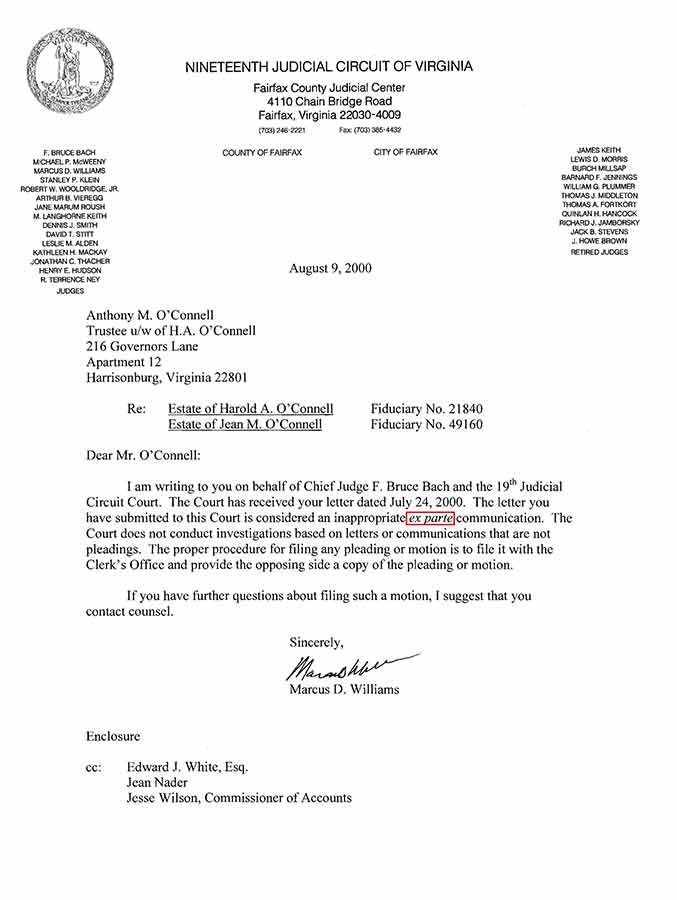

2000 JudgesWhy would my July 24, 2000, letter to the Judges explaining our family's predictiment be labeled ex parte (inappropriate) communication? 2000-judges-121p

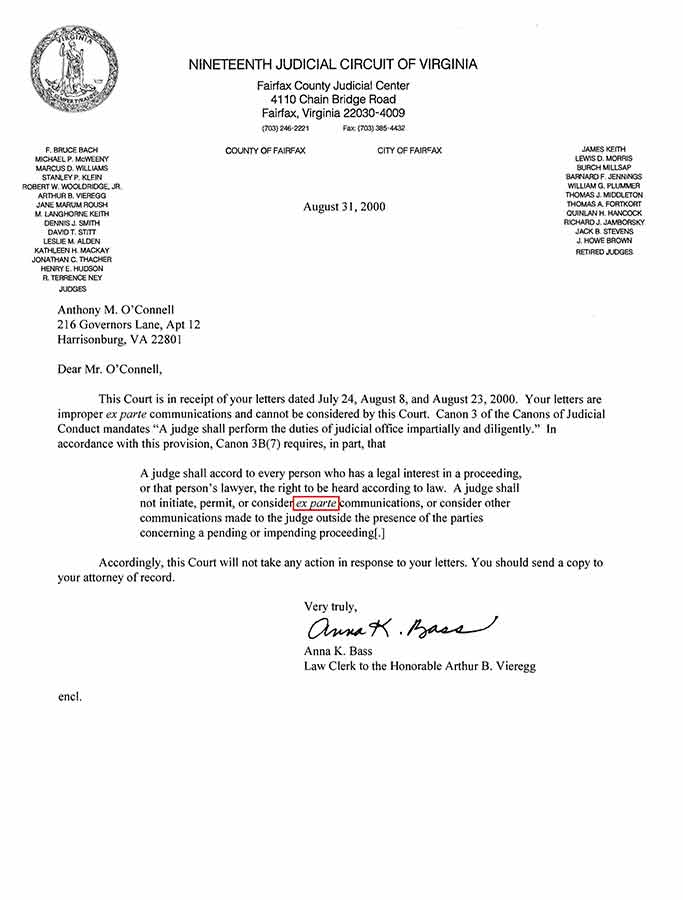

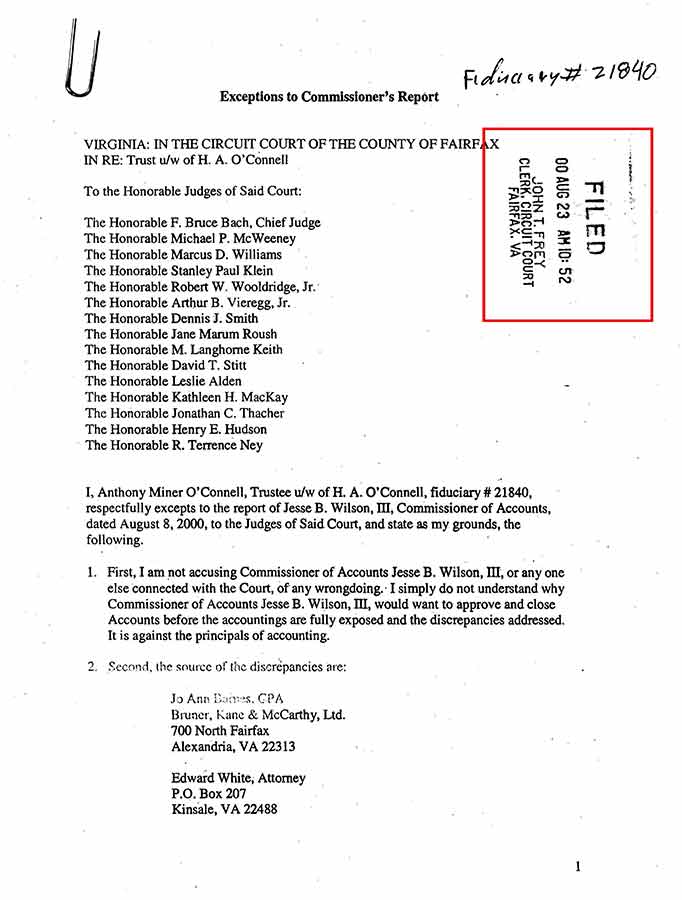

Instead of exposing the accounting, the Commissioner of Accounts closed my accounting for the Trust. My Exceptions to this disappeared after being received by the Court on August 23, 2000. Why did my 1994 Exceptions disappear after being received by the Court? Exceptions1994-4p Why did my 2000 Exceptions disappear after being received by the Court? Exceptions2000-52p This means something is wrong and it should be corrected. |

| Jean O'Connell Nader* 350 Fourth Avenue New Kensington, PA 15068 |

Co-executor of the Estate (Innocent) Beneficiary of the Trust u/w of H. A. O'Connell Beneficiary of the Land Trust containing Accotink |

| Sheila O'Connell* 44 Carleton Street Portland, ME 04012 |

Beneficiary of the Estate Beneficiary of the Trust u/w of H. A. O'Connell Beneficiary of the Land Trust containing Accotink |

| Anthony M. O'Connell 216 Governors Lane, Apt 12 Harrisonburg, VA 22801 |

Trustee for the Trust u/w of H. A. O'Connell (Primary beneficiary is Jean M. O'Connell) Trustee for the Land Trust containing Accotink Beneficiary of the Estate Beneficiary of the Trust u/w of H. A. O'Connell Beneficiary of the Land Trust containing Accotink |

*The secret advisors have destroyed my credibility with my sisters, Jean Nader and Sheila O'Connell. Please expect the secret advisors to use my sisters to carry out their advice; such as to keep accountings secret and to contest me. A similar thing would happen if the Trustee tried to sell Accotink. This is why I have to get a just power to intervene. My sisters, Jean Nader, and Sheila O'Connell, will never believe me unless a just power intervenes.

Innocent family member set up

Jo Anne Barnes and Edward White have protected themselves against the traditional avenues of justice through the Court by installing (1985) and using an innocent family member to unwittingly carry out their agenda. If I file charges in Court they will have me in a mutually destructive contest with an innocent and unbonded member of my own family, Jean Nader. The only thing Jean Nader is doing wrong is to trust the secret advisor's advice. But I can not stop them from doing that. I tried to get around the innocent family member set-up:

a. I wrote the Virginia Bar in 1992 (Jean Nader is not a member of the Bar). This did not work. The Bar advised me to use the traditional paths of the Court. That would put me in a mutually destructive contest with the innocent family member.

b. I wrote a book about how I believed the operation worked and mailed it out to public officials in 1997. This did not work. If that book made people angry I am sorry, but I am supposed to try to protect Jean M. O'Connell's family and assets, and the traditional paths of justice are blocked with the innocent family member set up.

I can think of only three things that a just power could do with the innocent family member setup:

a. Continue to let them steal money to avoid punishing the innocent family member (which is why the secret advisers use the innocent family member to carry out their agenda).The secret advisors have set it up so that they can financially ruin Jean Nader before allowing accountings to be exposed ( They Steal Money, page 10). They will use all their power to keep using Jean Nader as a cover under the guise that they are protecting her.

b. Stop them from stealing money and punish the innocent too (Jean Nader is too innocent and scared to separate from them on her own. At this point I believe the secret advisors have so traumatized Jean Nader that she is fear driven, that they could have her do most anything to avoid having the estate accounting exposed. A just power or their agent could verify this by a personal visit to Jean Nader).

c. First separate and protect the innocent family member from the secret advisors, and then stop the secret advisors. This is the only fair choice. But I don't know how that could be done. I have tried for nine years.

The innocent family member, Jean O'Connell Nader, is their protection. They are not going to let her go. She is the key. Only a Judge, I believe, has the discretionary power to stop the secret advisors from continuing to use the innocent family member. If a Judge can not stop them from doing this, I believe no one can, and the innocent family member setup and the secrecy truly make Jo Ann Barnes and Edward White untouchable.

Unless a just power convinces Jean Nader to stop letting the fraud operation use her the Testators family will remain helpless against them.

(10) New accounting. A new accounting by an objective outsider is absolutely essential. Only a Judge could, I believe, order a new accounting of the Estate of Jean M. O'Connell by an objective outsider.

The secret advisors have intentionally created so much ambiguity, confusion, accounting entanglements, setups, coerced or forced signing of documents, commingling of what should have been an asset of the estate with the beneficiaries individual finances, that it is impossible to unravel. They do that so that it is near impossible to unravel and to see what they have done. There is cover after cover after cover. Their accounting is confusion and deception where money disappears.

Please do not charge a new accounting to the testator's family who has no control over the CPA-lawyer-stockbroker accounting. History suggests that the first thing the secret advisors will do is to advise the innocent family member that it will be an additional cost to her and led her to believe that I am costing her money.

Please set aside all the documents they had the beneficiaries' sign that covers the secret advisors. If I refuse to sign a document I should not sign, the secret advisors withhold my distribution and put the family through a " ... I merely asked for a receipt so that a proper accounting might be filed, Mr. O'Connell has tried one stunt after another to disrupt the flow of administration, not withstanding my repeated attempts to calm him down."

The new accountant should compare the secret advisors versions of the accountings sent to the IRS, to the Court, to and from the stockbroker, to the innocent family member, etc. The pattern is that many' if not most of the deceptions are exposed by comparing the different versions sent to different entities.

(11) My credibility. I am the one they most want to not see their accountings. I have an MBA, I have worked for the IRS and most everything I have or have lost depends on exposing their accountings. They destroyed my credibility because they don't want my family and others like you to believe me.

One way to verify fraud that does not involve accounting is to compel Jo Anne

Barnes and Edward White (not the innocent family member who they have set up to carry this out for them) to identify in writing exactly what it is that they have accused me of for the past fifteen years. Allow me to respond if they do. They should have some reason, other than my having experience in accounting and trying to expose theirs, for destroying my reputation and rendering the testator's family helpless. They don't. If a Judge can't pin them down to an unaccountable position on this please understand how the public and I can't (From the lawyer's letter of July 20, 1995: For the umpteenth time, I will ignore your plaintive request that I identify your "wrongdoings"). I can't defend myself against something they won't identify. For them this was just another cover to steal money. For me it was my life. At this point, if any weight at all is given to the number and power of people who have been led to believe whatever Jo Anne Barnes and Edward White have implied against me, it is hopeless. I beg you, I literally get down on my knees and beg you, to pin Jo Anne Barnes and Edward White down to an unaccountable position on this.

My sisters will never believe Jo Ann Barnes and Edward White have framed me over the past fifteen years unless a just power tells them. Only a Judge, I believe, could compel them to take an accountable position on this.

(12) It is impractical to list all the traps and covers for investigators that I know about and I don't know them all. Please forward each excuse/reason why they won't provide a true and full financial disclosure and allow me to respond. Please do not leave me out of the information loop. I know more about the traps for investigators than among anyone who has come forward. I am the one whom they most want to not see their accountings. Please do not relinquish control of this to anyone until exposure is complete and I have one hard copy in my hands. About one million dollars in real estate is at stake.

Please do nothing if not committed from the start for a 100% true and complete financial disclosure with one hard copy in my hands. Exploratory or tentative investigation is worse than none because the investigator will encounter a mountain of convincing cover, which the investigator won't recognize as cover, and the investigation stops, and it results in another de facto approval.

If you do not intervene I would like the Court to know that I have done everything I could to try to expose the accountings, to stop them from stealing money, and to free Accotink from their control.

The secret advisors operate behind impenetrable secrecy. It is impossible to get to the truth or to prove something when the evidence is kept secret. The secret advisors do not want me to understand their set ups much less be able to document them to others. Because of the impenetrable secrecy that the secret advisors operate behind, everything in this letter and all of it's enclosures is only my own personal opinion.

But if you compel a 100% true and complete exposure of the CPA-lawyer-stockbroker accounting for the Estate, with one hard copy of it in my hands, and it is reviewed by a just power, I believe that it will show that this is true:

- The CPA Jo Anne Barnes and the Lawyer Edward White are two principals in a fraud operation that stole money from the Estate of Jean M. O'Connell.

- They took covert control of about a million dollars in real estate (B8845 p1444 and B8037 p1446) by entangling it in their accounting of the Trust and the Estate and made it appear as if I was the cause of it.

- They destroyed the Testator's family to protect themselves.

- They destroyed my reputation because I have experience in accounting and they do not want my family and other's like you to believe what I am telling you.

Sincerely,

(seal)

Anthony M. O'Connell, Trustee u/w of H. A. O'Connell

Enclosures:

They Steal Money

Jean M. O'Connell

CD contains the following files:

They Steal Money

Jean M. O'Connell

Testator

CPA

Stockbroker

Innocent Family Member

Fear

Render Testator's Family Helpless

They Use The Trust of Judges

Sabotage Sale, 1988

Sabotage Sale, Again

My Credibility

Correspondence with Judge Thomas S. Kenny

Copies to:

Jo Ann Barnes, CPA

Edward White, lawyer

Allison May, stockbroker

Commissioner of Accounts Jesse B. Wilson III

Assistant Commissioner of Accounts Henry C. Mackall

Deputy Commissioner of Accounts Peter A. Arntson

SEC Commission

IRS

VA Bar

Jean Nader

Sheila O'Connell"

(13 enclosures follow)

They Steal Money

Summary

One way they stole money was to use two versions of the Estate Tax Return with payment. These are not amendments or corrections, but two separate versions with the same dates. There is only supposed to be one. The innocent family member sent me a copy of a $175,000 version, which suggests that this was the version that was sent to her.

The $1 19,000 version appears to be a doctored version of this $175,000 version (page 3).

Based on the known accounting, the secret advisors sent the innocent family member the

$175,000 version for signature and payment, then doctored that $175,000 version to read

$119,000, and sent the $119,000 version with a $119,000 payment, and not the $175,000 payment, to the IRS. The basic difference between the $175,000 payment and the $119,000 payment disappeared from their accounting (page 5). Money is not supposed to disappear. If Jean Nader were not totally innocent she would not have sent me a copy of the $175,000. The two versions of the Estate Tax Return are exposed because of this temporary break in the secrecy.

$175.000 version for innocent family member to sign

(a) Extension Request, IRS Form 4768 - dated June 11, 1992. Payment has to be included with this IRS Form 4768 (Page 1).

(b) Estate Tax Return, IRS Form 706 - dated September 2 and 8,1992 (Page 2)

$119,000 version actually sent to the IRS

(a) Extension Request, IRS Form 4768 - dated June 11, 1992. This $119,000 version is a doctored version of the $175,000 version (Page 3).

(b) Estate Tax Return, IRS Form 706 -Missing. There has to be a $1 19,000 version of the IRS Form 706 somewhere (Page 4).

(See the pdf reference for the 10 pages of documents that are not included here)

Jean M. O'Connell

The testator, Jean M. O'Connell, gave to Virginia. She was a nationally recognized landscape designer who did the landscape designs, without compensation, for:

The Franconia Olivet Episcopal Church.

The Springfield Richard Byrd Library.

The Commonwealth Hospital in Fairfax,

The Louise Archer Elementary School.

Grandview Farmhouse and mini-pavilion, a National Trust for Historic

Preservation property at Woodlawn.

A memorial garden in the National Arboretum.

The Northern Virginia Mental Health Institute.

The Woodbridge Methodist Church.

The 18" century Magruder House of the Prince George Historical Society.

The Wolf Trap Elementary School.

The Pope-Leighey House by Frank Lloyd Wright.

The Fair Oaks Hospital.

The Clifton Episcopal Church.

The Oakton Elementary School.

The 4-H Club Headquarters near Front Royal,

The roadbed of the abandon W & 0 Railroad in Vienna

The Springfield Junior Chamber of Commerce-commercial area plantings.

The Knoll Garden, Goodwill House West, in Falls Church.

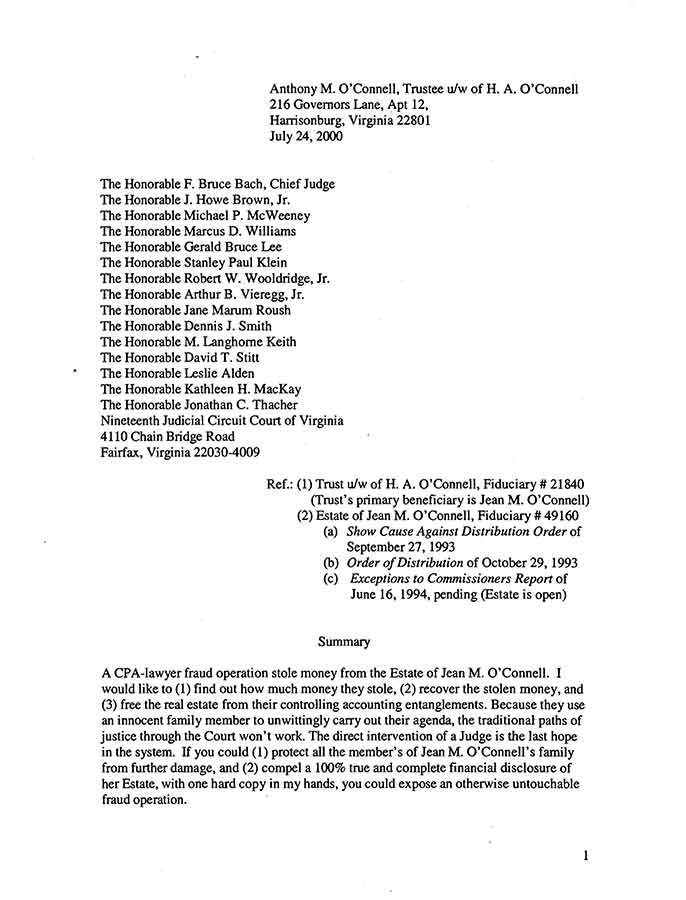

Because the personal intervention of a Judge is the last hope in the system, I beg the

Judges of the Nineteenth Judicial Circuit Court to personally intervene, and protect all the testator's family and assets from further damage."

Testator

Summary

There were no conflicts among any members of Jean M. O'Connell's family concerning any Will or any Trust before the secret advisors ran their set ups. The secret advisors set up Jean M. O'Connell. They used her trust to take control of her assets and to render her and her family helpless against them (page 3).

The secret advisors create conflicts in the testator's family to protect themselves. It is a cover for the secret advisor's activities. Any time the secret advisors divert accountability from themselves to the testator's family, as if they were just carrying out one family member's instructions against another, please reject it and any variation of it.

Jean M. O'Connell gave a lot to Fairfax County and Virginia (page 1). I beg a just power to step in and stop the damage."

(See the pdf reference for the 8 pages of documents that are not included here)

CPA

Summary

Secrecy prevails. There are no known letters from Jo Anne Barnes that would document her advice to the innocent family member between her two letters of November 25, 1991 and September 30, 1994, the most active period of the estate. The CPA's first letter volunteers to the innocent family member that she would be happy to work with Mr. White (page 1). The CPA's second letter directs the innocent family member to sign a document stating that the Estate is closed (pages 2 and 3)."

(See the pdf reference for the 3 pages of documents that are not included here)

Stockbroker

Summary

Secrecy prevails. The innocent family member sent me copies of two documents (pages 1 and 2). I believe the stockbroker launders the stolen money."

(See the pdf reference for the 3 pages of documents that are not included here)

Innocent Family Member

Summary

The secret advisors frame their clients with their accounting. To avoid accountability they use the trust of an innocent family member to carry out their agenda:

Page 1: Commingle funds. Obfuscates accountings and entangles assets like Accotink.

Page 2 and 3: Secrecy prevails. They have the innocent family member carrying out their agenda to the degree that the secret advisor's name(s) are secret.

Page 6: Ties another knot in the real estate tax entanglement the CPA and lawyer put on Accotink.

The only thing the innocent family member is doing wrong is to rely on the advice of the secret advisors. But I can not stop that. If they can get away with using the innocent family member to steal money from the Estate while they are under Court jurisdiction and review, they can get away with most anything using the innocent family member and their accountings entanglements in a sale of Accotink. Please see what they got away with in Sabotage Sale, 1988.

Unless a just power stops the secret advisers from continuing to use the innocent family member, the Trustee of Accotink has no prudent choice but to keep it in the protection of the Virginia Land Trust (B8845 p1444 and B8307 p1446)."

(See the pdf reference for the 7 pages of documents that are not included here)

Fear

Summary

The secret advisors frame their clients with their accounting. Here they make the innocent family member appear negligent for not reporting a joint CD, and consequently, for having to amend the Estate Tax Return. I believe one purpose is to scare Jean Nader into keeping accountings secret (as if she had done something wrong) and to divert attention from their two versions of the Estate Tax Return (They Steal Money).

I believe the secret advisors now have the innocent family member so scared of having Estate accountings fully exposed, that she feels that there is no safe place for her to turn to, except to continue to follow their secret advice. A just power could verify this with a personal visit.

Note: Before her death, my mother, Jean M. O'Connell, told me that her CPA (Jo Ann Barnes) had advised her to create a joint CD with Jean Nader in order to cover the extra expenses Jean Nader would incur as co-executor of her estate.

Page 1: The secret advisor(s) report to the IRS, on the Testator's 1991 individual tax return 1040, that the balance of joint CD# 6621 1061 is on Jean Nader's individual tax return 1040. But they don't advise Jean Nader to report it, or ask her if she had reported it, on her individual tax return 1040.

Page 3, May 29, 1992: Anthony O'Connell asks the lawyer, with a copy to the CPA firm, about this joint CD: On Schedule B under dividend income, what is the significance of **BAL ON I040 OF JEAN NADER, SSN 225 50 90521 Neither the lawyer nor the CPA firm responded.

Page 4: They have the innocent family member respond.

Page 8, January 21, 1993: I receive a statement and a check for this joint CD. I had not previously received any bank statements of my mothers at my address (6541 Franconia Road, Springfield, Virginia). I believe Mr. White requested that the bank send it to my address. I forward it to the innocent family member.

Page 10, April 26, 1993: The lawyer makes the innocent family member appear responsible: Since this was a joint account, the income was yours. Since you sent me that statement, I assumed you had picked it up on your return.

Page 12, June 21, 1993: The lawyer amends the Estate Tax Return due to the "discovery" of the joint CD. He makes a show of protecting the innocent family member in explaining it to the IRS, as if the innocent family member had done something wrong.

Page 13, July 7, 1993: The lawyer attacks me. He got the innocent family member to cosign this letter: Second, an amendment to the estate tax returns was filed at the end of

June reflecting the existence of a CD which had not been discovered until recently (See IRS correspondence attached)

The existence of the joint CD was clearly known to the secret advisors, at least as early as May 29, 1992 (which is before the June 15, 1992 due date of the original Estate Tax Return), before the lawyer tells the IRS on June 21, 1993 that it was recently discovered."

(See the pdf reference for the 14 pages of documents that are not included here)

Render Testator's Family Helpless

Summary

Greatly simplified, the secret advisors render a family helpless by first (1) establishing a wall of secrecy between family members, and then (2) using an innocent family member to carry out advice that is intended to set one family member against another. The innocent family member carries out their advice because they assume it is legitimate advice.

The secrecy and the set-ups render the family legally helpless because they use the innocent family member to carry out their agenda. If another family member tries to find out what the secret advisors are doing, such as exposing their accountings or stopping them from stealing money, they use the innocent family member to contest that other family member. They make the innocent family member accountable under the guise that they are protecting the innocent family member as well as themselves.

As preposterous as it first sounds, rendering the family helpless is a certainty, it is a virtual given, it impossible to prevent, if one innocent family member relies on the fraudulent advice. I anticipated it, I did everything I could think of to try to stop it, and I could not.

Page 1 -Mr. White is asked, on behalf of all the beneficiaries, to relinquish his fiduciary position to Anthony O'Connell.

Page 2 -Mr. White refuses.

Page 3 -I ask Mr. White some questions about his accounting.

Page 4 -The first accounting questions I ask Mr. White results in Mr. White refusing to communicate with me and placing the innocent family member between himself and me.

This structure of the secrecy and the use of the innocent family allow Mr. White to run the set ups that render the family helpless.

Pages 5 and 6 -With the wall of secrecy supposedly in place, the set-ups using the innocent family member begin.

Set-up #1

Accounting entanglement using document

AGREEMENT CONFIRMING DISTRIBUTION OF VEHICLE

Please see page 7

Set-up # 2

The lawyer hires the CPA

Edward White unilaterally hires the CPA Jo Ann Barnes to advise the Edward White on the Trust u/w of H. A. O'Connell. I am the Trustee for the Trust u/w of H. A. O'Connell

My guess is that the CPA's secret advice to the innocent family member agrees with the lawyer's secret advice to the innocent family member concerning the Trust and the Estate. See CPA. The CPA does not disagree with the lawyer's advice in the lawyer letter of April 22, 1992. I know of no instance of the CPA disagreeing with the lawyer's advice since 1985.

Set-up # 3

Entangle Trust accounting with Estate accounting

Please see pages 10-18

They stress this. This is important. It allows them to "capture" about a million dollars in real estate by entangling it in their accounting of the Trust and their accounting of the Estate.

Jo Ann Barnes and Edward White create accounting entanglements and use them as takeover tools. It gives them control of an asset somewhat like an attachment, except that their entanglements are usually impossible to pin down and address, and only they, and not their clients, have the power to remove them. Because they control the entanglements they control the assets and people they entangle. They exercise these takeover tools at a critical time, such as during a sale negotiation and settlement of real estate. They are used to create conflicts, to set one family member against another, to divide and conquer, to supplant. A good example is the 1985 Needs how much in Testator.

Forcing me to file the Trust's account approximately 18 months early allows the CPA and lawyer to entangle their accounting of the Trust's (I unwittingly hired the CPA (firm) to prepare the Trust's Seventh Court Account) with their accounting of the Estate. The Trust's Seventh Court Account is not due until October 20,1993 (page 10).

Entanglement by creating a debt from the Estate to the Trust

The CPA (firm) did the Trust's Seventh Court Account in a manner that required me to pay the Estate $ 1,475.97 (page 11). The lawyer discovers that this is $659.97 too much (page 12). They report this to the IRS while I can not even get the CPA(firm) or the lawyer to address this $659.97 much less pay it back to the Trust (page 18).

Entanglement using the real estate tax:

(It is so ambiguous it can be used in any way they want).

I am of the opinion that the estate owes the trust for the second half real estate taxes from September 15,1991 through December 31,1991 in the amount of $1052.35. This is shown on your accounting a disbursed to the heirs. Should this be paid back to the heirs or to the Trust? Lawyer to Trustee, May 19, 1992 (page 12)

The $1,794.89 of real estate taxes which you as Trustee paid on behalf of the three heirs

(Sheila O'Connell, Jean Nader and Anthony O'Connell) was an obligation owed directly by the three heirs as your mother's interest in this real estate passed directly to each of you at her death. When you received the K-1's for 1991, attached was a schedule for each of you to report 1/3 rd of these real estate taxes on your individual income tax returns CPA(firm) to Trustee, February 12, 1993 (page 17)

Set-up # 4

A policy of secrecy from me is established

Set-up # 5

This continues a series of set-ups to take control of Accotink

April 22, 1992:

The best scenario of the three alternatives given here would reduce Accotink's value by 40%.

I avoided the structured set up by hiring a professional appraiser and sent Edward

White a completed professional appraisal on June 9, 1992 that reduced the valve of Accotink by 50%.

December 11,1992:

The lawyer and the CPA suggest asking for an additional 30% reduction. I believe this is to take control by promoting an adversarial partition suit:

.... Since the lands is held as tenants in common, it could be partitioned into smaller facts (zoning problems not withstanding) and either the trust or any of you could sell you interest if a buyer could be found. ....

Edward White to the beneficiaries

February 2,1993:

..... I can only say that had I not been adamant about re-valuing the Accotink property, Mr. O'Connell's initial approach would have cost this estate

dearly.. . . . . .

Finally, I would like, for the record some memorandum from you and Sheila concerning my earlier comments as to attempting a further reduction in the Accotink valuation. Lawyer to Jean Nader, February 2,1993

I believe the reevaluations of real estate are not only used as a takeover tool but to steal money in the created confusion:

June 11,1992:

I gave Edward White the professional appraisal on June 9, 1992, which is before the June 15,1992 due date for the Estate Tax Return. But on June 11,1992 the lawyer extends the Estate Tax Return filing due date anyway, telling the IRS on the $175,000 version of the Estate Tax Return that the appraisal is still in progress:

The decedent was a part owner of a tract of ground the value of which is to be determined by an appraisal in progress. The enclosed payment is based on the maximum value for the property and will be changed.

Edward White to the IRS

January 13,1992:

As you recall the Accotink property is assessed at $600,000.00 by the county.

Based on the appraisal, we used one half of that figure (times the percentage interest owned by your mother). In the event the IRS does not agree and insists on the full evaluation, the estate tax liability could increase by about $67,000.

Edward White to the beneficiaries

Set-up # 6

Entanglement using gift

Please see page 9

My having a copy of the Form 709 for 1988 may or may not have stopped this entanglement.

Set-up # 7

Covers

The Debts and Demands, the Show Cause Against Distribution Order and the Order of Distribution are optional. Because the secret advisors ask for these approval type procedures after keeping accountings secret and stealing money, they apparently believe it will help cover them.

Set-up # 8

The secret advisors got their Order of Distribution and the release of liability letter from the IRS clearly knowing that they framed me with the debt of $659.97. Now they can use it to control Accotink and continue to make it appear as if it were my fault. Please imagine the consequences if I had not corrected the huge debts in My Credibility."

(See the pdf reference for the 18 pages of documents that are not included here)

They Use The Trust of Judges

Summary

The Show Cause Against Distribution Order and the Order of Distribution, as well as the

Debts and Demands, are optional. The secret advisors ask for them after keeping accountings secret and stealing money. They use these as cover."

(See the pdf reference for the 8 pages of documents that are not included here)

Sabotage Sale, 1988

Summary

I sent Edward White a signed and notarized Purchase Agreement for a real estate sale I made in my capacity as Trustee and asked if he would handle the settlement (Page 1). Three and a half months later, five days before settlement, Edward White sent me a deed to sign that states, among other things, that I could not qualify as Trustee (Pages 4 and 5). Court records show I was qualified as Trustee (Page 6): Edward White put me in the position of having to sign this deed as written or he would make it appear to my family that I was obstructing the settlement. I signed the deed as written.

By law settlement has to be made in accordance with the terms of the Purchase Agreement unless all parties agree to any changes. The lawyer did not ask or notify me of any changes (page 3). The Purchase Agreement requires that the lawyer represent only all or only none of the individuals comprising the single legal entity of "Seller" (page 2). If the lawyer is representing none he should not be sending them deeds to sign (page 4) or charging them for his services (page 7).

Please note that Edward White's version given to my mother (page 8) is different from the version given to the Bar investigator (pages 9 and 10). This is what they can get away with. Edward White does not even have to take an accountable position.

If I had let the secrecy or the deed drive me to hire another lawyer here, then again, Edward White could technically avoid fiduciary responsibility to me because I hired another lawyer (but remain in charge of the real estate sale that I am responsible for and which by definition requires fiduciary accountability), and I am made to appear as the adverse party represented by counsel. What stopped me from falling for the hire-another attorney-trap here is that I did not believe that a lawyer could get away with deviating from the terms of this straightforward Purchase Agreement.

Unless a just power intervenes a similar thing will happen if the Trustee tries to sell the remaining real estate (B8845 p1444 and B8307 p1446). They have already sabotaged the Trustee's planned sale of this real estate. The evidence is in their accounting of the estate of Jean M. O'Connell."

(See the pdf reference for the 10 pages of documents that are not included here)

Sabotage Sale, Again

Summary

Accotink is our family's remaining real estate. It's valuable. I had a contract for it in 1989 for $1.15 million. The secret advisors have targeted it for takeover. To prevent a hostile takeover I asked my sisters to put it in a Virginia Land Trust with Anthony O'Connell as Trustee (B8845 p1444 and B8307 p1446). My sisters and I want to sell Accotink but Jo Anne Barnes and Edward White have already sabotaged the Trustee's planned sale by entangling it in their accounting of the Estate of Jean M. O'Connell and of their accounting of the Trust u/w of H. A. O'Connell. My sisters do not understand that these accounting entanglements are intended to sabotage the Trustee's sale. Jo Ann Barnes and Edward White create accounting entanglements and use them as takeover tools. It gives them control of an asset somewhat like an attachment, except that their entanglements are usually impossible to pin down and address, and only they, and not their clients, have the power to remove them. Because they control the entanglements they control the assets and people they entangle. They exercise these takeover tools at a critical time, such as during a sale negotiation and settlement of real estate. They are used to create conflicts, to set one family member against another, to divide and conquer, to supplant. A good example is in 1985, in the Needs how much in Testator.

The secret advisors have made it appear that I am responsible for the entanglements they created. I do not have the power to stop them from doing this or to compel them to remove the entanglements I know about. Unless a just power intervenes and compels the exposure and removal of all their accounting entanglements the Trustee has no prudent choice but to leave Accotink in the protection of the Virginia Land Trust. It would be walking into a known trap to try to sell Accotink until all their entanglements are exposed and removed and Accotink is left free and clear.

Known entanglements:

Entanglement using document entitled AGREEMENT CONFIRMING

DISTRIBUTION OF VEHICLE (Render Testator's Family Helpless, Set-up #1)

Entanglement by creating a debt from the Estate to the Trust (Render Testator's Family Helpless, Set-up # 3)

Entanglement using real estate tax (Render Testator's Family Helpless, Set-up #3)

Entanglement using gift (Maybe) (Render Testator's Family Helpless, Set-up # 6)

Entanglements that would have been unless I had openly pointed them out:

Entanglement of the 1991 capital gains tax of $28,334.00 in federal tax, plus penalties and interest (My Credibility).

Entanglement of the 1991 capital gains tax of $5,712.00 in Virginia tax, plus penalties and interest (My Credibility).

Entanglement of the 1992 capital gains tax of about $113,336.00 in federal tax, plus penalties and interest (My Credibility).

Entanglement of the 1992 capital gains tax of about $22,848.00 in Virginia tax, plus penalties and interest (My Credibility).

Unknown entanglements:

The pattern is that there will be surprises. That is one reason I need a 100% true and complete financial disclosure before trying to see Accotink.

Are there any other debts which your mother owed the Trust?

Edward White to Anthony O'Connell,, May 19, 1992"

(See the pdf reference for the 1 page document that is not included here)

My Credibility

Summary

My sisters used to trust me (page 1). Then the secret advisors attacked my credibility.

Why? Because (1) I have experience in accounting and they don't want my sisters and others like you to believe me, or, (2) because I have actually done some thing wrong?

(1) Common sense says the secret advisers would want me to see their accountings if they had nothing to hide. Especially after I point out their omission of $28,334.00 in federal tax and $5,712.00 in Virginia tax for tax year 1991 (page 2), and their planned omission of about $113,336.00 in federal tax, and $22,848.00 in Virginia tax for tax year 1992 (page 2-5). I have an MBA, I have worked for the IRS, and I have done my homework. I am the one who they most want to not see their accountings.

or

(2) If I have done something wrong, what is it? I can't get them to identify it (.......For

the umpteenth time, I will ignore your plaintive request that I identify your "wrongdoings", Edward White, July 20, 1995). Please compel Jo Anne Barnes and

Edward White (Please set aside whatever the innocent family may send you. Jean

Nader has been set up to protect them) to identify in writing exactly what it is that they have accused me of. Allow me to respond if they do. They should have some legitimate reason for destroying my credibility. They don't.

Now my sisters do not trust my advice. They trust the secret advisors advice. About one million dollars in real estate is at stake (B8845 p1444 and B8307 ~1446). I believe my sisters will never understand that they should not trust the secret advisors advise unless they hear it from a just power.

I beg you; I literally get down on my knees and beg you, to verify fraud by trying to pin down Jo Anne Barnes and Edward White to an accountable position on their implications of my "wrongdoings". Why did they destroy my credibility?(page 3). If a Judge can't pin them down to an accountable position on this, please understand how the public and I can't."

(See the pdf reference for the 5 pages of documents that are not included here)

Correspondence with Judge Thomas S. Kenny

I am sorry to read that Judge Thomas S. Kenny died of cancer"

(See the pdf reference for the 6 pages of documents that are not included here)

Related documents

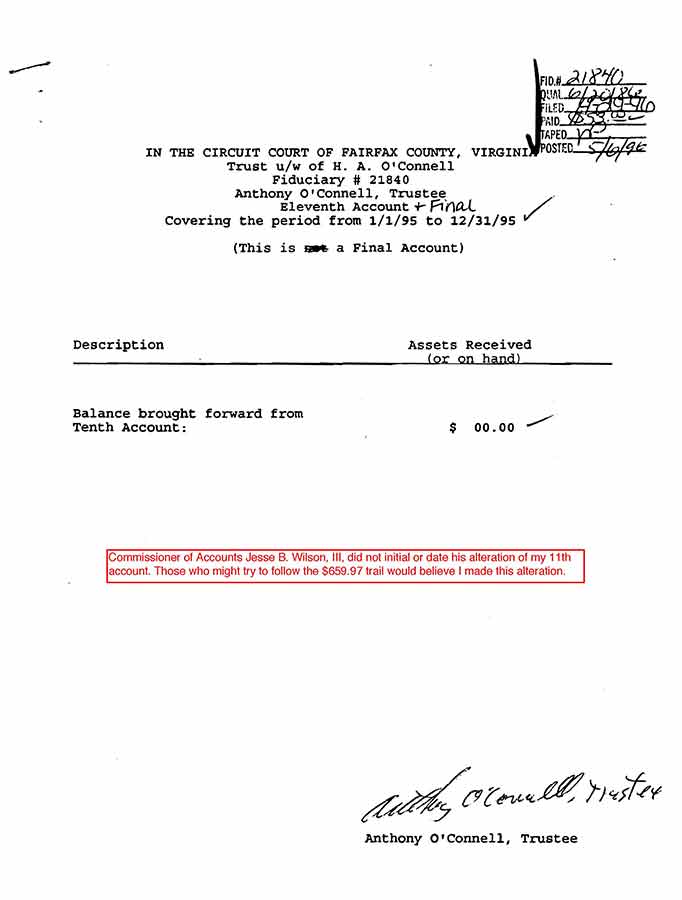

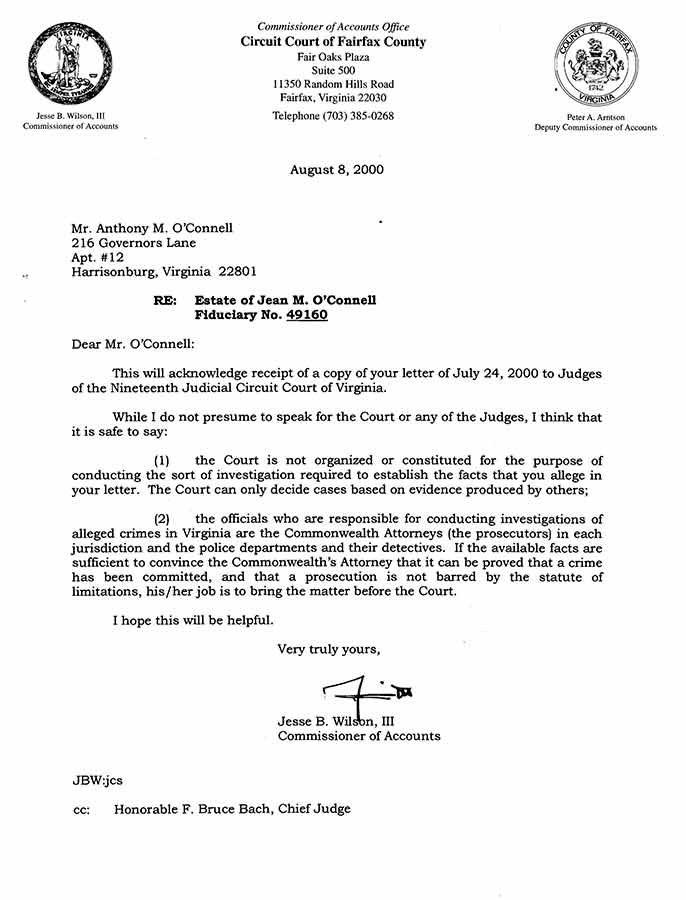

(below) The Commissioner of Accounts closed my trust account against my intent.

>

(above) I filed an Exceptions to the Commissioner's Report and it

disappeared after being received by the Court on August 23, 2000.

(below) I was told my letter was inappropriate ex parte communication.