit his responsibility to half of the $526.55 interest on the 1040 because of the interest earned in the estate by his non payment (enclosure 32). Something is not quite cricket here. Mr. White is not a beneficiary. Why should he profit from his under payment of my mother's taxes. If this is accepted, shouldn't Mr. White compensate the estate for lost interest because of his over payments? For example, his estate return shows an overpayment of $70,050.51 (enclosure 33).

3. Because of the new Clinton/Gore administration, I felt the beneficiaries would most probably save taxes if all possible distributions could be made by December 31, 1992. December is the last month the beneficiaries can make tax deductible disbursements.

All three beneficiaries own and operate their own business. That can't be done because the IRS has not yet concurred with the reduced valuation of the real estate (enclosure 39). If Mr. White had filed the estate return on time this probably would not have been an obstacle. The beneficiaries lost this option to manage their personal and business finances.

According to Mr. White's extension request of June 11, 1992, the delay was due to (1) value of real estate not determined, and (2) "The estate does not at this date possess full data for certain gifts and debts of the estate and other needed information" (enclosure 34).

I put a formal appraisal of the real estate in Mr. White's hands approximately three weeks (mailed June 8 or 9, 1992) after learning he had made no progress on this issue in the eight months after my mother's death, and that the earliest he could get an appraiser would be an additional five months. That is thirteen months.

Mr. White never asked me about my gifts until July 16, 1992 (enclosure 35). 1 responded the next day (enclosure 36). Who is delaying and damaging the estate?

4. Mr. White withheld my distribution of $75,000.00. I had to hire a lawyer to get it and he was a Godsend (enclosure 38). 1 believe my sister consulted with this attorney and got another perspective. Mr. White has been very polite since. I feel a beneficiary should not have to hire an attorney to protect himself from his co-executor. I estimate that the cumulative costs for this attorney approach one thousand to several thousand dollars. Should the beneficiaries have to pay this or should the person who created the problem?

5. In Mr. White's letter of April 22, 1992, to my sister (enclosure 24), he says he will have to bill the estate for outside advice as to whether or not any of the trust under .my father's will is involved in the estate. I feel the beneficiaries should not have to pay extra for that level of knowledge. Most any clerk in the Commissioner of Accounts Office could tell him this.

6. What amount of damage is done to me and my mother when my mother believes the things Mr. White wrote about me? What is the amount of damage done when my mother drops me as her co-executer and adds Mr. White? Why did her feelings change?

7. What amount of damage is done to me and my sister when my sister accepts that m may have to sue her and her me?

8. In casual conversation with my sister several weeks ago, it dawned on me that Mr. White thinks the $545,820.42 Lynch payment of 4/21/92 to the estate is tax free and he writes a letter to that effect 11/13/92 (enclosure 39). I respond with my letter of November 16, 1992 (enclosure 40). Thirteen months after my mothers death, he doesn't know this instalment sale is taxable? I believe most first year accounting students would know this. What damage is caused the by this lack of tax planning and inattention?

I want to try to put in perspective Mr. White's performance on this one issue of the Lynch Deed of Trust. Mr. White was coauthor of the Deed of Trust with it's payment schedule and conditions, and made himself trustee.

a. In the spring of 1992 my sister reads to me over the phone her copy of Mr. White's letter to her informing the Lynches that they owe the estate $56,334.67 in interest on the note to the estate in 1992. He later learned the correct amount of interest was $45,067.74. I would think this mistake would raise Mr. White's consciousness enought to reread his own writing.

b. Mr. White fails to report the 79% taxable amount of the $125,188.17 Lynch payment on my mother's 1991 individual return. If I had not brought this to Mr. White's attention, how much more would the estate have suffered (enclosure 41)?

c. This month, eight months after the Lynch payment of $545,820.42 to the estate, thirteen months after my mother's death, I find out by accident that Mr. White is unaware that 79% of this $500,752.68 in principal is taxable. If I had not brought this to Mr. White's attention, how much more would the estate have suffered (enclosure 40)?

9. With this track record, I don't think it is unreasonable that I am concerned about possible damages on which I, as yet, have no information.

10. What is the cost of my time in trying to protect my mother's estate?

11. I believe Mr. White made problems when their were none, and made the simple complex.

In closing, the events of the past seven years have caused me incredible personal anguish. I'll never forget the night my mother called me in Saint Louis, and between sobs, said she had no one she could trust. She never explained it. She died six months later. The next day I received Mr. White's letter of March 15, 1991 of which a copy had been sent to my mother. Please be kind enough to read this letter (enclosure 24). I believe it shows Mr. White's intentions; to deliberately mislead a seventy-nine year old woman into thinking she should not trust her son.

My mother died apparently thinking I could not be trusted. What was her perception of me? She removed me as co-executor of her will in 1985 and added Mr. White. Why did she want me as co-executor up to 1985, but then changed her mind?

I respectfully request that you investigate this and that you ask Mr. White to produce real evidence that would justify his defamatory and divisive accusations to my mother and sister. When I asked him, he refused, saying "client confidentiality". I hope your investigation would include my performance as a trustee, and if I erred on the side of requesting too much information, I hope you would tell me so. I would welcome a written determination from you inorder to show my sisters, relatives and friends that Mr.

White's smears on my integrity were unwarranted. I ask that you take appropriate regulatory action against him so that others are protected from the emotional pain and suffering he has caused me and my family.

Have similar complaints been filed against Mr. White?

Sincerely, Anthony

O'Connell

"

Enclosures (44)"

(Insert Bars letter)