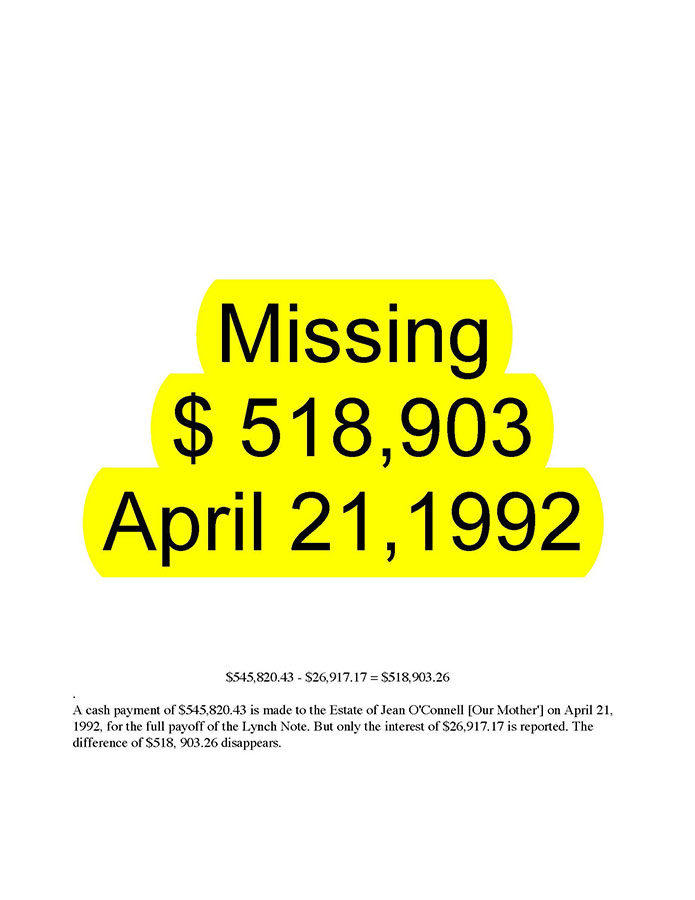

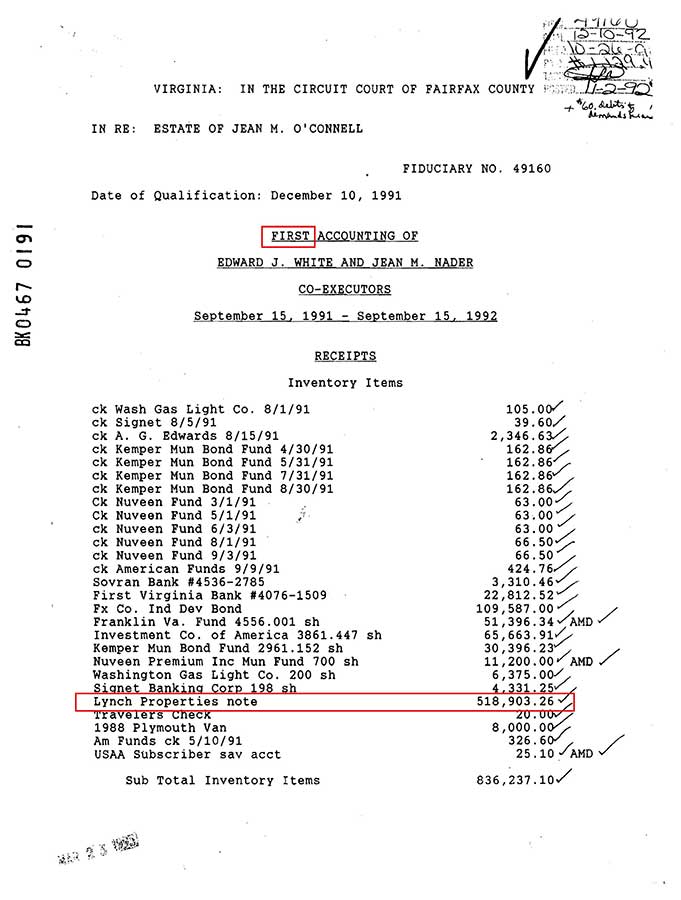

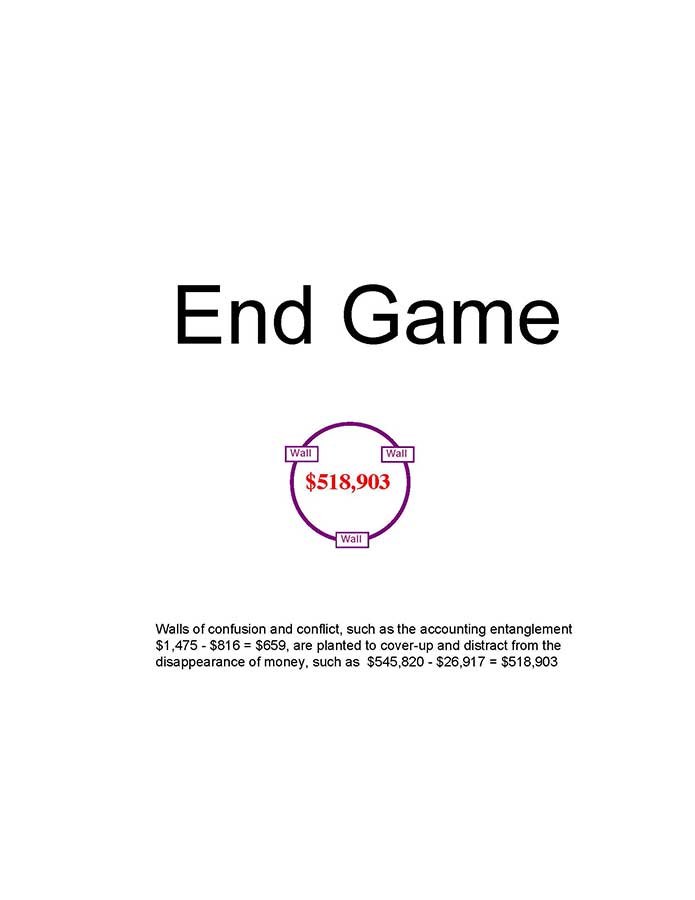

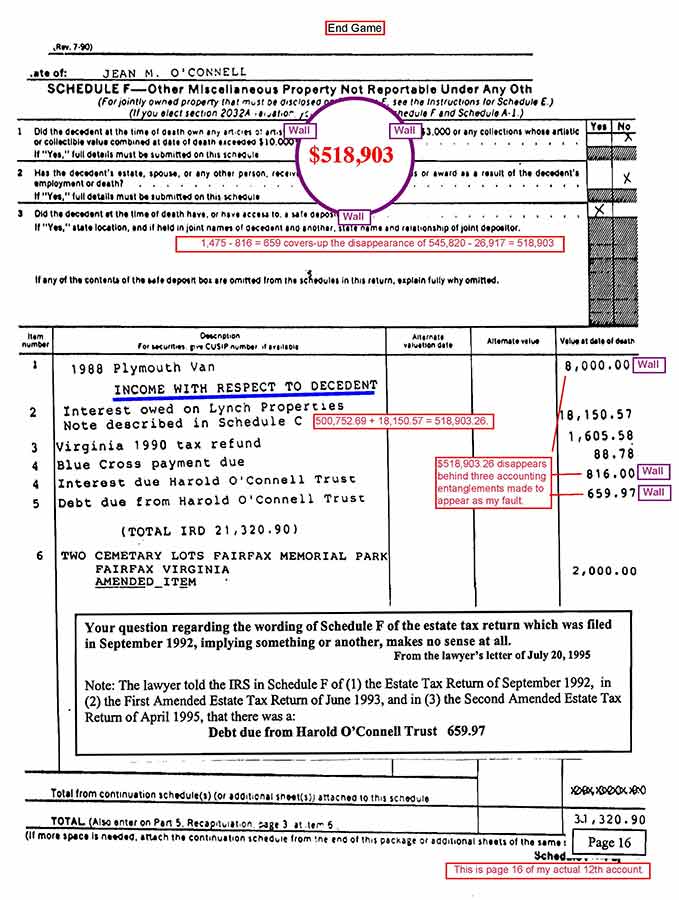

$518,903 disappears

How to make $518,903 disappear

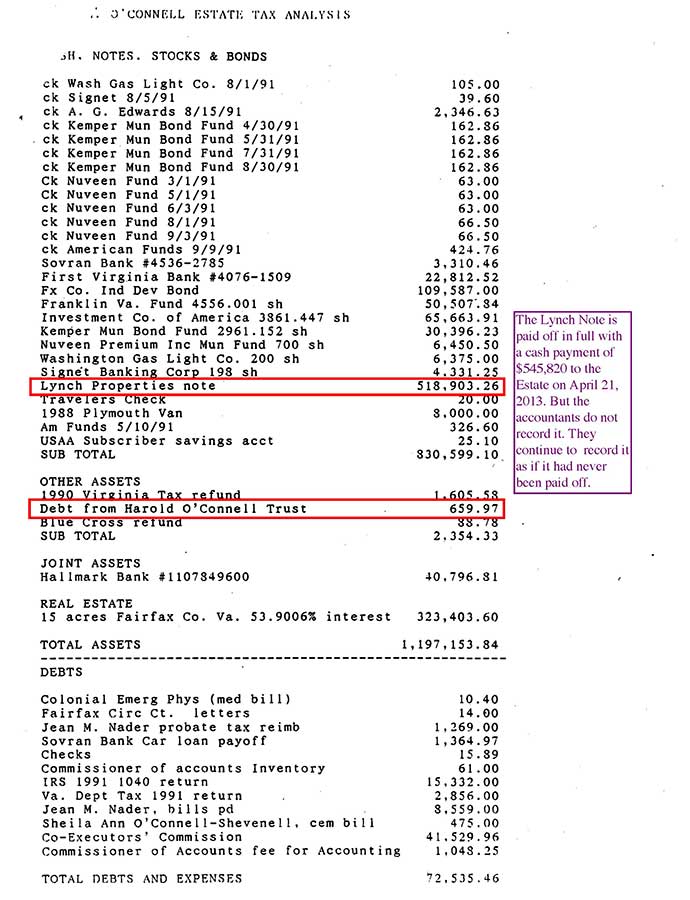

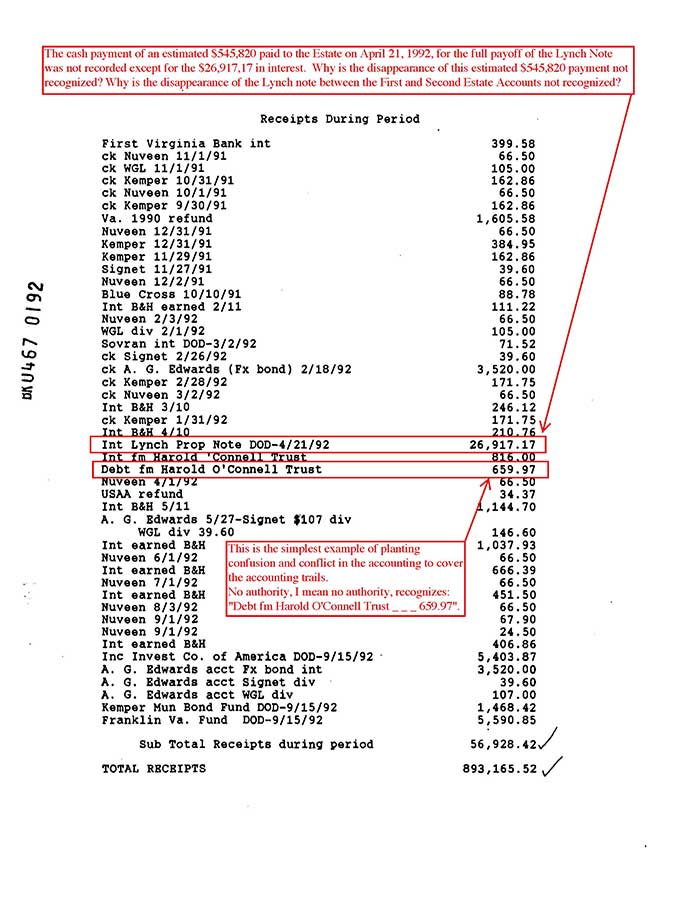

The CPA Joanne Barnes and the Attorney Edward White make money disappear and use our trusting sister as unwitting cover. A cash payment of $545,820.43 is made to our Mother's estate for the full payoff of the Lynch Note on April 21, 1992. But only the interest of $26,917.17 is reported. The difference of $518, 903.26 disappears. The only way to get to the truth is to follow the trails. 545,820.43 - $26,917.17 = $518,903.26.

The Lynch Note disappears between the First Estate Court Account and the Second Estate Court Account with no explanation. It continues to be reported to the IRS as if it had not been paid off but is still maturing towards it's scheduled maturity date of April 21, 1995.

Our trusting sister is used to unwittingly divide, disempower, and destroy, our family to cover it up.

(Review -)The CPA Joanne Barnes and the Attorney Edward White make money disappear and use our trusting sister as unwitting cover. A cash payment of $545,820.43 is made to our Mother's estate for the full payoff of the Lynch Note on April 21, 1992. But only the interest of $26,917.17 is reported. The difference of $518, 903.26 disappears. The only way to get to the truth is to follow the trails. You can always trust that 545,820.43 - $26,917.17 = $518,903.26.

Begin new 4

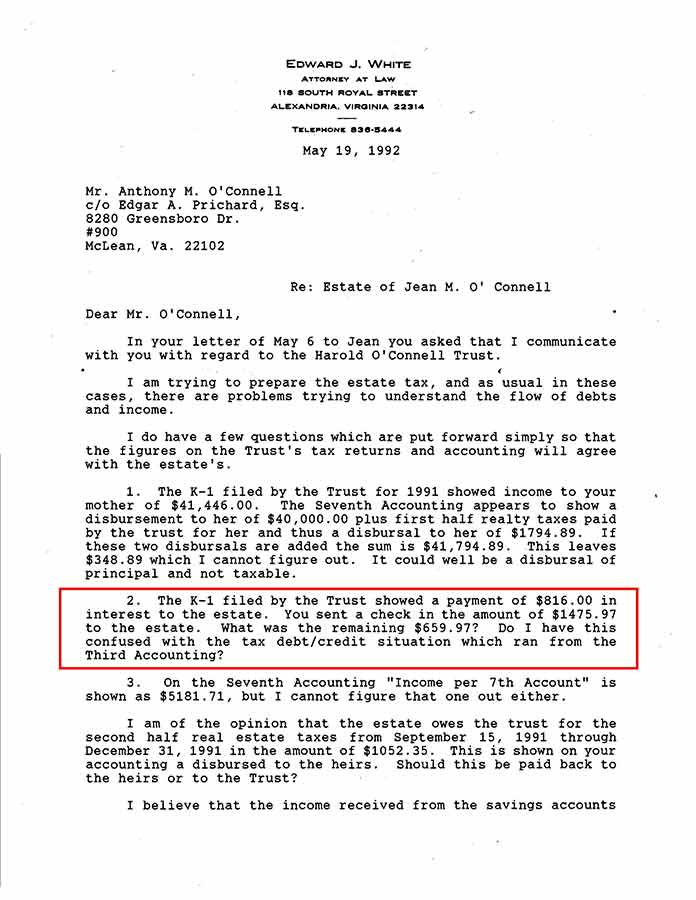

1992.02.18 (Edward White to Anthony O'Connell, copy to Jean Nader)

"Re: Estate of Jean M. O'Connell,

Dear Mr. O'Connell,

In order to prepare your mother's 1991 income tax returns, I need the amount that the Harold O'Connell Trust paid her during 1991. In the event the payment was not made in 1991, I will need to file the amount which was due as "income with respect to a decedent" on the estate tax and fiduciary tax returns. The cutoff date for your computation will be September 15, 1991. After that date the trust technically terminated, and the income belongs to the beneficiaries of that trust.

Jean and I are making progress on the estate. We have decided to leave the A. G. Edwards accounts in place since they are earning a better rate of return than a bank can give.

I am trying to get to the bottom of the car problem with Sovran and should be able to get the title soon so that it can be transferred to you before the insurance expires.

Jean has informed me that you and your sisters have decided that it is best to try and list the Accotink property at its actual value as of the of death rather than a higher value based on its future value. Since you have worked so diligently on this problem in the past, could you give me the name of an appraiser who could do a valuation which will take into account all of the county inspired problems. It seems to me that the county value of $600,000.00 is too high based on the hurdles you have run into in trying to develop it.

Could you also send me the address of Lynch Properties?

Sincerely, Edward J. White"

1992.02.25 (Edward White to Anthony O'Connell, copy to Jean Nader)

"I have received your letter of February 24, 1992 in which you request that I reconsider my refusal to resign as co-executor of your mother's estate.

Once more I decline to take such action.

When your mother approached me about changing the co-executors of her will, we discussed the matter at length. She specifically desired to make the changes which are in effect now, and was quite firm in her decision. It would be clearly disloyal of me to dishonor her intentions.

If you are represented, I will be glad to discuss this matter with your counsel.

Sincerely, Edward J. White"

End new 4

* * * Begin new 1

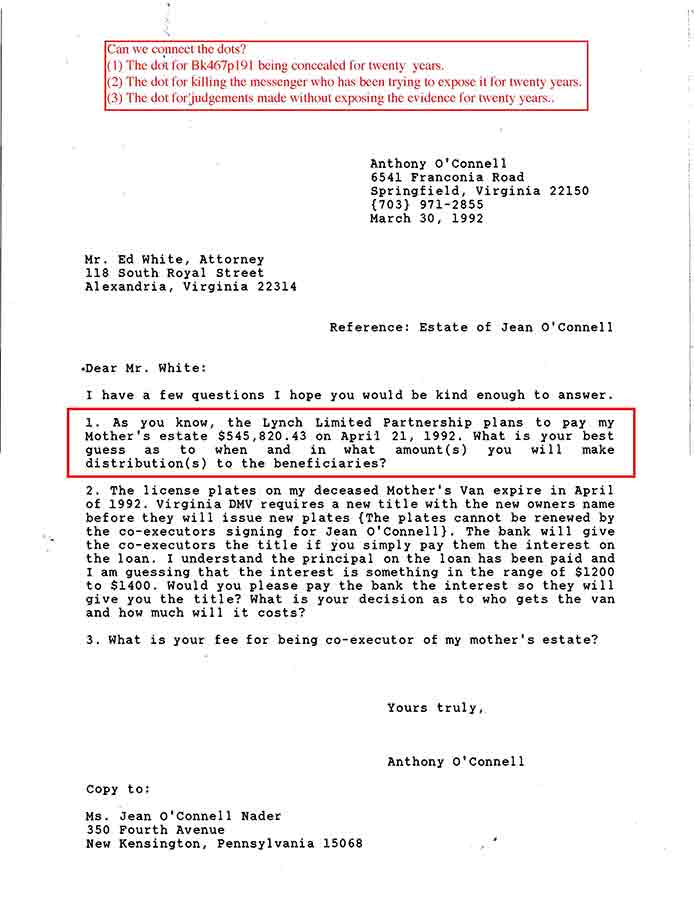

1) I ask attorney Edward White about the planned $545,820.43 payment.

1992.03.30 (Anthony

O'Connell

to Edward White) (Copy to Jean Nader)

"I have a few questions I hope you would be kind enough to answer.

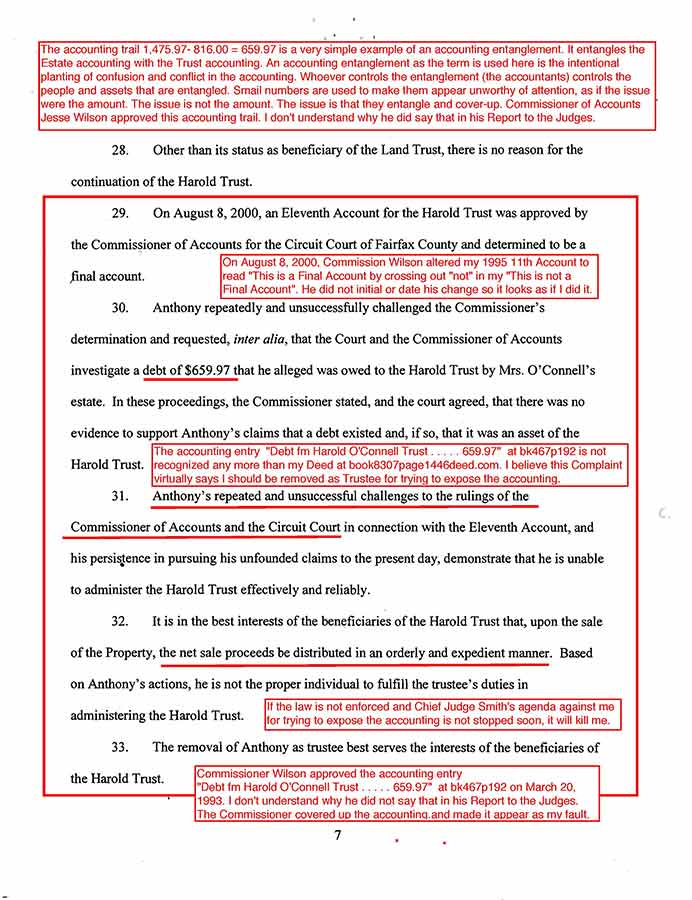

1. As you know, the Lynch Limited Partnership plans to pay my Mother's estate $545,820.43 on April 21, 1992. What is your best guess as to when and in what amount(s) you will make distribution(s) to the beneficiaries?

2. The license plates on my deceased Mother's Van expire in April of 1992. Virginia DMV requires a new title with the new owners name before they will issue new plates {The plates cannot be renewed by the co-executors signing for Jean O'Connell). The bank will give the co-executors the title if you simply pay them the interest on the loan. I understand the principal on the loan has been paid and I am guessing that the interest is something in the range of $1200 to $1400. Would you please pay the bank the interest so they will give you the title? What is your decision as to who gets the van and how much will it costs?

3. What is your fee for being co-executor of my mother's estate?

Yours truly, Anthony

O'Connell"

2) Edward White puts our trusting sister Jean Nader between himself and me. This is fatal.

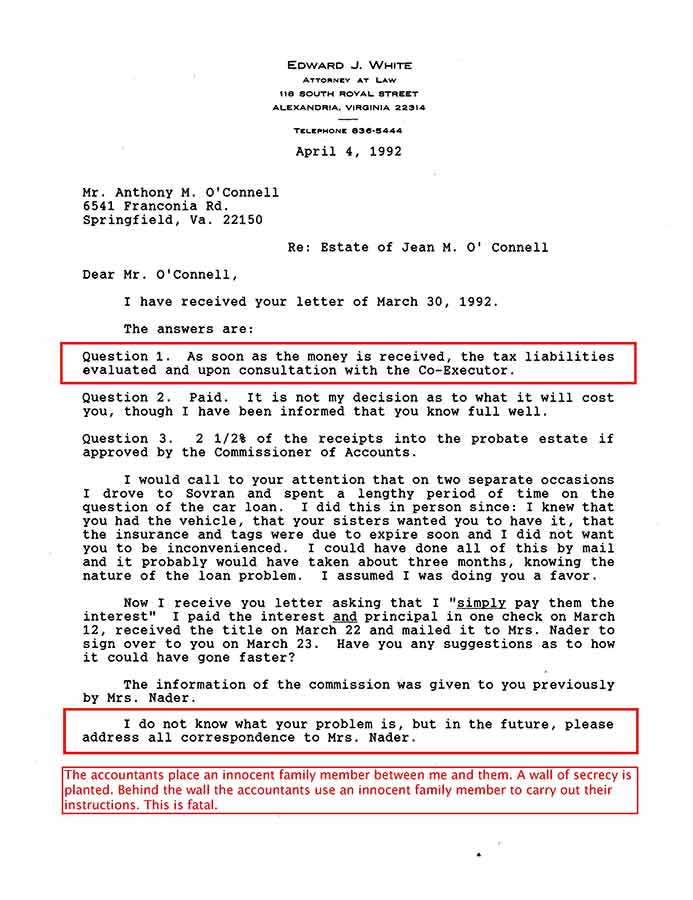

1992.04.04 (Edward White to Anthony O'Connell, copy to Jean Nader)

"I have received your letter of March 30, 1992.

The answers are:

Question 1. As soon as the money is received, the tax liabilities evaluated and upon consultation with the Co-Executor.

Question 2. Paid. It is not my decision as to what it will cost you, though I have been informed that you know full well.

Question 3. 2 Y % of the receipts into the probate estate if approved by the Commissioner of Accounts.

I would call to your attention that on two separate occasions I drove to Sovran and spent a lengthy period of time on the question of the car loan. I did this in person since: I knew that you had the vehicle, that your sisters wanted you to have it, that the insurance and tags were due to expire soon and I did not want you to be inconvenienced. I could have done all of this by mail and it probably would have taken about three months, knowing the nature of the loan problem. I assumed I was doing you a favor.

Now I receive you letter asking that I "simply pay them the interest" I paid the interest and principal in one check on March 12, received the title on March 22 and mailed it to Mrs. Nader to sign over to you on March 23. Have you any suggestions as to how it could have gone faster?

The information of the commission was given to you previously by Mrs. Nader.

I do not know what your problem is, but in the future, please address all correspondence to Mrs. Nader.

I am trying to be patient with you, but I find that this estate is time consuming enough without having to deal with letters such as the last two that I have received.

Sincerely, Edward J. White"

Comment:

This is fatal. Dividing the family is fatal. Wedges will be planted using trusting family member Jean Nader to carry them out so it looks as if the resultant confusion and conflict comes from the family. It is made to appear as if the family tore itself apart over money. The confusion and conflict cover the accounting trails.

3) On April 21, 1992, the $545,820.43 payment is made to the estate for the full premature payoff of the Lynch Note. I am shutout.

4) On April 22, 1992, the day after the $545,820.43 payment, .Edward White gives Jean Nader

covert instructions that will tear out family apart. He does not mention the $545,820.43 payment. I am shutout.

(Begin new 2)

The Attorney's covert instructions to our sister in the 4/22/92 letter below were made the day after the 4/21/92 payment of $545,820.43 (Jean Nader is so innocent she sent me a copy of this letter, not understanding that I was not supposed to see it.) The $545,820.43 payment is not mentioned. There are about nine major set ups in this letter. No family can survive this. (End new 2)

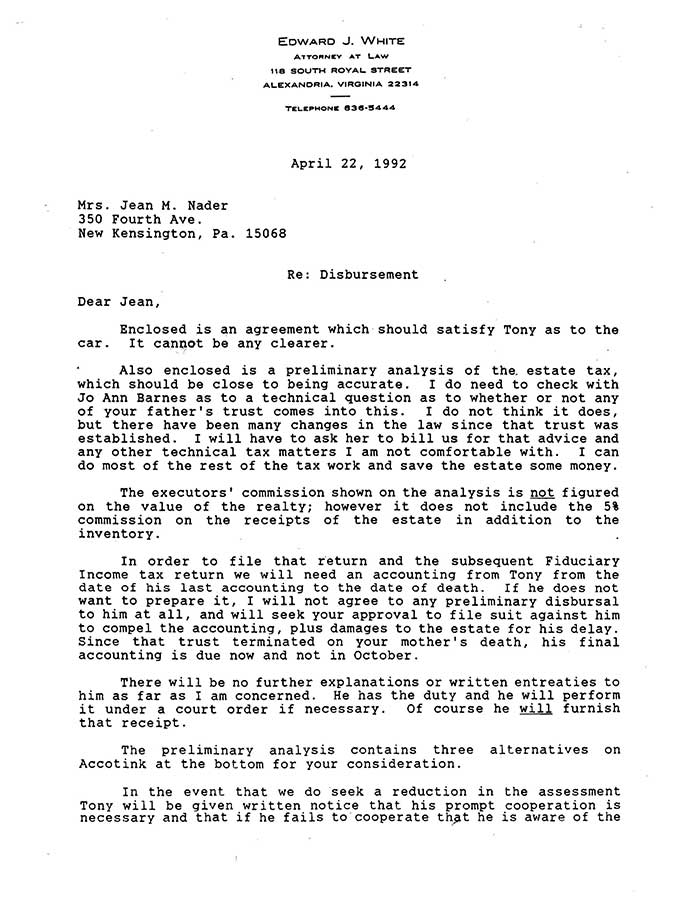

1992.04.22 (Edward White to Jean Nader)

"Enclosed is an agreement which should satisfy Tony as to the car. It cannot be any clearer.

Also enclosed is a preliminary analysis of the estate tax, which should be close to being accurate. I do need to check with Jo Ann Barnes as to a technical question as to whether or not any of your father's trust comes into this. I do not think it does, but there have been many changes in the law since that trust was established. I will have to ask her to bill us for that advice and any other technical tax matters I am not comfortable with. I can do most of the rest of the tax work and save the estate some money.

The executors' commission shown on the analysis is not figured on the value of the realty; however it does not include the 5% commission on the receipts of the estate in addition to the inventory.

In order to file that return and the subsequent Fiduciary Income tax return we will need an accounting from Tony from the date of his last accounting to the date of death. If he does not want to prepare it, I will not agree to any preliminary disbursal to him at all, and will seek your approval to file suit against him to compel the accounting, plus damages to the estate for his delay. Since that trust terminated on your mother's death, his final accounting is due now and not in October.

There will be no further explanations or written entreaties to him as far as I am concerned. He has the duty and he will perform it under a court order if necessary. Of course he will furnish that receipt.

The preliminary analysis contains three alternatives on Accotink at the bottom for your consideration.

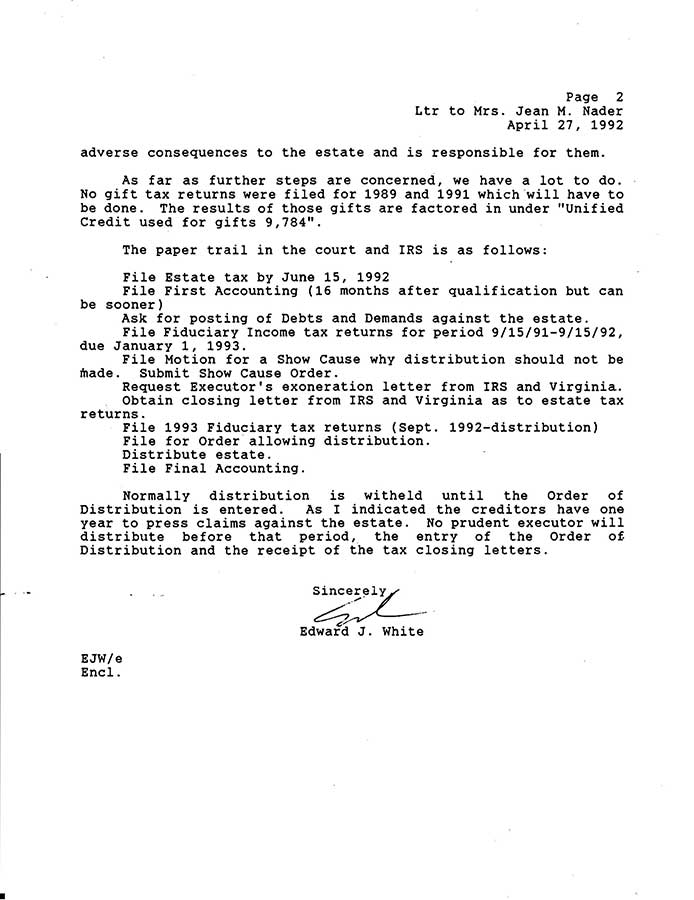

In the event that we do seek a reduction in the assessment Tony will be given written notice that his prompt cooperation is necessary and that if he fails to cooperate that he is aware of the adverse consequences to the estate and is responsible for them.

As far as further steps are concerned, we have a lot to do. No gift tax returns were filed for 1989 and 1991 which will have to be done. The results of those gifts are factored in under "Unified Credit used for gifts 9,784".

The paper trail in the court and IRS is as follows:

File Estate tax by June 15, 1992

File First Accounting (16 months after qualification but can be sooner)

Ask for posting of Debts and Demands against the estate.

File Fiduciary Income tax returns for period 9/15/91-9/15/92, due January 1, 1993.

File Motion for a Show Cause why distribution should not be made. Submit Show Cause Order.

Request Executor's exoneration letter from IRS and Virginia.

Obtain closing letter from IRS and Virginia as to estate tax returns.

File 1993 Fiduciary tax returns (Sept. 1992-distribution)

File for Order allowing distribution.

Distribute estate.

File Final Accounting.

Normally distribution is withheld until the Order of Distribution is entered. As I indicated the creditors have one year to press claims against the estate. No prudent executor will distribute before that period, the entry of the Order of Distribution and the receipt of the tax closing letters.

Sincerely, Edward J. White

EJW/e

Encl.

Comments:

a) These covert instructions were made the day after the $545,820.43 payment (Jean Nader is so innocent she sent me a copy of this letter, not understanding that I was not supposed to see it.) The payment is not mentioned. There are about nine major set ups in this letter. No family can survive this intact.

b) This covert letter to our sister, at the beginning of the administration of the estate, in 1992, under the guise of protecting the estate, in what is supposed to be a fiduciary relationship, urges my sister to take me to Court. It should not be a surprise, after 20 years of varying degrees of this agenda, that they got her to take me to Court in 2012 with the Complaint.

(Begin new 3)

This covert letter to our trusting sister, at the beginning of the administration of the estate, in 1992, under the guise of protecting the estate, in what is supposed to be a fiduciary relationship, urges my sister to take me to Court. It should not be a surprise, after 20 years of varying degrees of this agenda, that they got her to take me to Court in 2012 with the fraudulent Complaint in 2012. There is nothing you can do to stop them from tearing your family apart and taking over your famlies assets. The Virginia Bar would not stop it.

"Mr. Anthony M. O'Connell

Page 2

November 1, 1993

Finally, you indicate that Mr. White, over a period of seven years, has made

defamatory and divisive statements which you consider to be far more damaging than the

issue regarding the real estate settlement. The Code of Professional Responsibility does not

proscribe defamatory statements by an attorney, and our office is not the appropriate forum

to investigate or prosecute your claim. If you feel that you have been defamed or libeled

by the Respondent, then your remedy is to file a civil action, but a Bar complaint is not an

appropriate vehicle to resolve that issue.

I am truly sorry that I cannot advance your claims or interest, however, I must stand

on my original decision to dismiss your complaint. I trust that you will appreciate my

explanation, although you disagree with it.

Very truly yours

(seal)

James M. McCauley

Assistant Bar Counsel

JMM/dls"

(End new 3)

5) 1993.02.10 There is nothing you can do to stop them from tearing your family apart if one member of your family trusts them. The Virginia Bar did not stop the lawyer.

1993.02.10 Virginia Bar to Anthony OConnell

"The Respondent did not file a written answer to your complaint. However, Mr. White is represented by counsel in this matter, David R. Rosenfeld, Esquire, and I met with Mr. Rosenfeld and his associate in Alexandria to go over all of the factual matters related to this complaint."

1993.11.01 Virginia Bar to Anthony OConnell

"Finally, you indicate that Mr. White, over a period of seven years, has made defamatory and divisive statements which you consider to be far more damaging than the issue regarding the real estate settlement. The Code of Professional Responsibility does not proscribe defamatory statements by an attorney, and our office is not the appropriate forum to investigate or prosecute your claim. If you feel that you have been defamed or libeled by the Respondent, then your remedy is to file a civil action*, but a Bar complaint is not an appropriate vehicle to resolve that issue."

(*My taking my sister to Court instead of my sister taking me to Court does not protect our family.)

6) 2012.08.30 Their signature cover is to use a trusting family member to unwittingly divide, destabilize, and disempower, the family they victimize. They had my sister take me to Court. This skips over exposing the accounting at http://www.book467page191money.com. This is what the uninterrupted agenda described in the lawyer's letter of April 22, 1992, does .

COMPLAINT

COMES NOW the Plaintiff, Jean Mary O'Connell Nader, by counsel, and brings this

action pursuant to § 26-48 and 55-547.06 of the Code of Virginia (1950, as amended) for the removal and appointment of a trustee, and in support thereof states the following.

Parties and Jurisdiction

1. Plaintiff Jean Mary O’Connell Nader ("Jean") and *Defendants Anthony Miner

O’Connell ("Anthony") and Sheila Ann O'Connell ("Sheila") are the children of Harold A. O’Connell ("Mr. O’Connell"), who died in 1975, and Jean M. O'Connell ("Mrs. O'Connell"), who died on September 15, 1991.

2. The trusts that are the subject of this action are: (a) the trust created under the Last Will and Testament of Harold A. O'Connell dated April 11, 1974, and admitted to probate in this Court on June 18, 1975; and (b) a Land Trust Agreement dated October 16, 1992, which was recorded among the land records of this Court in Deed Book 8845 at Page 1449.

3. Jean, Sheila, and Anthony are the beneficiaries of both of the trusts and, therefore, are the parties interested in this proceeding.

Facts

4. During their lifetimes, Mr. and Mrs. O'Connell owned as *tenants in common a

parcel of unimproved real estate identified by Tax Map No. 0904-0 1-00 17 and located near the Franconia area of Fairfax County, Virginia and consisting of approximately 15 acres (the "Property").

5. After his death in 1975, a 46.0994% interest in the Property deriving fiom Mr,

O'Connell's original 50% share was transferred to a trust created under his Last Will and Testament (the "Harold Trust"), of which Anthony serves as trustee. A copy of the Last Will and Testament of Harold A. O'Connell is attached hereto as Exhibit A.

6. Mrs. O'Connell held a life interest in the Harold Trust and, upon her death in

1991, the trust assets were to be distributed in equal shares to Jean, Sheila, and Anthony as remainder beneficiaries. Although other assets of the Harold Trust were distributed to the remainder beneficiaries, the trust's 46.0994% interest in the Property has never been distributed to Jean, Sheila, and Anthony in accordance with the terms of the Harold Trust.

7. After Mrs. O'Connell's death, her 53.9006% interest in the Property passed to

Jean, Sheila, and Anthony in equal shares, pursuant to the terms of her Last Will and Testament and Codicil thereto, which was admitted to probate in this Court on December 10, 1991.

8. Thus, after Mrs. O'Connell's death, Jean, Sheila, and Anthony each owned a

17.96687% interest in the Property, and the Harold Trust continued to own a 49.0994% interest in the Property.

9. By a Land Trust Agreement dated October 16, 1992, Jean, Sheila, and Anthony,

individually and in his capacity as trustee of the Harold Trust, created a Land Trust (the "Land Trust"), naming Anthony as initial trustee. A copy of the Land Trust Agreement is attached hereto as Exhibit B and incorporated by reference herein. The Harold Trust, Jean, Sheila, and Anthony (individually) are the beneficiaries of the Land Trust.

10. The Property was thereafter conveyed by Jean, Sheila, and Anthony, individually

and as trustee of the Harold Trust, to Anthony, as trustee of the Land Trust, by a Deed dated October 16,1992 and recorded on October 23,1992 in Deed Book 8307 at Page 1446 among the land records for Fairfax County.

11. As trustee under the Land Trust, Anthony was granted broad powers and

responsibilities in connection with the Property, including the authority and obligation to sell the Property. Paragraph 4.04 of the Land Trust Agreement states, in part, as follows:

If the Property or any part thereof remains in this trust at the expiration of twenty (20) years from date hereof, the Trustee shall promptly sell the Property at a public sale after a reasonable public advertisement and reasonable notice thereof to the Beneficiaries.

12. To date, the Property has not been sold, and the Land Trust is due to expire on

October 16,2012.

13. According to Paragraph 9.03 of the Land Trust Agreement, the responsibility for

payment of all real estate taxes on the Property is to be shared proportionately by the

beneficiaries. However, if a beneficiary does not pay his or her share, the Land Trust Agreement provides:

The Trustee will pay the shortfall and shall be reimbursed the principal plus 10% interest per annum. Trustee shall be reimbursed for any outstanding real estate tax shares or other Beneficiary shared expense still owed by any Beneficiary at settlement on the eventual sale of the property.

14. For many years, Jean sent payment to Anthony for her share of the real estate

taxes on the Property. Beginning in or about 1999, Anthony refused to accept her checks because they were made payable to "County of Fairfax." Anthony insisted that any checks for the real estat'k taxes be made payable to him individually, and he has returned or refused to forward Jean's checks to Fairfax County. Under the circumstances, Jean is unwilling to comply with Anthony's demands regarding the tax payments.

15. Anthony is not willing or has determined he is unable to sell the Property due to a

mistaken interpretation of events and transactions concerning the Property and, upon information and belief, the administration of his mother's estate. Anthony's position remains intractable, despite court rulings against him, professional advice, and independent evidence. As a result, Anthony is unable to effectively deal with third parties and the other beneficiaries of the Land Trust.

16. In 2007, Anthony received a reasonable offer from a potential buyer to purchase

the Property. Upon information and belief, Anthony became convinced of a title defect with the Property that, in his opinion, was an impediment to the sale of the Property. A title commitment issued by Stewart Title and Escrow on April 24,2007, attached hereto as Exhibit C, did not persuade Anthony that he, as the trustee of the Land Trust, had the power to convey the Property. Because of this and other difficulties created by Anthony, the Property was not sold.

17. Since 2007, it appears the only effort put forth by Anthony to sell the Property has

been to post it for sale on a website he created, http://www.alexandriavirginial5acres.com

18. Since 2009, Anthony has failed to pay the real estate taxes for the Property as

required by the Lhd Trust Agreement. Currently, the amount of real estate tax owed, including interest and penalties, is approximately $27,738.00.

19. Anthony has stated that he purposely did not pay the real estate taxes in order to

force a sale of the Property and clear up the alleged title defects.

20. Since the real estate taxes are more than two years delinquent, Anthony's failure

to pay may result in a tax sale of the Property. Anthony was notified of this possibility by a notice dated October 26, 201 1, attached hereto as Exhibit D. In addition to the threatened tax sale, the Land Trust is incurring additional costs, including penalties, interest, and fees, that would not be owed if Anthony had paid the real estate taxes in a timely manner.

21. In May 20 12, Jean, through her counsel, wrote a letter to Anthony requesting that

he cooperate with a plan to sell the Property or resign as trustee. To date, Anthony has not expressed a willingness to do either, and still maintains that the alleged title defect and other "entanglements" must be resolved before any action can be taken towards a sale of the Property.

Count I: Removal of Anthony O'Connell as Trustee of Land Trust

22: The allegations of paragraphs 1 through 21 are incorporated by reference as if

fully stated herein.

23. As trustee of the Land Trust, Anthony has a fiduciary duty to comply with the

terms of the trust agreement, to preserve and protect the trust assets, and to exercise reasonable care, skill, and caution in the administration of the trust assets.

24. Anthony has breached his fiduciary duties by his unreasonable, misguided, and imprudent actions, including but not limited to, his failure to sell the Property and non-payment of the real estate taxes on the Property.

25. The breaches of duty by Anthony constitute good cause for his removal as trustee

of the Land Trust.

WHEREFORE, Plaintiff Jean Mary O'Connell Nader prays for the following relief:

A. That the Court remove Anthony Minor O'Connell as trustee under the Land Trust

Agreement dated October 16, 1992, pursuant to 26-48 of the Code of Virginia

(1950, as amended);

B. That all fees payable to Anthony Minor O'Connell under the terms of the

aforesaid Land Trust Agreement, including but not limited to, the trustee's

compensation under paragraph 9.01, and all interest on advancements by the

trustee to the trust for payment of real estate taxes pursuant to paragraph 9.03, be

disallowed and deemed forfeited;

C. That all costs incurred by Plaintiff Jean Mary O'Connell Nader in this action,

including reasonable attorneys' fees, be paid by the Land Trust; and

D. For all such further relief as this Court deems reasonable and proper.

Count 11: Removal of Anthony O'Connell as Trustee of the Trust under the Will of Harold A. O'Connell

26. The allegations of paragraphs 1 through 25 are incorporated by reference as if

fully stated herein.

27. The terms of the Harold Trust provide that, upon the death of Mrs. O'Connell, the

assets are to be distributed to Jean, Sheila, and Anthony in equal shares. Notwithstanding the terms of the Harold Trust and the provisions for its termination, Anthony entered into the Land

Trust Agreement in his capacity as trustee of the Harold Trust. As a result, upon the sale of the

Property, Anthony can exercise greater control over the Harold Trust's share of the sale proceeds

than if the parties held their beneficial interests in their individual capacities.

28, Other than its status as beneficiary of the Land Trust, there is no reason for the

continuation of the Harold Trust.

29. On August 8,2000, an Eleventh Account for the Harold Trust was approved by the Commissioner of Accounts for the Circuit Court of Fairfax County and determined to be a final account.

30. Anthony repeatedly and unsuccessfully challenged the Commissioner's determination and requested, inter alia, that the Court and the Commissioner of Accounts investigate a debt of $659.97 that he alleged was owed to the Harold Trust by Mrs. O'Connell's estate. In these proceedings, the Commissioner stated, and the court agreed, that there was no evidence to support Anthony's claims that a debt existed and, if so, that it was an asset of the Harold Trust.

31. Anthony's repeated and unsuccessful challenges to the rulings of the

Commissioner of Accounts and the Circuit Court in connection with the Eleventh Account, and his persistence in pursuing his unfounded claims to the present day, demonstrate that he is unable to administer the Harold Trust effectively and reliably.

32. It is in the best interests of the beneficiaries of the Harold Trust that, upon the sale

of the Property, the net sale proceeds be distributed in an orderly and expedient manner. Based on Anthony's actions, he is not the proper individual to fulfill the trustee's duties in administering the Harold Trust.

33. The removal of Anthony as trustee best serves the interests of the beneficiaries of the Harold Trust.

WHEREFORE, Plaintiff Jean Mary O'Connell Nader prays for the following relief:

A. That the Court remove Anthony Minor O'Connell as trustee under the Last Will

and Testament of Harold A. O'Connell, pursuant to § 55-547.06 of the Code of

Virginia (1 950, as amended);

B. That all costs incurred by Plaintiff Jean Mary O'Comell Nader in this action

including reasonable attorneys' fees, be awarded to her in accordance with § 55- 550.04 of the Code of Virginia (1950, as amended); and

C. For all such further relief as this Court deems reasonable and proper.

Count 111: Appointment of Successor Trustee

34. The allegations of paragraphs 1 through 33 are incorporated by reference as if

fully stated herein.

35. Jean is a proper person to serve as trustee of the Land Trust in order to sell the

Property on behalf of the beneficiaries of the Land Trust, and she is willing and able to serve in such capacity.

36. The best interests of the beneficiaries would be served if the Land Trust is continued for a sufficient period of time to allow the successor trustee to sell the Property, rather than allowing the Land Trust to terminate on the date specified in the Land Trust Agreement. Each of the individual beneficiaries of the Land Trust is age 70 or above, and it would be prudent to sell the Property during their lifetimes, if possible, rather than leaving the matter for the next generation to resolve.

37. Jean is a proper person to serve as trustee of the trust created under the Last Will

and Testament of Harold A. O'Connell, and she is willing and able to serve in such capacity.

WHEREFORE, Plaintiff Jean Mary O'Connell Nader prays for the following relief:

A. That Plaintiff Jean Mary O'Connell Nader be appointed as successor trustee under

the aforesaid Land Trust Agreement, with the direction to sell the Property upon

such terms and conditions as this Court deems reasonable and appropriate,

including, but not limited to, fixing a reasonable amount as compensation of the

successor trustee for her services;

B. That the term of the Land Trust be continued for a reasonable time in order to

allow for the sale of the Property;

C. That Plaintiff Jean Mary O'Connell Nader be appointed as successor trustee under

the Last Will and Testament of Harold A. O'Connell for all purposes, including

distribution of the net proceeds of the sale of the Property that are payable to such

trust;

D. That all costs incurred by Plaintiff Jean Mary O'Connell Nader in this action,

including reasonable attorneys' fees, be paid by the Land Trust; and

E. For all such further relief as this Court deems reasonable and proper.

* * * End of new 1

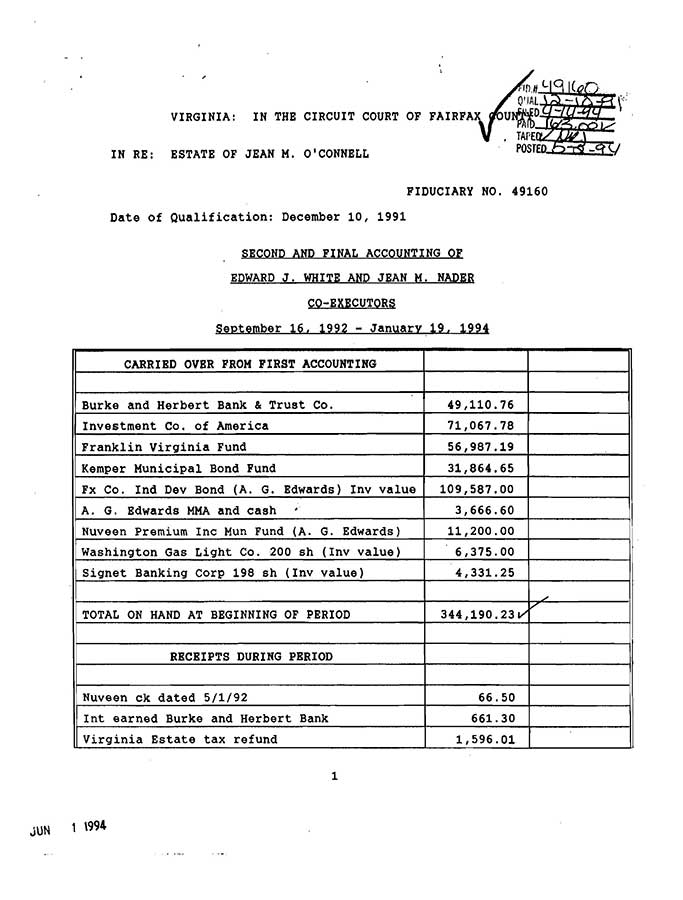

The Lynch Note disappears between the First Court Accounting (above) and the Second and Final Court Accounting (below) with no explanation. It continues to be reported to the IRS as if it had not been paid off but is still maturing towards it's scheduled maturity date of April 21, 1995.

* * * * *

(1 - I ask attorney Edward White about the planned $545,820.43 payment.)

1992.03.30 (Anthony

O'Connell

to Edward White) (Copy to Jean Nader)

"I have a few questions I hope you would be kind enough to answer.

1. As you know, the Lynch Limited Partnership plans to pay my Mother's estate $545,820.43 on April 21, 1992. What is your best guess as to when and in what amount(s) you will make distribution(s) to the beneficiaries?

2. The license plates on my deceased Mother's Van expire in April of 1992. Virginia DMV requires a new title with the new owners name before they will issue new plates {The plates cannot be renewed by the co-executors signing for Jean O'Connell). The bank will give the co-executors the title if you simply pay them the interest on the loan. I understand the principal on the loan has been paid and I am guessing that the interest is something in the range of $1200 to $1400. Would you please pay the bank the interest so they will give you the title? What is your decision as to who gets the van and how much will it costs?

3. What is your fee for being co-executor of my mother's estate?

Yours truly, Anthony

O'Connell"

(2 - Edward White puts our trusting sister Jean Nader between himself and me. This is fatal.)

1992.04.04 (Edward White to Anthony O'Connell, copy to Jean Nader)

"I have received your letter of March 30, 1992.

The answers are:

Question 1. As soon as the money is received, the tax liabilities evaluated and upon consultation with the Co-Executor.

Question 2. Paid. It is not my decision as to what it will cost you, though I have been informed that you know full well.

Question 3. 2 Y % of the receipts into the probate estate if approved by the Commissioner of Accounts.

I would call to your attention that on two separate occasions I drove to Sovran and spent a lengthy period of time on the question of the car loan. I did this in person since: I knew that you had the vehicle, that your sisters wanted you to have it, that the insurance and tags were due to expire soon and I did not want you to be inconvenienced. I could have done all of this by mail and it probably would have taken about three months, knowing the nature of the loan problem. I assumed I was doing you a favor.

Now I receive you letter asking that I "simply pay them the interest" I paid the interest and principal in one check on March 12, received the title on March 22 and mailed it to Mrs. Nader to sign over to you on March 23. Have you any suggestions as to how it could have gone faster?

The information of the commission was given to you previously by Mrs. Nader.

I do not know what your problem is, but in the future, please address all correspondence to Mrs. Nader.

I am trying to be patient with you, but I find that this estate is time consuming enough without having to deal with letters such as the last two that I have received.

Sincerely, Edward J. White"

Comment:

This is fatal. Dividing the family is fatal. Wedges will be planted using trusting family member Jean Nader to carry them out so it looks as if the resultant confusion and conflict comes from the family. It is made to appear as if the family tore itself apart over money. The confusion and conflict cover the accounting trails.

(3 - On April 21, 1992, the $545,820.43 payment is made to the estate for the full premature payoff of the Lynch Note. Concealed from me.)

(4 - On April 22, 1992, the day after the $545,820.43 payment, .Edward White gives Jean Nader

covert instructions that will tear out family apart. He does not mention the $545,820.43 payment. Concealed from me.)

1992.04.22 (Edward White to Jean Nader)

"Enclosed is an agreement which should satisfy Tony as to the car. It cannot be any clearer.

Also enclosed is a preliminary analysis of the estate tax, which should be close to being accurate. I do need to check with Jo Ann Barnes as to a technical question as to whether or not any of your father's trust comes into this. I do not think it does, but there have been many changes in the law since that trust was established. I will have to ask her to bill us for that advice and any other technical tax matters I am not comfortable with. I can do most of the rest of the tax work and save the estate some money.

The executors' commission shown on the analysis is not figured on the value of the realty; however it does not include the 5% commission on the receipts of the estate in addition to the inventory.

In order to file that return and the subsequent Fiduciary Income tax return we will need an accounting from Tony from the date of his last accounting to the date of death. If he does not want to prepare it, I will not agree to any preliminary disbursal to him at all, and will seek your approval to file suit against him to compel the accounting, plus damages to the estate for his delay. Since that trust terminated on your mother's death, his final accounting is due now and not in October.

There will be no further explanations or written entreaties to him as far as I am concerned. He has the duty and he will perform it under a court order if necessary. Of course he will furnish that receipt.

The preliminary analysis contains three alternatives on Accotink at the bottom for your consideration.

In the event that we do seek a reduction in the assessment Tony will be given written notice that his prompt cooperation is necessary and that if he fails to cooperate that he is aware of the adverse consequences to the estate and is responsible for them.

As far as further steps are concerned, we have a lot to do. No gift tax returns were filed for 1989 and 1991 which will have to be done. The results of those gifts are factored in under "Unified Credit used for gifts 9,784".

The paper trail in the court and IRS is as follows:

File Estate tax by June 15, 1992

File First Accounting (16 months after qualification but can be sooner)

Ask for posting of Debts and Demands against the estate.

File Fiduciary Income tax returns for period 9/15/91-9/15/92, due January 1, 1993.

File Motion for a Show Cause why distribution should not be made. Submit Show Cause Order.

Request Executor's exoneration letter from IRS and Virginia.

Obtain closing letter from IRS and Virginia as to estate tax returns.

File 1993 Fiduciary tax returns (Sept. 1992-distribution)

File for Order allowing distribution.

Distribute estate.

File Final Accounting.

Normally distribution is withheld until the Order of Distribution is entered. As I indicated the creditors have one year to press claims against the estate. No prudent executor will distribute before that period, the entry of the Order of Distribution and the receipt of the tax closing letters.

Sincerely, Edward J. White

EJW/e

Encl.

| JEAN M .O'CONNELL ESTATE TAX ANALYSIS |

|

|

|

|

| CASH(?), NOTES, STOCKS & BONDS. |

|

|

|

|

| ck Wash Gas Light Co. 8/1/91 |

|

105.00 |

|

|

| ck Signet 8/5/91 |

|

39.00 |

|

|

| ck A. G. Edwards 8/15/91 |

|

2,346.63 |

|

|

| ck Kemper Mun Bond Fund 4/30/91 |

|

162.86 |

|

|

| ck Kemper Mun Bond Fund 5/31/91 |

|

162.86 |

|

|

| ck Kemper Mun Bond Fund 7/31/91 |

|

162.86 |

|

|

| ck Kemper Mun Bond Fund 8/30/91 |

|

162.86 |

|

|

| Ck Nuveen Fund 3/1/9 |

|

63.00 |

|

|

| Ck Nuveen Fund 5/1/91 |

|

63.00 |

|

|

| ck Nuveen Fund 6/3/91 |

|

63.00 |

|

|

| ck Nuveen Fund 8/1/91 |

|

66.50 |

|

|

| ck Nuveen Fund 9/3/91 |

|

66.50 |

|

|

| ck American Funds 9/9/91 |

|

424.76 |

|

|

| Sovran Bank #4536-2785 |

|

3.310.46 |

|

|

| First Virginia Bank #4076-1509 |

|

22,812.52 |

|

|

| Fx Co. Ind Dev Bond |

|

109,587.00 |

|

|

| FranklinxVa. Fund 4556.001 sh |

|

50.507.84 |

|

|

| Investment Co. of America 3861.447 sh |

|

65.663.91 |

|

|

| Kemper Mun Bond Fund 2961.152 sh |

|

30,396.23 |

|

|

| Nuveen Premium Inc Mun Fund 700 shWashington Gas Light Co. 200 sh |

|

6.450.60 |

|

|

| Washington Gas Light Co. 200 sh |

|

6.375.00 |

|

|

| Signet Banking Corp 198 sh |

|

4.331.25 |

|

|

| Lynch Properties note |

|

518,903.26 |

This note was paid off in full the previous day. This $518,903.26 disappeared. |

| Travelers Check |

|

20.00 |

|

|

| 1988 Plymouth Van |

|

8.000.00 |

|

|

| Am Funds 5/10/91 |

|

326.60 |

|

|

| USAA Subscriber savings acct |

|

25.10 |

|

|

| SUB TOTAL |

|

830,599.10 |

|

|

| OTHER ASSETS |

|

|

|

|

| 1990 Virginia Tax refund |

|

1,605.58 |

|

|

| Debt from Harold O'Connell Trust |

|

659.97 |

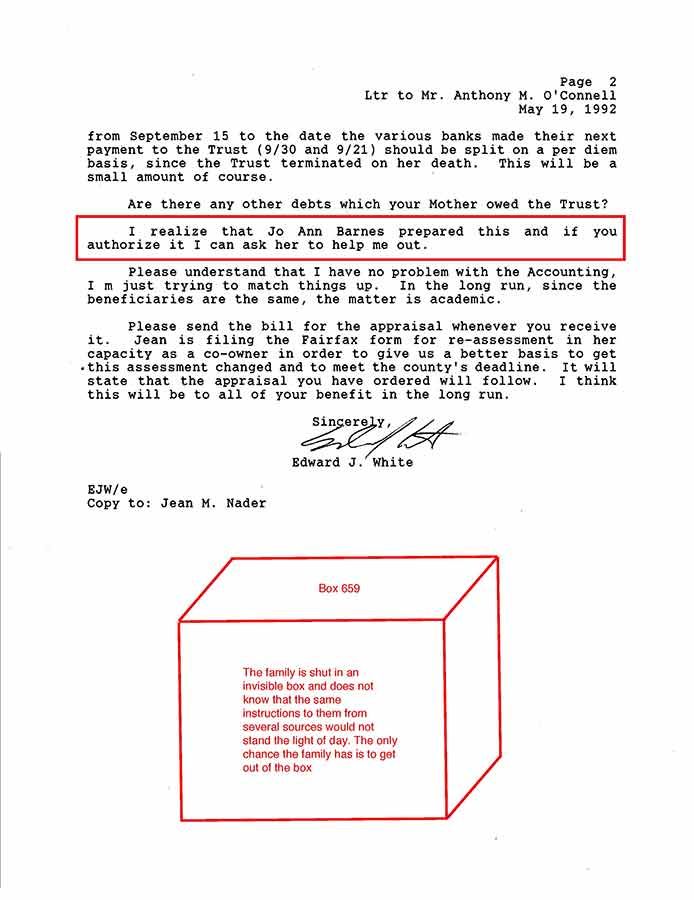

About a month later Edward White will ask me what this is which makes it appear that I created it. |

| Blue Cross refund |

|

88.78 |

|

|

| SUB TOTAL |

|

2354.33 |

|

|

| JOINT ASSETS |

|

|

|

|

| Hallmark Bank #1107849600 |

|

40,796.81 |

|

|

| REAL ESTATE |

|

|

|

|

| 15 acres Fairfax Co. Va. 53.9006% interest |

|

323,403.60 |

|

|

| TOTAL ASSETS |

|

1,197,153.84 |

|

|

| -------------------------------------------------------- |

|

|

|

|

| DEBTS |

|

|

|

|

| Colonial Emerg Phys (med bill) |

|

10.40 |

|

|

| Fairfax Circ Ct. letters |

|

14.00 |

|

|

| Jean M. Nader probate tax reimb |

|

1,269.00 |

|

|

| Sovran Bank Car loan payoff |

|

1,364.97 |

|

|

| Checks |

|

15.89 |

|

|

| Commissioner of accounts Inventory |

|

61.00 |

|

|

| IRS 1991 1040 return |

|

15,332.00 |

|

|

| Va. Dept Tax 1991 return |

|

2,856.00 |

|

|

| Jean M. Nader, hills pd |

|

8,559.00 |

|

|

| Sheila Ann O'Connell-Shevenell, cem bill |

|

475.00 |

|

|

| Co-Executors' Commission |

|

41,529.96 |

|

|

| Commissioner of Accounts fee for Accounting |

|

1,048.25 |

|

|

| TOTAL DEBTS AND EXPENSES |

|

72,535.46 |

|

|

| JEAN M. O'CONNELL ES'I'A'l'E TAX ANAI.YSIS [page 2] |

|

|

|

|

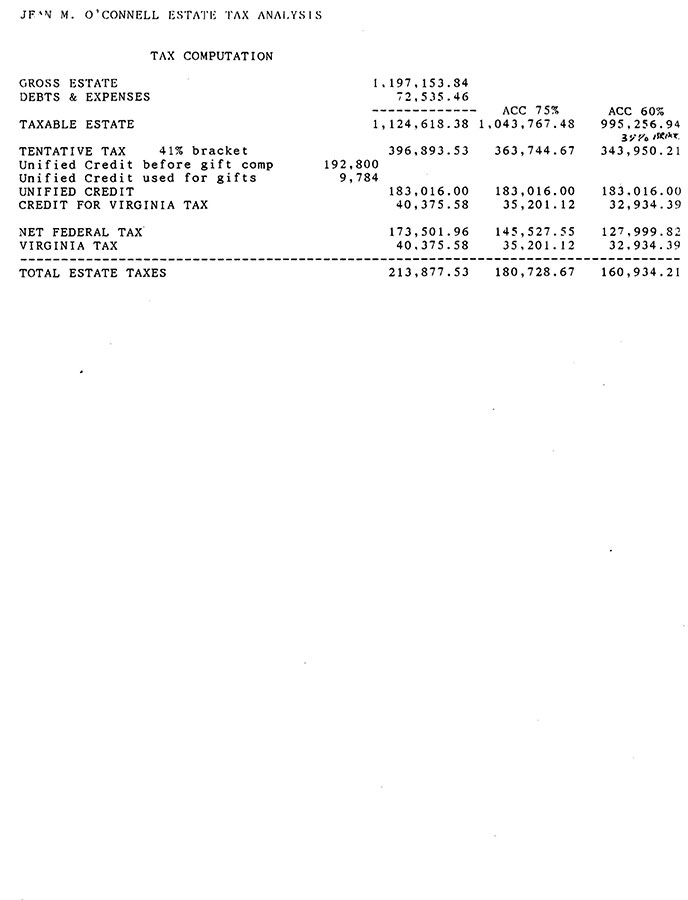

TAX COMPUTATION |

|

|

|

|

| GROSS ESTATE |

|

1,197,153.84 |

|

|

| DEBTS & EXPENSES |

|

72,535.46 |

|

|

| |

|

|

ACC 75% |

ACC 60% |

| TAXABLE ESTATE |

|

1,124,615.38 |

1,043,767.48 |

995,256.94 |

| TENTATIVE TAX 41% bracket |

|

396,893.53 |

363,744.67 |

343,950.21 |

Unified Credit before gift comp |

192,800 |

|

|

|

| Unified Credit used for gifts |

9,784 |

|

|

|

| UNIFIED CREDIT |

|

183,016.00 |

183,016.00 |

183,016.00 |

| CREDIT FOR VIRGINIA TAX |

|

40,375.58 |

35,201.12 |

32.934.39 |

| NET FEDERAL TAX |

|

|

|

127.999.82 |

| VIRGINIA TAX |

|

|

|

32.934.39 |

| ---------------------------------------------- |

------ |

------------ |

---------- |

--------- |

| TOTAL ESTATE TAXES |

|

213,877.53 |

180,728.67 |

160,934.21 |

| |

|

|

|

|

| |

|

|

|

|

Comments:

a) These covert instructions were made the day after the $545,820.43 payment (Jean Nader is so innocent she sent me a copy of this letter, not understanding that I was not supposed to see it.) The $545,820.43 payment is not mentioned. There are about nine major set ups in this letter. No family can survive this intact.

b) This covert letter to our sister, at the beginning of the administration of the estate, in 1992, under the guise of protecting the estate, in what is supposed to be a fiduciary relationship, urges my sister to take me to Court. It should not be a surprise, after 20 years of varying degrees of this agenda, that they got her to take me to Court in 2012 with the Complaint.

(5 - The Lynch Note disappears between the First Estate Court Account and the Second Estate Court Account with no explanation. It continues to be reported to the IRS as if it had not been paid off but is still maturing towards it's scheduled maturity date of April 21, 1995.)

* * * * *

Add

From 518903-transcscripts-11webs.html 46kb

May 19 letter (Text, not pdf)

page 7 of complaint (image and text)

add white's feb 18, 1992 (Add it "End Game"?

From 518903-transscript .html 40kb

From 518903-10webs.html 14kb

|