Footnote 16

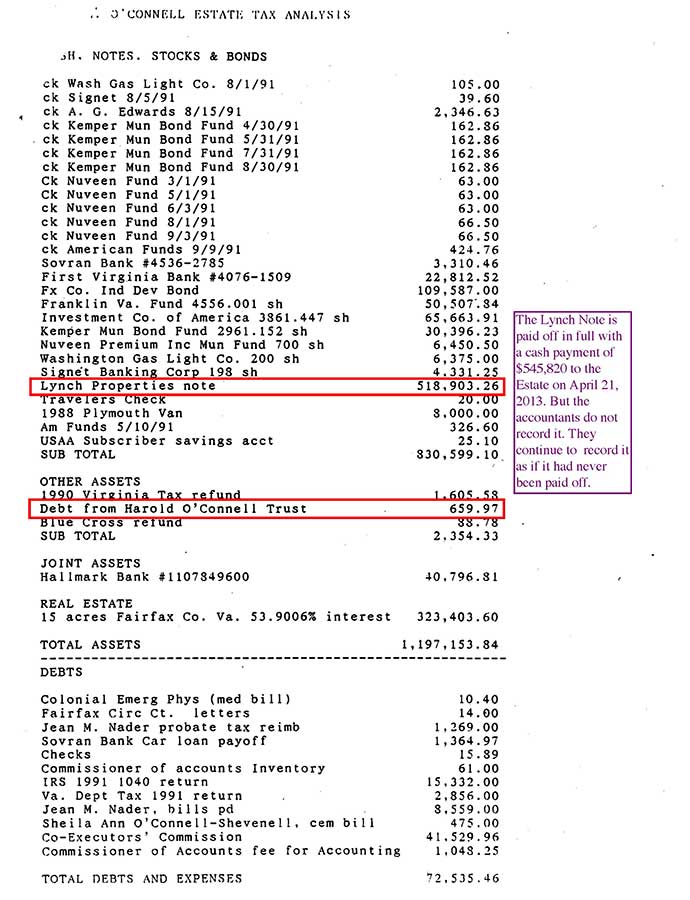

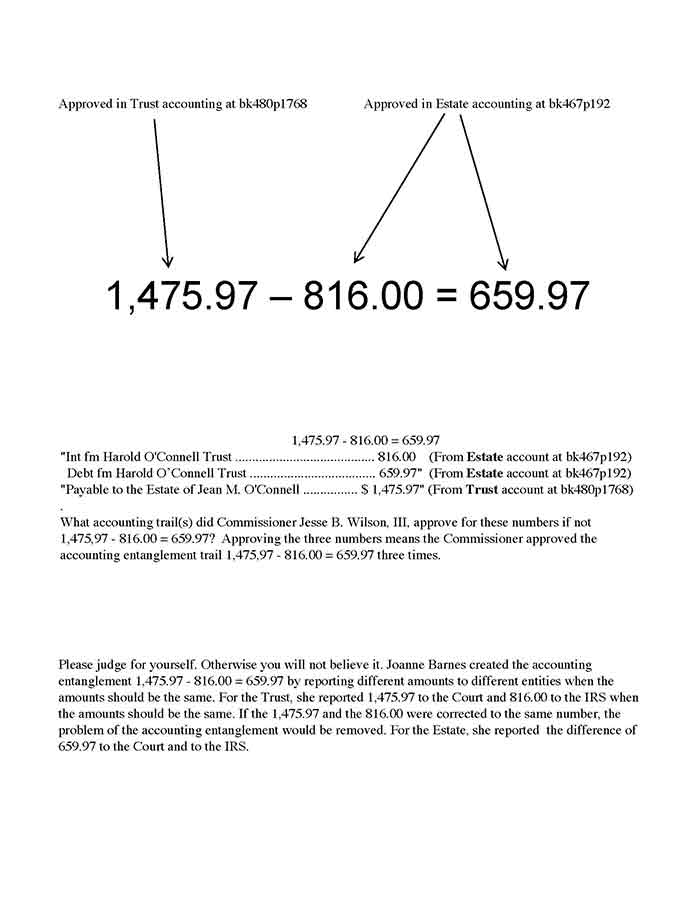

659 covers 518903

26 pages

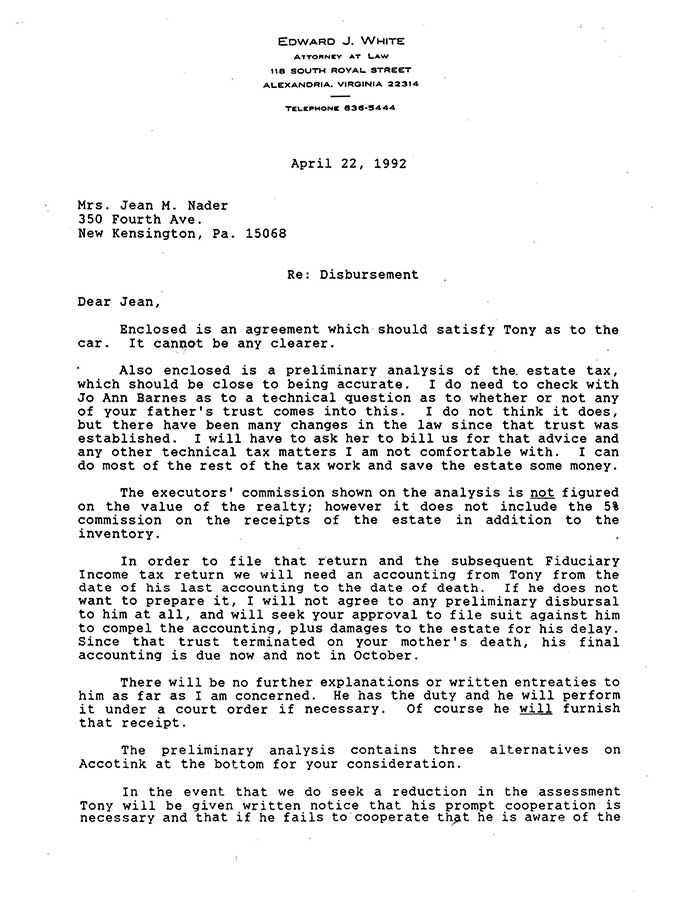

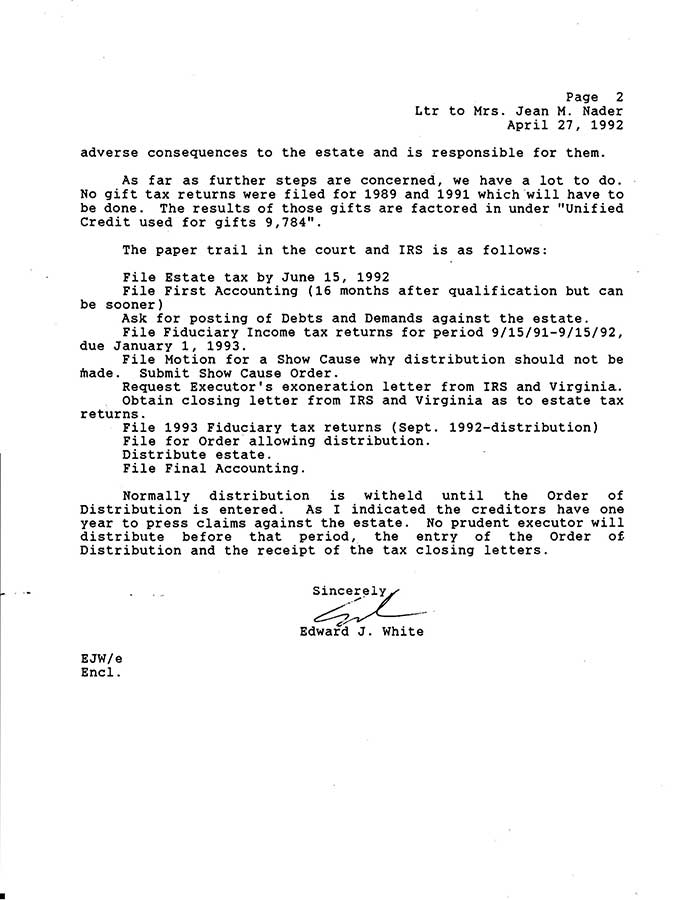

1992.02.18 (Edward White to Anthony O'Connell, copy to Jean Nader)

"Re: Estate of Jean M. O'Connell,

Dear Mr. O'Connell,

In order to prepare your mother's 1991 income tax returns, I need the amount that the Harold O'Connell Trust paid her during 1991. In the event the payment was not made in 1991, I will need to file the amount which was due as "income with respect to a decedent" on the estate tax and fiduciary tax returns. The cutoff date for your computation will be September 15, 1991. After that date the trust technically terminated, and the income belongs to the beneficiaries of that trust.

Jean and I are making progress on the estate. We have decided to leave the A. G. Edwards accounts in place since they are earning a better rate of return than a bank can give.

I am trying to get to the bottom of the car problem with Sovran and should be able to get the title soon so that it can be transferred to you before the insurance expires.

Jean has informed me that you and your sisters have decided that it is best to try and list the Accotink property at its actual value as of the of death rather than a higher value based on its future value. Since you have worked so diligently on this problem in the past, could you give me the name of an appraiser who could do a valuation which will take into account all of the county inspired problems. It seems to me that the county value of $600,000.00 is too high based on the hurdles you have run into in trying to develop it.

Could you also send me the address of Lynch Properties?

Sincerely, Edward J. White"

1992.02.25 (Edward White to Anthony O'Connell, copy to Jean Nader)

"I have received your letter of February 24, 1992 in which you request that I reconsider my refusal to resign as co-executor of your mother's estate.

Once more I decline to take such action.

When your mother approached me about changing the co-executors of her will, we discussed the matter at length. She specifically desired to make the changes which are in effect now, and was quite firm in her decision. It would be clearly disloyal of me to dishonor her intentions.

If you are represented, I will be glad to discuss this matter with your counsel.

Sincerely, Edward J. White"

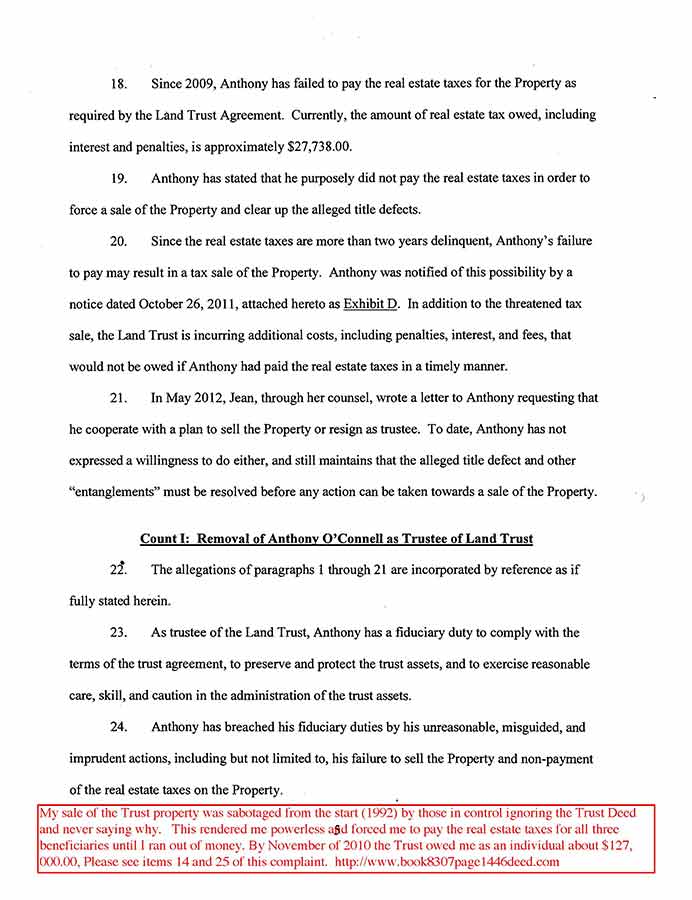

1992.02.27 (Edward White and Jean Nader to Nuveen Unit Transfer Dept) (No copy to another)

"We are the Co-Executors of the estate of Jean M. O'Connell who died on September 15, 1991.

You are requested to transfer the entirety of this account to (hand written- the estate of Jean M. O'Connell) A. G. Edwards & Sons, Inc, c/o Allison May, 524 King Street, Alexandria, Va. 22314.

Enclosed is a W-9 form, a name affidavit and a current letter of appointment.

Sincerely, Edward J. White"""""""""""" Jean M. O'Connell Nader Co-Executors, Estate of Jean M. O'Connell"

Title of new account: Edward J. White & Jean M. Nader co-executors of the estate of Jean M. O'Connell 118 S. Royal St. Alexandria, Va. 22314 ID # 25-637-7917" (Hand written)

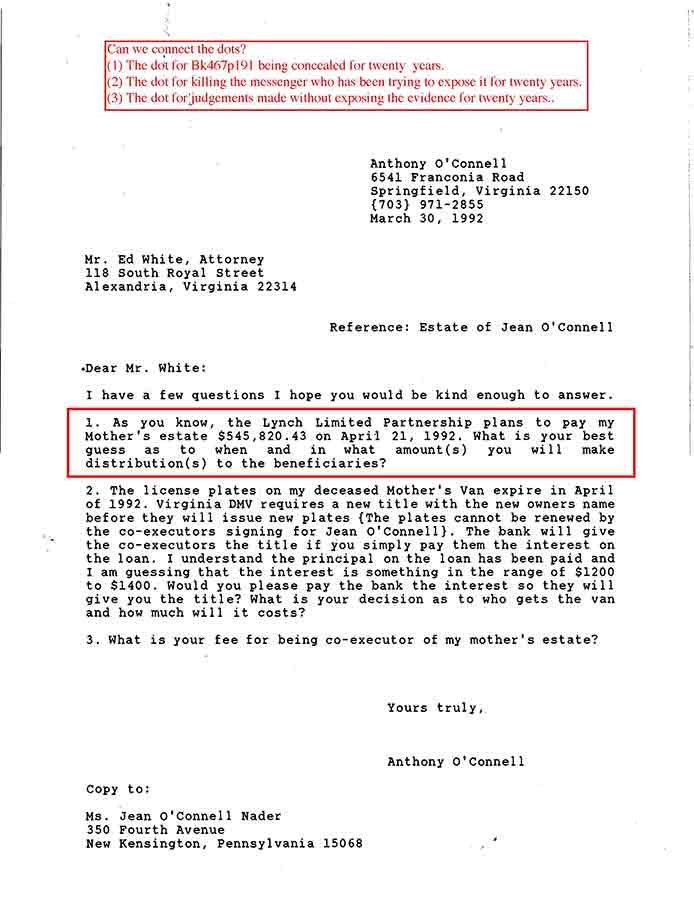

1992.03.31 (Edward White (using Jean Nader to mail it) to Anthony O'Connell)

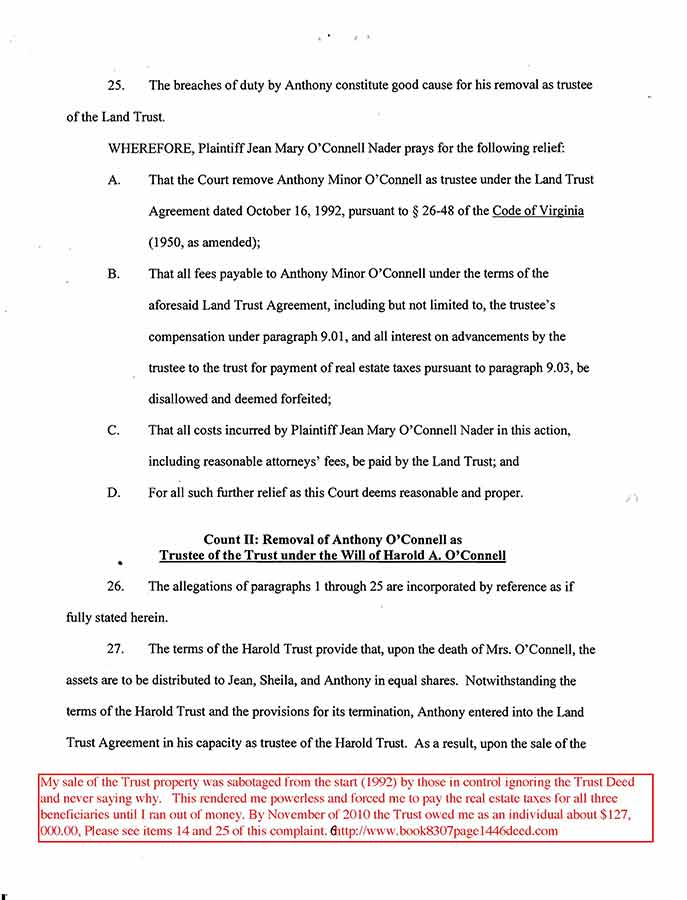

"Dear Tony

I hope you are having a good day-

Enclosed is

(1) the Van Title,

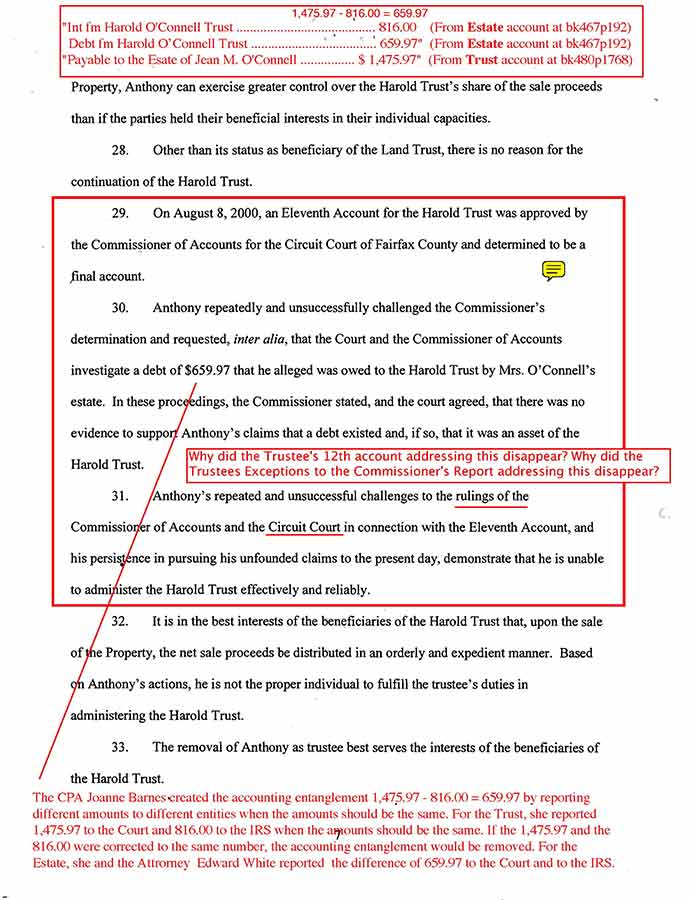

(2) a death certificate

(3) a court appointment and a

(4) receipt.

You need # 1, 2, 3 to have the van transferred to your name-

The receipt # 4, must be returned to me or Ed White as soon as possible because it must be filed with our accounting to the court-"

Enclosure:

"Received of the Estate of Jean M. O'Connell, one 1988 Plymouth Station Wagon of a value of $8,000"

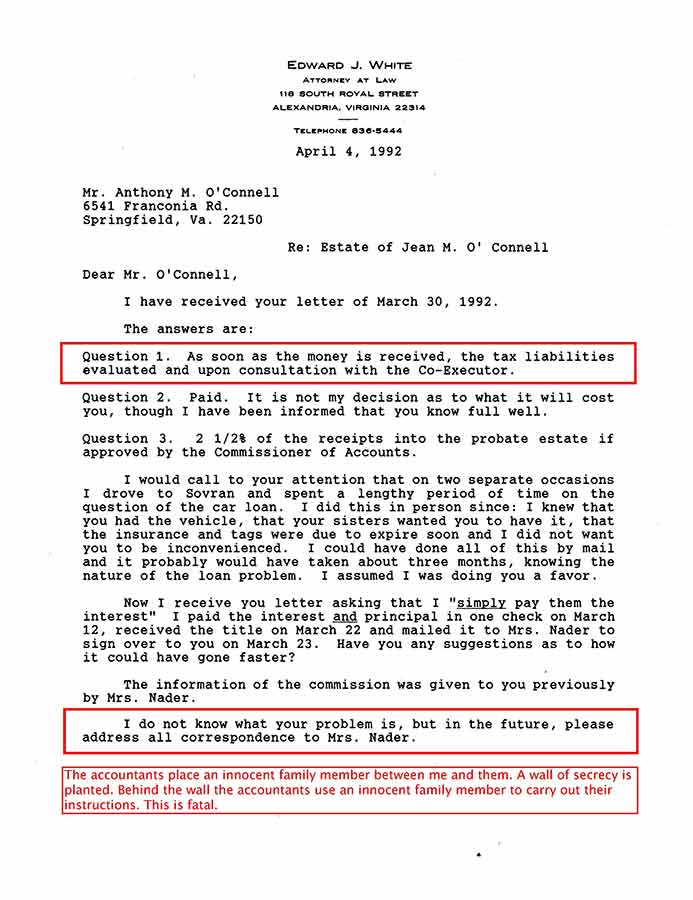

1992.04.04 (Edward White to Anthony O'Connell, copy to Jean Nader)

"I have received your letter of March 30, 1992.

The answers are:

Question 1. As soon as the money is received, the tax liabilities evaluated and upon consultation with the Co-Executor.

Question 2. Paid. It is not my decision as to what it will cost you, though I have been informed that you know full well.

Question 3. 2 Y % of the receipts into the probate estate if approved by the Commissioner of Accounts.

I would call to your attention that on two separate occasions I drove to Sovran and spent a lengthy period of time on the question of the car loan. I did this in person since: I knew that you had the vehicle, that your sisters wanted you to have it, that the insurance and tags were due to expire soon and I did not want you to be inconvenienced. I could have done all of this by mail and it probably would have taken about three months, knowing the nature of the loan problem. I assumed I was doing you a favor.

Now I receive you letter asking that I "simply pay them the interest" I paid the interest and principal in one check on March 12, received the title on March 22 and mailed it to Mrs. Nader to sign over to you on March 23. Have you any suggestions as to how it could have gone faster?

The information of the commission was given to you previously by Mrs. Nader.

I do not know what your problem is, but in the future, please address all correspondence to Mrs. Nader.

I am trying to be patient with you, but I find that this estate is time consuming enough without having to deal with letters such as the last two that I have received.

Sincerely, Edward J. White"

Frame me with 659

Frame me with 659

Frame me with 659

Frame nme with 659

Frame me with 659

Ignore 659

Make 659

disappear. Frame me.

Make 659 disappear. Frame me.

make 659 disappear Frame me. Remove me as Trustee for trying to get it recognized.

entanglement using car as $8000.00 gift-estate tax interplay)

16. In addition, Mr. White timely requested an extension for

filing the decedent's last income tax return and therefore no penalties were involved. As justification for the delay, Mr. White points out that he experienced some delay in obtaining the K-1 from you and your own complaint appears to concede that there was a problem with getting the K-1 to Mr. White. 16

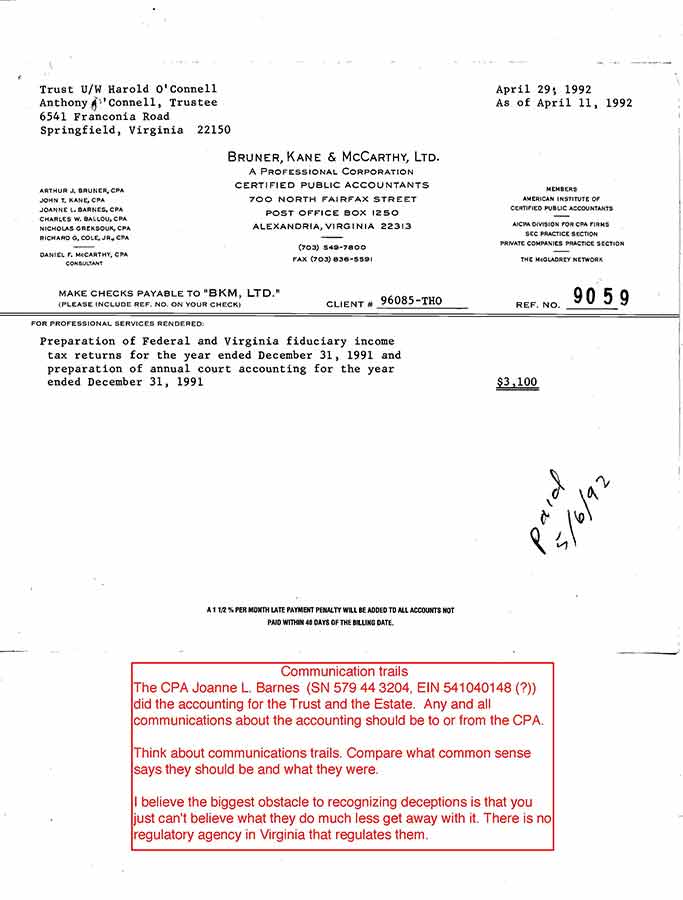

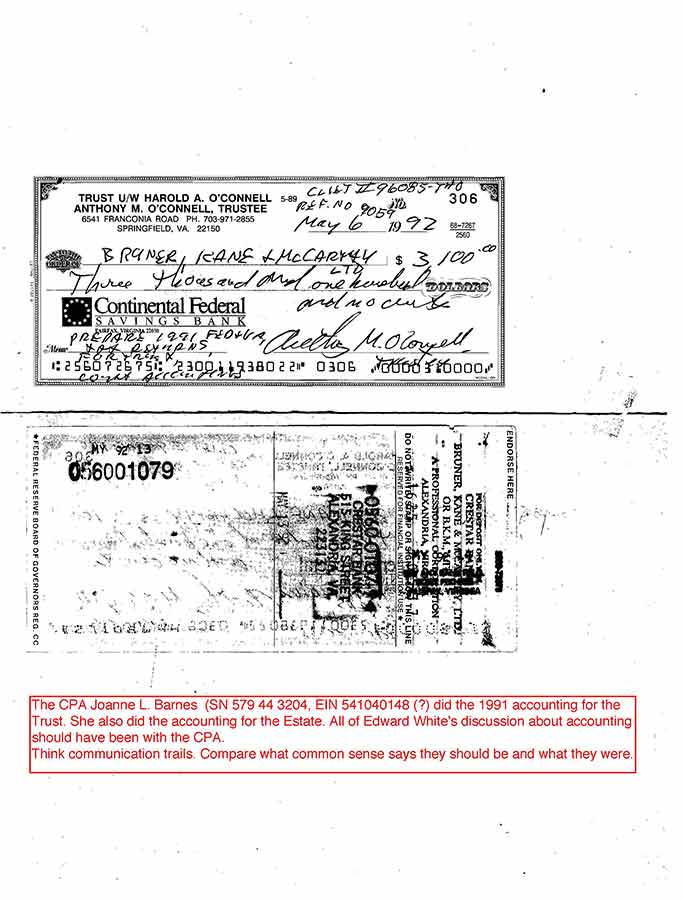

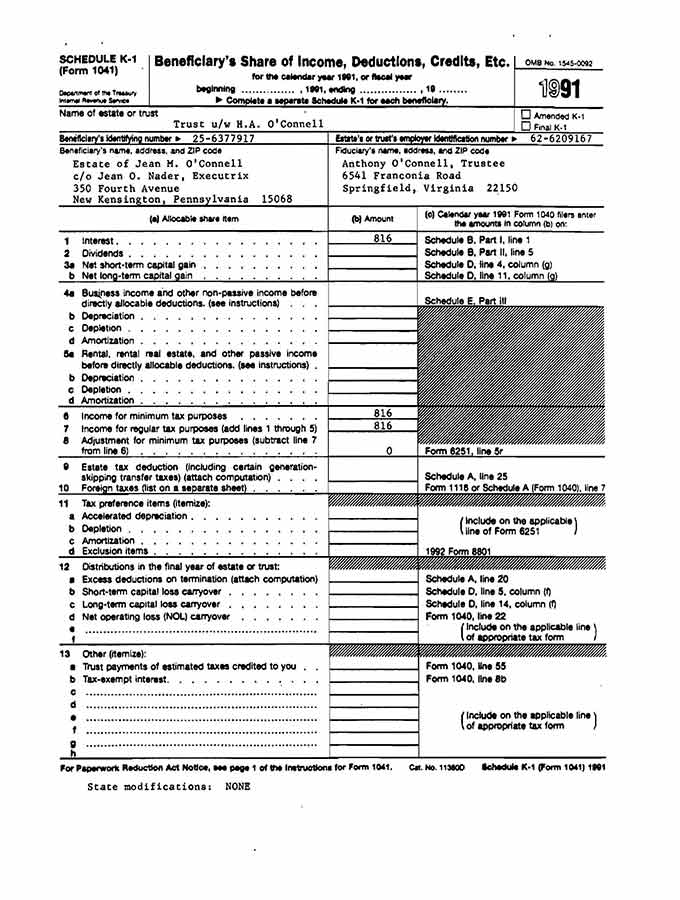

16 The CPA Joanne Barnes did the accounting for the Trust and the Estate. This would mean that the CPA was late in getting the K-1 to herself.

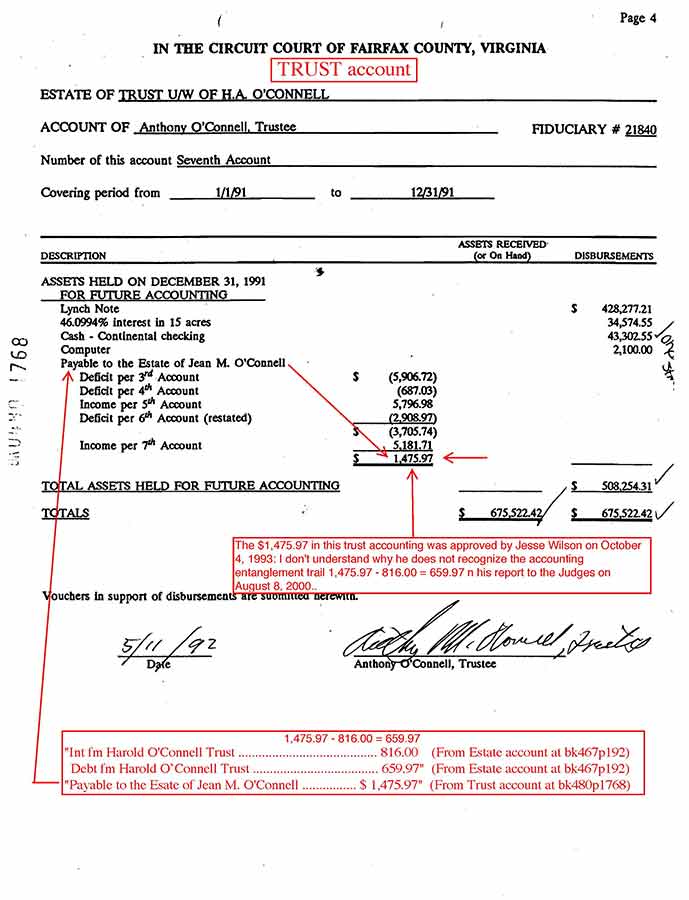

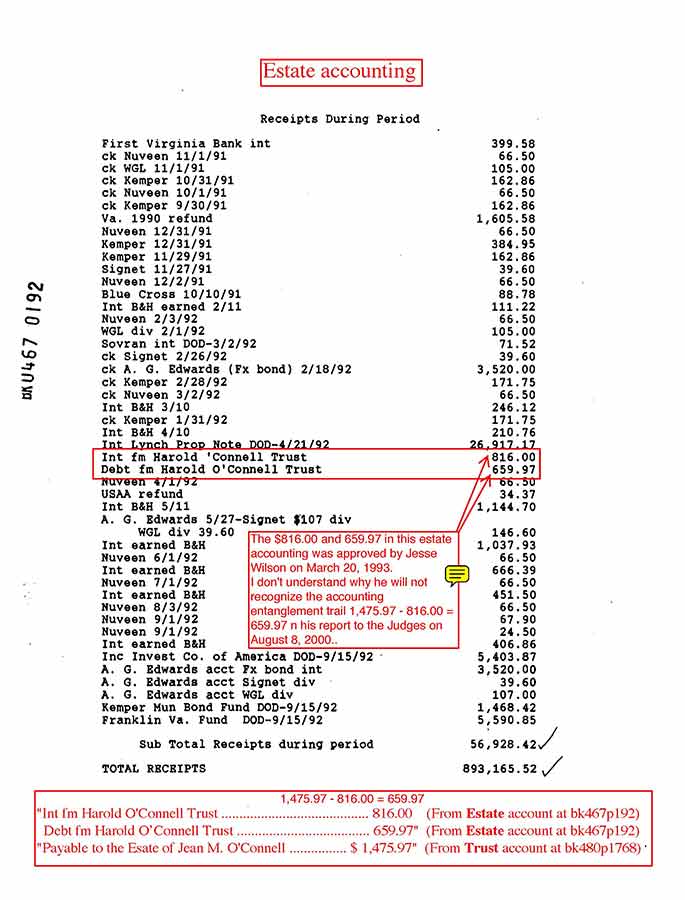

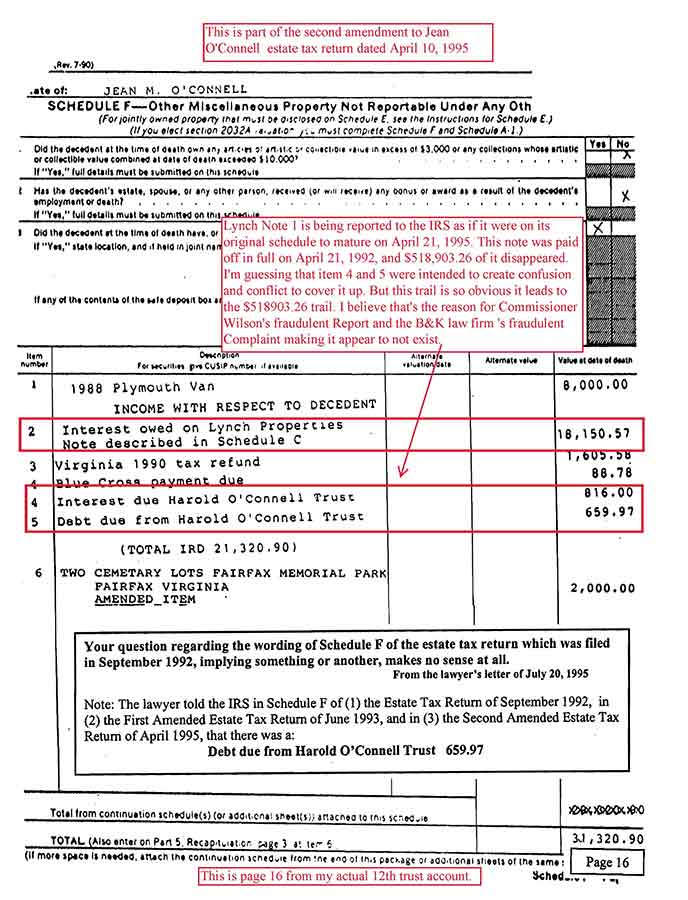

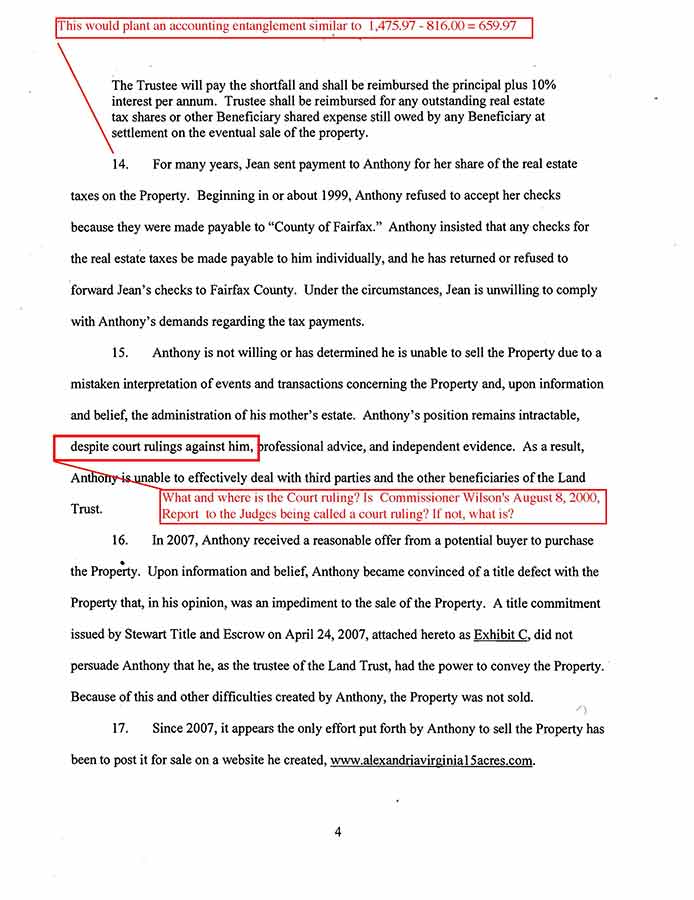

The AE (accounting entanglement) 1,475.97 - 816.00 = 659.97 covers the disappearance of $518, 903.26 (545,820.43 - 26,91717 = 518,903.26). History suggests the intent was to cover-up the dissappearance of the $518,903.43. That I'm made responsable for 1,475.97 - 816.00 = 659.97t, and the K-1 with its 816.00 further evidence to support that.

I believe these documents and transcripts are self explanatory. Basically, they frame me with the AE (accounting entanglement) 1,475.97 - 816.00 = 659.97. After I brought attention to the 659.97 its made to appear as if it doesn't exists. One indicator of its importance is the degree the Commissioner of Accounts and the B&K law firm cover it up. Small numbers are used to create accounting entanglements. as if the issue were the amount and not that they entangle. The issue is that they entangle.

See note 16

The AE 1,475.97 - 816.00 = 659.97 covers the 545,820.43 - 26,91717 = 518,903.26

1992.05.19 (Edward White to Anthony O'Connell, c/o E.A. Prichard, copy to Jean Nader)

"In your letter of May 6 to Jean you asked that I communicate with you with regard to the Harold O'Connell Trust.

I am trying to prepare the estate tax, and as usual in these cases, there are problems trying to understand the flow of debts and income.

I do have a few questions which are put forward simply so that the figures on the Trust's tax returns and accounting will agree with the estate's.

1. The K-1 filed by the Trust for 1991 showed income to your mother of $41,446.00. The Seventh Accounting appears to show a disbursement to her of $40,000.00 plus first half realty taxes paid by the trust for her and thus a disbursal to her of $1794.89. If these two disbursals are added the sum is $41,794.89. This leaves $348.89 which I cannot figure out. It could well be a disbursal of principal and not taxable.

2. The K-1 filed by the Trust showed a payment of $816.00 in interest to the estate. You sent a check in the amount of $1475.97 to the estate. What was the remaining $659.97? Do I have this confused with the tax debt/credit situation which ran from the Third Accounting?

3. On the Seventh Accounting "Income per 7th Account" is shown as $5181.71, but I cannot figure that one out either.

I am of the opinion that the estate owes the trust for the second half real estate taxes from September 15, 1991 through December 31, 1991 in the amount of $1052.35. This is shown on your accounting a disbursed to the heirs. Should this be paid back to the heirs or to the Trust?

I believe that the income received from the savings accounts from September 15 to the date the various banks made their next payment to the Trust (9/30 and 9/21) should be split on a per diem basis, since the Trust terminated on her death. This will be a small amount of course.

Are there any other debts which your Mother owed the Trust?

I realize that Jo Ann Barnes prepared this and if you authorize it I can ask her to help me out.

Please understand that I have no problem with the Accounting, I m just trying to match things up. In the long run, since the beneficiaries are the same, the matter is academic. Please send the bill for the appraisal whenever you receive it. Jean is filing the Fairfax form for re-assessment in her capacity as a co-owner in order to give us a better basis to get this assessment changed and to meet the county's deadline. It will state that the appraisal you have ordered will follow. I think this will be to all of your benefit in the long run.

Sincerely, Edward J. White"

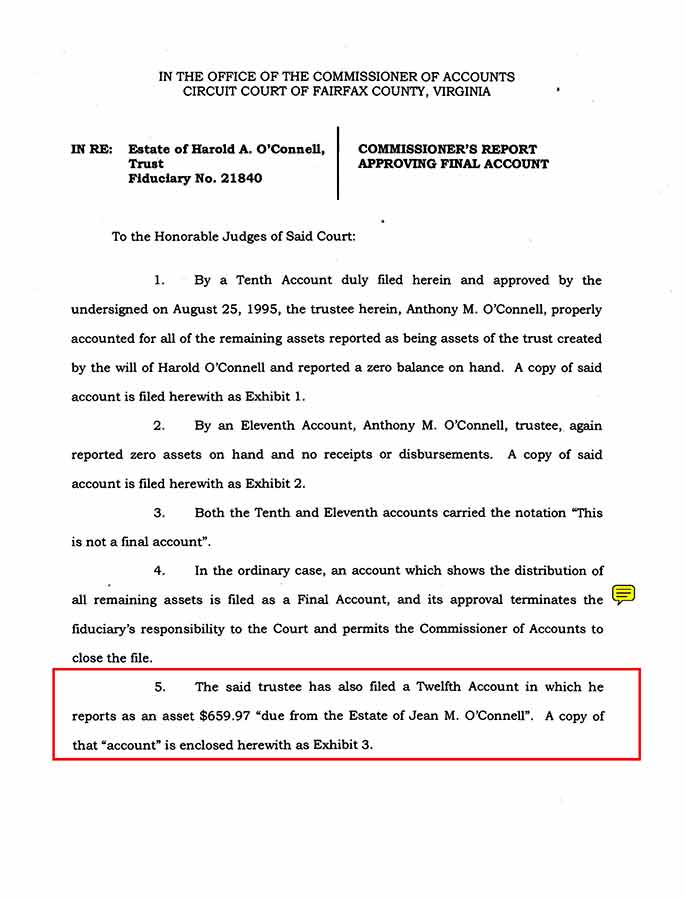

2000.08.08 (Jesse Wilson's Report to the Judges)

"To the Honorable Judges of Said Court:

RE: Estate of Harold A. OConnell, Trust

Fiduciary No. 21840

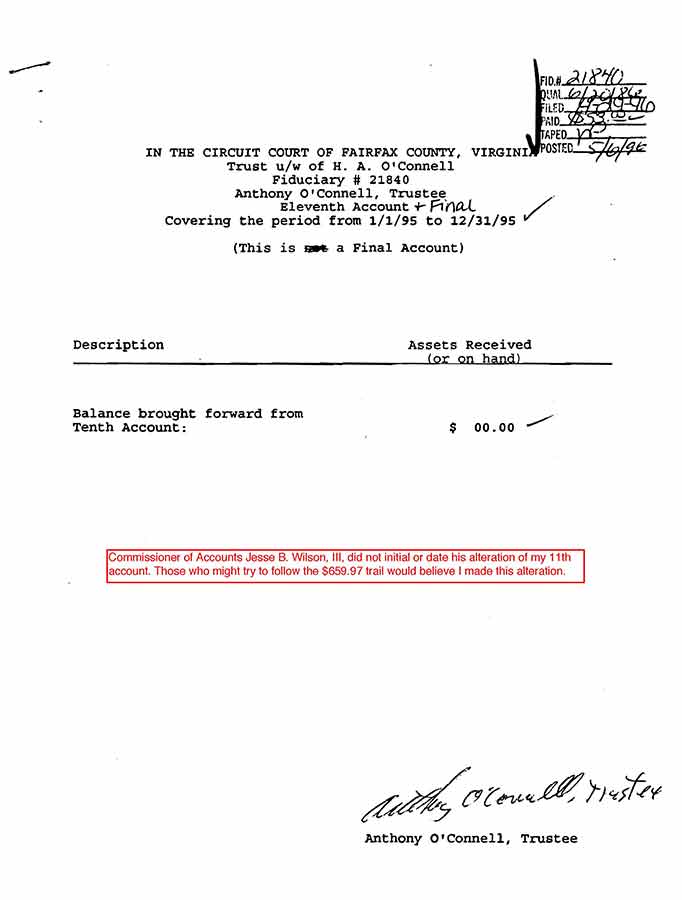

1. By a Tenth Account duly filed herein and approved by the undersigned on August 25, 1995, the trustee herein, Anthony M. 0'Connell, properly accounted for all of the remaining assets reported as being assets of the trust created by the will of Harold OConnell and reported a zero balance on hand. A copy of said account is filed herewith as Exhibit 1.

2. By an Eleventh Account, Anthony M. OConnell, trustee, again reported zero assets on hand and no receipts or disbursements. A copy of said account is filed herewith as Exhibit 2.

3. Both the Tenth and Eleventh accounts carried the notation "This is not a final account".

4. In the ordinary case, an account which shows the distribution of all remaining assets is filed as a Final Account, and its approval terminates the fiduciary's responsibility to the Court and permits the Commissioner of Accounts to close the file.

5. The said trustee has also filed a Twelfth Account in which he reports as an asset $659.97 "due from the Estate of Jean M. OConnell". A copy of that "account" is enclosed herewith as Exhibit 3.

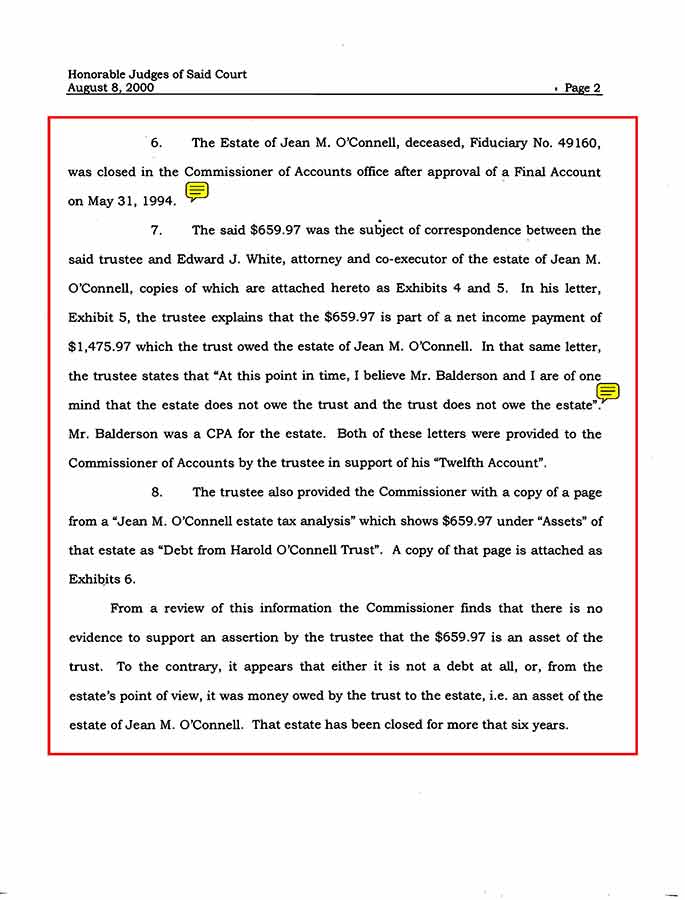

6. The Estate of Jean M. OConnell, deceased, Fiduciary No. 49160, was closed in the Commissioner of Accounts office after approval of a Final Account on May 31, 1994.

7. The said $659.97 was the subject of correspondence between the said trustee and Edward J. White, attorney and co-executor of the estate of Jean M. OConnell, copies of which are attached hereto as Exhibits 4 and 5. In his letter,

Exhibit 5, the trustee explains that the $659.97 is part of a net income payment of $1,475.97 which the trust owed the estate of Jean M. OConnell. In that same letter, the trustee states that "At this point in time, I believe Mr. Balderson and I are of one mind that the estate does not owe the trust and the trust does not owe the estate".

Mr. Balderson was a CPA for the estate. Both of these letters were provided to the Commissioner of Accounts by the trustee in support of his "Twelfth Account".

8. The trustee also provided the Commissioner with a copy of a page from a "Jean M. OConnell estate tax analysis" which shows $659.97 under "Assets" of that estate as "Debt from Harold OConnell Trust". A copy of that page is attached as Exhibits 6.

From a review of this information the Commissioner finds that there is no evidence to support an assertion by the trustee that the $659.97 is an asset of the trust. To the contrary, it appears that either it is not a debt at all, or, from the estate's point of view, it was money owed by the trust to the estate, i.e. an asset of the estate of Jean M. OConnell. That estate has been closed for more that six years.

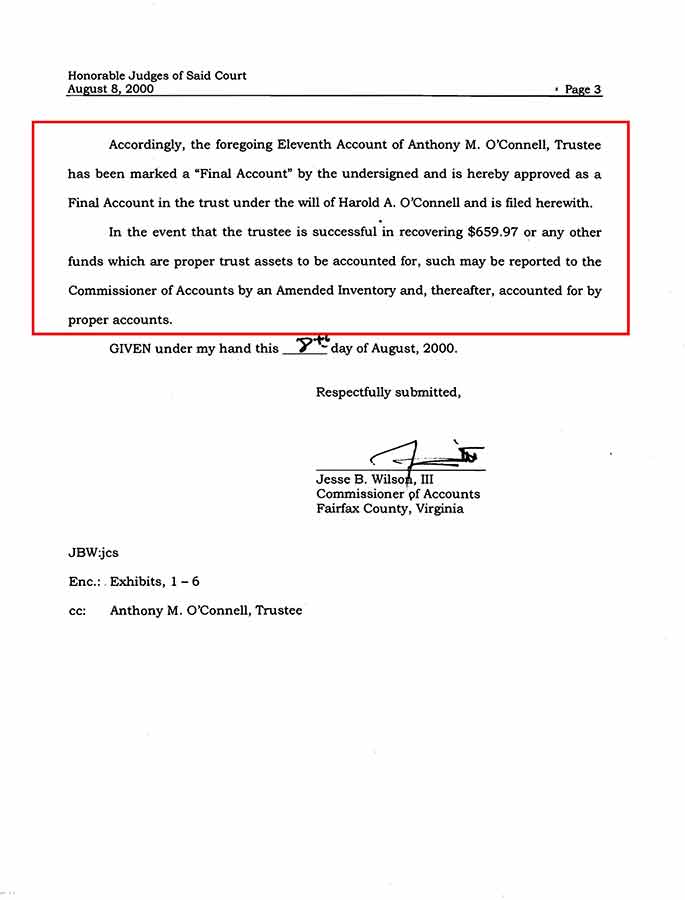

Accordingly, the foregoing Eleventh Account of Anthony M. OConnell, Trustee has been marked a "Final Account" by the undersigned and is hereby approved as a Final Account in the trust under the will of Harold A. OConnell and is filed herewith.

In the event that the trustee is successful in recovering $659.97 or any other funds which are proper trust assets to be accounted for, such may be reported to the Commissioner of Accounts by an Amended Inventory and, thereafter, accounted for by proper accounts.

GIVEN under my hand this 8th day of August, 2000.

Respectfully submitted,

Jesse B. Wilson, III

Commissioner of Accounts

Fairfax County, Virginia

JBW:jcs

Enc.: Exhibits, 1 - 6

cc: Anthony M. OConnell, Trustee"

(See the exhibits in the pdf reference)

From the Complaint against me prepared by the B&K law firm (above).

|